The most recent “Clippings” posting on Substack was titled “Reflexivity,” and featured the credit cycle, money for advisors from the alts rush, the Berkshire cash hoard, KKR’s explosive growth, and much more (even a timely cartoon). Each edition provides an eclectic mix (like these Fortnightly compilations), but you can zip through them quickly, since it’s all about the pictures. (Subscribe here.)

On to the readings.

The AI design problem

In a LinkedIn posting, Ken Akoundi argues that we treat human errors and AI errors differently. The former are “unsurfaced, unmeasured, or unreported,” and the latter are “scrutinized, logged, debated”:

This isn’t a people problem. It’s a design problem.

We’ve built workflows that depend on humans to do what humans are worst at: repetitive precision at scale.

And then we judge AI against a standard we’ve never actually measured in ourselves.

Writing for CFA Institute’s Enterprising Investor, Markus Schuller poses a question about “epistemic architecture: whether machines strengthen or weaken the human processes that generate knowledge.” While Schuller addresses the issues in broad (even civilizational) terms, the theme can be applied to the investment industry or an individual organization:

Machines may extend human capabilities, but they cannot replace the need for evidence-based reasoning, institutional design, and ethical deliberation. As AI becomes embedded in decision systems, the decisive question will not be machine capability but whether human governance remains anchored in the pursuit of evidence rather than technological promises.

Tom Slater of Baillie Gifford strikes a similar chord as Schuller in his article, “AI isn’t coming for your job. It’s coming for your mind.” AI “supercharges variation . . . reshapes transmission . . . and rewires selection” of ideas:

The concern is not that these new capabilities are worthless but that they may come at the cost of the foundational skills they depend on. An engineer who has never built a model from scratch may not recognise when an AI’s output is technically flawless but structurally unsound. A scientist who has never struggled through a statistical analysis manually may not spot results that are mathematically correct but conceptually meaningless. Verification without prior mastery risks becoming a superficial check rather than a genuine evaluation.

While Slater’s piece is not about investment organizations, his conclusion is directly applicable:

The people who will thrive are not those who use AI the most, but those who can still think without it. The institutions that will matter are not those that adopt AI fastest, but those that preserve the human capabilities AI cannot replace.

As Ken Akoundi said, we have a design problem. Now there is a confusing rush of AI; what needs to emerge is thoughtful organizational design thinking that combines people and machines in productive and sustainable ways.

(Since the Investment Ecosystem’s work focuses on organizational design and investment process, this is an area of emphasis for us. Get in touch if you want to explore it further.)

In the weeds

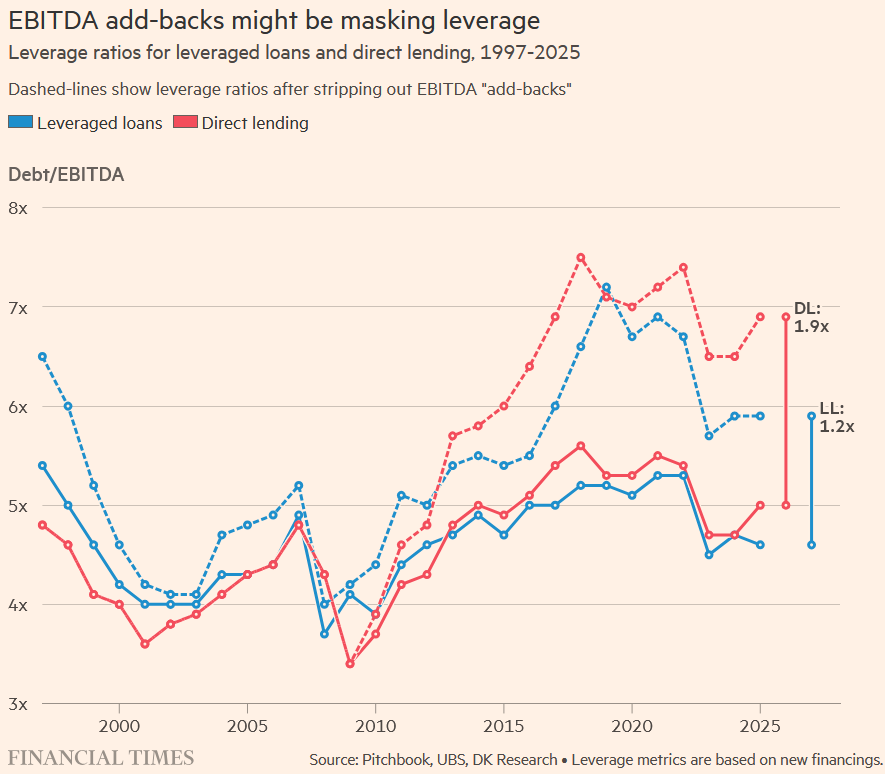

The real or perceived hiccups in private credit have spawned quite a bit of interest from independent researchers, who are trying to dig through the opaque filings of providers to see what’s really there. Here are two (of many) examples.

Nick Nemeth of Mispriced Assets doesn’t shy from a fight in his posting, “The Ares Lies.” It is “a line-by-line rebuttal of what Ares said on the April 28 earnings call.” One area of interest is the wide ranges in pricing on multiple loans to the same company.

Another bold assertion comes from Grizzly Research’s report on Partners Group:

We found numerous instances where the Master Fund’s valuations did not reconcile with the reality of the underlying businesses. We estimate close to 40% of the evergreen funds’ investments might be severely mismarked.

“Wait,” you might say, “Are we to believe a Substack writer or an activist short-seller over a large, successful, professional asset management organization?”

Good question.

It seems that this is where we are. The answers are in the details and the asset managers don’t really provide the details or answer hard questions about them.

There’s also this: Most people aren’t prepared to analyze complex credit matters regarding individual companies to say nothing of vast portfolios of them. That may be the case for some of the people writing about the area — but it also is likely true for many allocators at institutions who are investing in these funds or advisors who are recommending them to others.

Whichever way this current state of unease about private credit breaks, it’s clear that the scrutiny of current practices needs to be ratcheted up.

Voluntary blindness

Mark Higgins wrote a posting for Investing in Financial History, titled “The Voluntary Blindness of Modern Finance,” leveraging a paper he had recently published:

Mark Higgins wrote a posting for Investing in Financial History, titled “The Voluntary Blindness of Modern Finance,” leveraging a paper he had recently published:

The thesis is that the field of finance has come to rely too heavily on quantitative models, which restricts accepted truth to a narrow band of observations that can be proven at a high level of statistical significance. As a result, academics, policymakers, regulators, and many practitioners voluntarily blind themselves to simple, time-tested principles.

This entrenched bias toward quantification would be less concerning if conventional models were merely incomplete. The problem, however, is that their very design makes them likely to fail during the rarest and most impactful events that shape economic and market cycles.

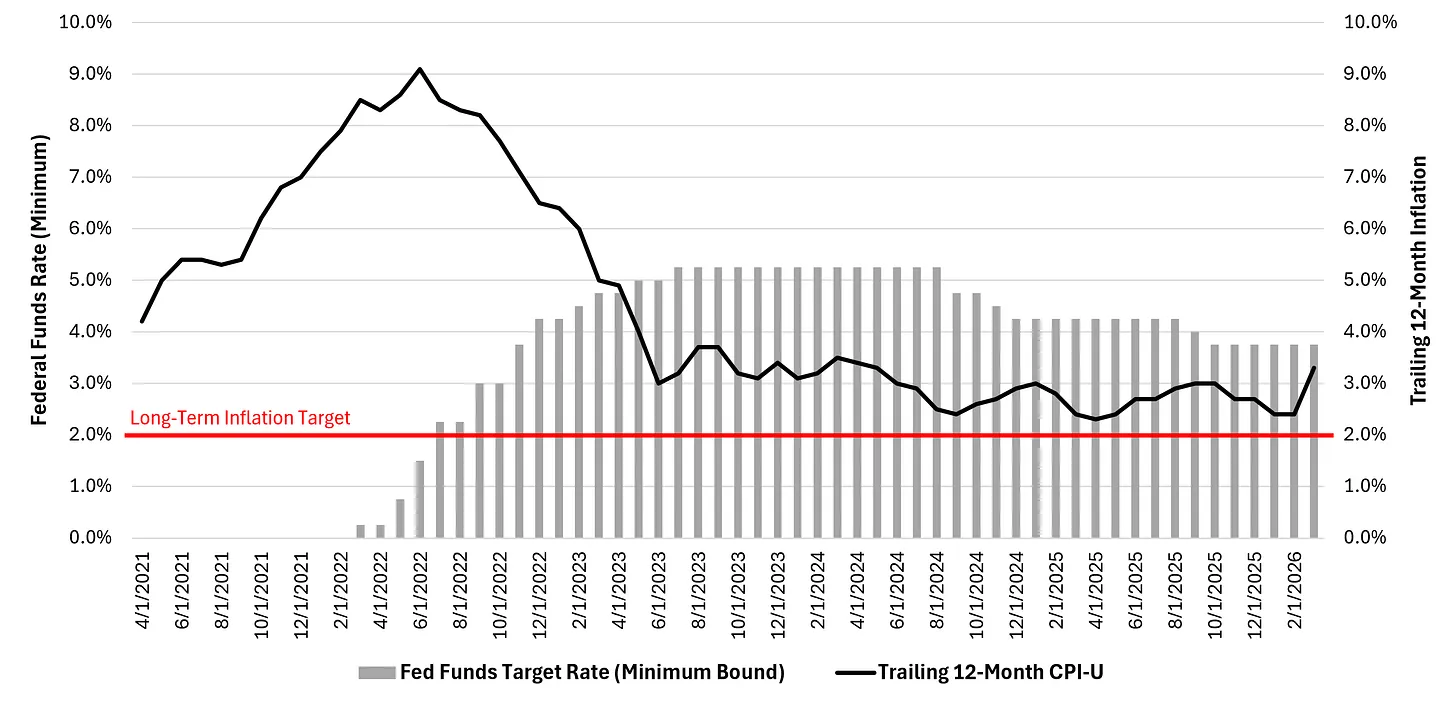

One example is illustrated in the chart above, which shows that the Federal Reserve ignored the simplicity of its inflation target for a “data dependency” that led it to lower rates before the objective was achieved, making it more susceptible to any inflation pressures, such as those caused by the war with Iran.

Higgins also delves into assumptions about private credit, the “structural incentive” for investment consultants to encourage more portfolio complexity, and “the paradox of academic precision.”

(To go with Higgins’ “voluntary blindness,” there was the “blissful ignorance” of those at this year’s Milken Institute conference, as detailed by the Financial Times. With stocks doing well, attendees ignored the concerns of more common folks, with one saying, “Does anyone really care if the Strait of Hormuz is open?”)

Daily pricing

Apollo made news by announcing that it was going to begin pricing its private credit assets daily. Matt Levine pointed out that individuals who may want to redeem their holdings will welcome the increased visibility, but it’s just more work (more check-ins, more questions from the boss, etc.) for institutional asset owners:

If you are a retail investor in an Apollo business development company, that is probably helpful. If you’re an institutional investor in private credit funds, though, being blithely ignorant about the value of your portfolio was kind of nice, and now you are stuck knowing the price.

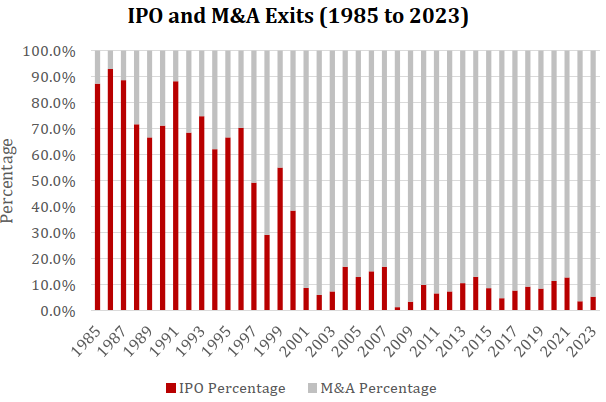

A math problem

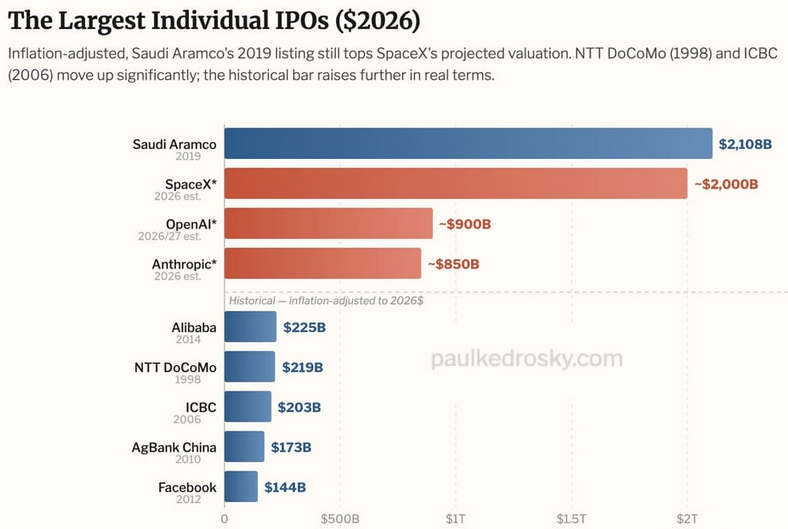

Paul Kedrosky featured this chart in a posting titled “The Coming Mega-IPO Flow & Funding Problem of 2026.”

The floating of Saudi Aramco in 2019 (a tiny float, by the way) gave that IPO a larger value than any of the big ones on the horizon (SpaceX, OpenAI, and Anthropic). But here’s the stunner: “All three together would exceed the entire dot-com IPO wave of 1995–2000.”

That creates “a math problem” for the market.

Other reads

“The Snapshot-in-Time Effect,” Byrne Hobart, Capital Gains.

If you want to be early to spotting changes, you have to treat the trend as a measure of some underlying reality that might not endlessly trend in the same direction.

“The Day Warren Buffett Sat in the Crowd,” Robert Dee. The Berkshire annual meeting — and a wait-and-see on Greg Abel.

“The Last Moat,” Ian Cassel, MicroCapClub.

The ultimate edge is still simply being present with management in varying ways that most other investors aren’t doing.

“Should Your Mom Have Private Equity in Her 401K?” Elisabetta Basilico, Alpha Architect. Perspective for individuals and financial advisors.

“The Case for Avoiding Riskier Funds,” Jeffrey Ptak, Morningstar.

Riskier funds didn’t make enough to compensate for their higher volatility; they died more often, succeeded less often, and cost more than less-risky funds.

Also, because more-volatile funds are likelier to get on our nerves, we may earn less on our average dollar than would be the case if we invested in less-volatile funds, the difference owing to inopportunely timed purchases and sales.

“Does size matter?” Ani Bruna, FT Alphaville. A lot of investors comb through 13F filings to see what managers are doing; those filings can give misleading indications of the sizes of exposures.

“You Say You’re Different. You Look Exactly the Same.” Claudia Quintela, The Emerging Manager.

The pitch decks look the same. The fact sheets look the same. The way managers sit down and open with their background, then walk through the strategy page by page, then show the performance chart, then ask for questions. The choreography is identical across hundreds of meetings.

“The Disappearance of the Ten-Year Fund,” Robert Bartlett and Paolo Ramella, SSRN. Implications from the extension of fund lives.

“Global Primer Series: Private Credit,” AP Research.

Today’s valuation problem becomes tomorrow’s refinancing problem. And none of that requires a banking panic, just enough borrowers to discover that the private market will not keep extending time on yesterday’s assumptions.

The lifeblood

“I would not underestimate the kind of creativity that shows up when fees are on the line.” — Debt Serious.

Flashback: Mark Mobius

The earliest New York Times article that mentions Mark Mobius was in 1971:

The head of a Hong Kong based trade research and development company proposed here yesterday the establishment of a private China trade fund to promote commercial exchanges between mainland China and the United States.

That was before Nixon’s groundbreaking visit to China the next year. Mobius always seemed ahead of his time and came to define emerging market investing after he began managing a fund for John Templeton in 1987, whose firm would later merge with Franklin to become Franklin Templeton.

Mobius died in April. His obituary in the Times revealed his relentless and nomadic quest to find the best emerging market stocks. It also included this surprising history:

Mr. Mobius did not become an investment fund manager until he was in his 50s. Before that, he held an assortment of jobs, including teaching communications, working at a talent agency, marketing Snoopy cartoon merchandise in Asia and operating his own financial research business.

The banality of investment process

A 2023 essay on this site used a documentary about the Beatles to draw analogies from their creative process to the investment process of an organization. A reminder: trying to assess an investment team by observing one of their meetings (which, in front of potential clients, are “more performance than reality”) is a poor substitute for all that you can’t see:

The messiness of the process isn’t there — and it is in that messiness that the alchemy often takes place, where the connections, conflicts, confusions, and true underlying culture come to the fore.

Thanks for reading. Many happy total returns.

{kind=link}

{kind=link}

Published: May 11, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.