The questions of the day at organizations of all kinds revolve around artificial intelligence. What functions can AI reliably perform? How will it change our process and business model? Who will be replaced as a result?

The range of possibilities is extremely broad and varies across different kinds of investment organizations. This posting reviews the findings of a recent academic paper that uses AI in its analysis, presages issues for asset management firms (and their clients) to consider, and challenges a popular investment notion.

It’s important to remember that the great bulk of research into asset manager behavior is based upon the study of equity mutual funds in the United States, and that is true in this case too. Therefore, the findings can’t necessarily be extrapolated to other realms. And, since this is a new angle of research, you can expect the concept to be further investigated by the authors and other researchers.

Findings

The paper, “Mimicking Finance,” was written by Lauren Cohen, Yiwen Lu, and Quoc H. Nguyen. They used AI and machine learning “to extract and classify the part of key economic agents’ behaviors that are predictable from past behaviors.” Those key agents? Portfolio managers.

Among their findings:

~ “71% of mutual fund managers’ trade directions can be predicted in the absence of the agent making a single trade.”

~ Manager behavior “is more predictable and replicable” for those with more experience as a portfolio manager, those within less competitive fund categories, and those who manage across multiple strategies.

~ Portfolio managers with larger ownership stakes in the funds they manage are less predictable. So are funds that have more managers.

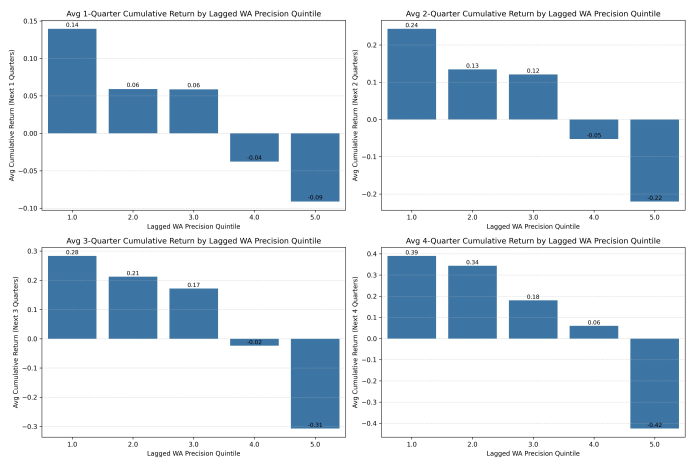

~ “Less predictable managers strongly outperform their peers, while the most predictable managers significantly underperform.”

~ “Even within each manager’s portfolio, those stock positions that are more difficult to predict strongly outperform those that are easier to predict.”

As shown below, when arranged by quintiles of predictability (less predictable managers are on the left of each chart), cumulative performance is monotonic. (However, the longest period measured is a year after the predictability clusters are formed; future research should look at returns beyond that horizon to see if results vary with an extended time frame.)

Musings

With every study — whether it is published externally or produced internally — you need to consider how it fits with the existing body of knowledge and whether it rings true to the world as you know it. Then you might adjust your prior views in response, dig in and do some research yourself, or dismiss it out of hand (if you have reason to believe that there’s something wrong with the data or the conclusions drawn).

As laid out above, the findings address the predictability of asset manager behavior, leading to a potential assumption by a reader that AI can replicate a significant portion of an asset manager’s decision making, allowing for AI substitution in the process (potentially lowering costs significantly).

But look at the last two bullet points. That’s where the interesting part of this research comes in. Does alpha come from the less predictable actions of portfolio managers? (The “non-routine” decisions, to use the authors’ description.)

If so, what does that say about the “consistent and repeatable” mantra that asset managers consistently repeat as part of their narratives — and that capital allocators regurgitate in describing the targets of their selection processes?

Maybe predictability isn’t all it’s cracked up to be. Maybe creativity is the essence of alpha and we’ve been looking for sameness when we should be trying to understand the elements of variability — what kinds of changes add value and what ones detract from it — as well as judging the penalty for stasis in an evolving investment ecosystem.

AI bots can mimic what has worked in the past. Humans should bring something else to the endeavor.

Related essays on this site you may want to read include “Balancing Exploration and Exploitation in Investment Organizations” and “The Active Management Reinvention Project.”

Published: March 18, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.