The second posting of Investment Ecosystem Clippings came out recently.

It’s an offshoot of this site, available on Substack — a scrapbook of charts and other pieces that illustrate happenings in today’s investing world.

Quick to review and full of diverse ideas, a new edition will be coming out soon. You may sign up here.

Private equity data

Speaking of Substack, there has been a blossoming of investment-related newsletters on the site in recent months, several of which focus on alternative investments.

Among them is one by Ludovic Phalippou, a professor at the University of Oxford who has challenged much of the private equity orthodoxy.

A helpful posting, “Navigating Private Equity Data: What the Main Datasets Actually Contain,” provides a synopsis of a recent paper, of which he writes:

The paper does not argue that any dataset is superior in all dimensions. Instead, it documents the strengths and weaknesses of each source and emphasizes that data choice should be driven by the research question.

Private equity data has improved substantially over time, but important limitations remain. Transparency about data construction, careful validation, and modesty in interpretation remain essential.

Statistics about private equity performance can be squishy; serious research starts with this kind of detailed knowledge about the data used.

See also: “Yale. How an IRR Became a Legend.”

It is a story about numbers, incentives, and how an entire industry collectively decided not to look too closely once a good narrative emerged.

It should be required reading for every asset owner and (now that individual investors are the major targets of the industry) every investment advisor. Not because there aren’t opportunities in private equity to be had, but because the narrative force field built up over time contains distortions that should have long since disappeared.

(Tim McGlinn of TheAltView has published several examples of industry advocacy groups, asset managers, and asset owners mixing internal rates of return with time-weighted ones in reports, obscuring the true economics at work. See, for example, a posting about “fun with numbers” in pension league tables and a follow-up to it.)

Boutique manager failures

A podcast featuring Chris Banholzer, Chas Burkhart, and Brad Mook of Rosemont Investment Group explored the topic, “Lessons Learned from Boutique Asset Manager Collapses.” (A transcript is also available.)

In looking at the data, “What started as a handful of high profile blowups over the last fifteen or so years, now feels a bit more systemic.” Once substantial businesses have lost large percentages of their assets under management.

Performance challenges are a factor, as are undue concentrations in product categories, clients, subadvisory arrangements, or consultant support — especially when there has been a lumpiness of inflows around performance peaks. But some firms survive and others fold or just limp along. One broad problem:

Great management and great leadership have proven over time to be extremely difficult to achieve.

Given the inherent variability in outcomes over time, sustainability depends on the soft attributes, the “behavioral characteristics of the people” across a variety of market and competitive environments, as well as the real culture (as opposed to the advertised one).

Succession issues and the need for an ownership transition often aren’t tackled in a timely fashion, which can lead to a sale to a financial buyer and the erosion of the franchise.

There’s much more of worth in this discussion among the principals, who make minority investments in asset management firms.

Mania and value in ESG

Two very different pieces of research on ESG came out recently, as is evidenced by their contrasting titles: “ESG Mania and Institutional Investments” (Riza Demirer and Huacheng Zhang) and “ESG Value Creation in Private Equity: From Rhetoric to Returns” (Evan Greenfield, Ashby Monk, and Dane Rook).

Mania: The authors of the first study categorize ESG investors as those who are “impact-chasing” (interested in achieving specific goals) and those who are “impact-washing” (“mainly driven by pragmatic motivations, including pecuniary, fad, agency concern, or fund flow”). Their conclusion:

Overall, our statistical and economic analyses show that most institutions crowd into the ESG market not because they aim to chase impact but more likely because they tend to impact-wash their funds.

Value: The second is a much different kind of paper, focused on situations where ESG is “embedded in investment judgment and aligned with fiduciary duty.” It summarizes the approach across the private equity investment cycle by British Columbia Investment Management Corporation (BCI). Three cases are offered, each of which includes descriptions of the activities that are attributed to ESG considerations and the specific changes in enterprise value that are expected as a result. The authors end by offering “five guiding principles for embedding ESG into the core of private equity investing.”

The casino

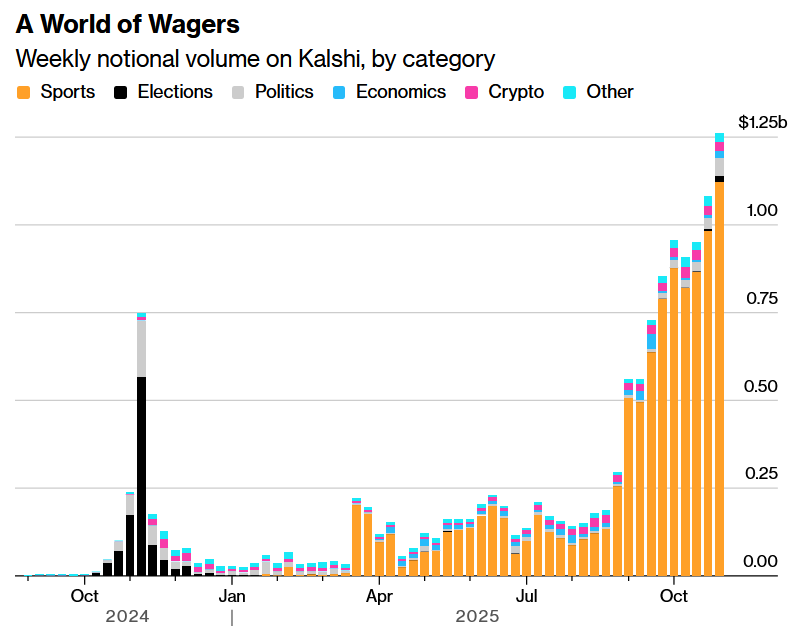

A Bloomberg story by Lu Wang examines “the fading line between investing and gambling.” There is a great conversion happening between prediction markets, sports betting, and traditional investment markets. Spawned by loosened regulations, the ease of placing wagers on phones, and the propensity of users to take leveraged positions, the scramble for a piece of the action among exchanges, trading houses, and other players has become relentless. New boundaries are being drawn:

To regulators the stakes are no longer just financial. They’re existential. If every interface becomes a casino, where does responsibility lie? With the trader? The tech? The system itself?

As the chart above shows, the 2024 elections caused a spike in activity (at least on Kalshi), but the big change on that site came when sports came into play.

We are clearly in the loosening part of the regulatory cycle, with professionals and amateurs flooding in to take advantage. It may go the other way some time in the future, but for now it’s full speed ahead.

Rolling the dice

An Institutional Investor article from Michelle Celarier about Seawolf Capital, which had strong performance last year, is unusual in that the firm is quoted as being unusually blunt about its aggressive tactics. A Mafia metaphor and a sports one (a shot clock) are involved. In the markets, as in the underworld, you never really know when time will run out.

Timing is everything

It’s hard when you make a bold call within an organization and it goes wrong, especially when it goes wrong right away. But (for the most part) it stays inside.

Not so for those on the sell-side who put out reports that announce and memorialize their calls. One particularly bad bit of timing recently: downgrading Venezuelan bonds the evening before the Saturday intervention by the United States that unleashed a wave of positive speculation about the nation’s prospects. Oof, indeed.

Other reads

“There Are No Counterfactuals,” Old Rope Research.

Processes can and should change. Investing is a field in which every circumstance is a 1 of 1, unfortunately. Pattern recognition and applying certain mental models do work, but only insofar as the facts and underwriting probabilities line up with the current market pricing.

“This is How a Run on an Insurance Company Could Happen,” Rod Dubitsky, Rod’s Substack. Looking at the “deep trouble brewing” at two insurers to see “how a run could happen on PE linked insurance companies.”

“The red flags investors should look for in private lending,” Michael Gatto, Financial Times.

Financial statement analysis has become something of a lost art in today’s era of rapid capital deployment in the credit markets.

“Jain Hedge Fund Costs Cut Into $750 Million Profits in 2025,” Nishant Kumar, et al., Bloomberg. The pod shop model in start-up mode: “gross returns in the mid-teens shrank to about a net 3.7% gain” for investors.

“Fast and Unsteady,” Jeffrey Ptak, Basis Pointing.

It’s a fool’s errand to try to handicap which funds will rank near the very top of their peer group 10 years hence. Stick with what you can count on — such as the persistence of fee differences between funds — and that should yield a more-than-acceptable result.

“The Evolution of GP Financing Solutions: From GP Stakes to GP Structures,” Dawson Partners. “Anemic” distributions have led to new forms of financing.

“Asset management is not a meritocracy,” Joachim Klement, Klement on Investing.

In short, even in a business where it is remarkably easy to assess the performance of an employee in numerical detail, women and minorities are subject to unconscious biases. And they say DEI initiatives aren’t necessary . . .

“Alignment Over Access: Gauging the Fit Between Alternative Investment Strategies and their Fund Structures,” John Moore, CAIA Association. How to evaluate vehicles repackaging institutional strategies in wrappers created for broader access.

Wanting

“There are only two tragedies. One is not getting what one wants, and the other is getting it.” — Oscar Wilde.

Flashback: The risk of risk management

During the depths of the financial crisis, quantitative finance expert Paul Wilmott offered thoughts on how “a failure to see beyond the numbers” dooms risk management as it should be practiced. He uses a simple example of a magician picking a card from a deck as an analogy to make his point:

This is really a question about whether modern risk managers are capable of thinking beyond maths and formulas.

Do they appreciate the human side of finance, the herding behaviour of people, the unintended consequences — what I think of as all the fun stuff?

Too much risk management stops before all that fun stuff (which is ultimately the most important).

Quantitative strategies

All of the previous postings are in the archives. For example, a 2022 posting covers an interview with Campbell Harvey on important topics in quantitative investment (and a few other things). It’s worth reading three-plus years later to see what has changed. One thing hasn’t, which closed the piece:

According to Harvey, “Short-termism is a fundamental problem with our political system and with the way businesses are run.” (And with much investment decision making.)

Thanks for reading. Many happy total returns.

Published: January 19, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.