Since the last Fortnightly, we’ve published an essay on portfolio manager predictability and alpha generation — and a Clippings posting that had images related to energy, fixed income, pod shops, emerging managers, the questionable but sticky concept of a “technical correction,” and more.

On to the readings for this issue.

Rewiring the ecosystem

CAIA Association released a report called “The World Rewired.” It highlights three categories of shifts that are occurring — macro, industry, and organizational — creating a “wholesale rewiring” of the investment ecosystem:

For decades, capital allocation strategies were built on a few key assumptions: steady globalization, relatively uniform regulatory frameworks, and a clear separation between public and private markets and their participants.

No longer.

Geopolitical risk is increasing, so “understanding the political durability of an investment thesis is now as important as modeling cash flows.”

Are the vehicles and structures that defined the modern investment era fit for purpose going forward? The report repeatedly touts the benefits of tokenization and the risk to current applications (and assets under management) for those who lag behind the adoption curve.

Asset owners, asset managers, and other entities need to revisit their assumptions for organizational design, incentives, and governance — and to hire different kinds of talent and rework process, especially to tap emerging capabilities of artificial intelligence.

The ideas go hand in hand with CAIA’s Vision 2035. Some of the ideas may be spot on as to what will happen while others will miss the mark; that’s the nature of such exercises. Yet, it’s a worthwhile read for leaders as well as practitioners, who are together charged with shaping how organizations change, day by day and year by year.

Eyes on insurance

Private credit has been all over the news of late, with recent headlines focused on the big increase in requested withdrawals by investors in semi-liquid funds, as concerns fester regarding portfolio loans to software firms and more cockroaches appearing.

But the huge increase in private credit at insurance companies is an undercurrent that needs to be addressed. Assessments of the situation range from “nothing to see here” to the makings of another financial crisis.

In “The PE Sausage Factory,” Phil Bak writes:

Insurance companies that always bought plain vanilla bonds are now being stuffed with private credit originated by their parent companies. This includes exotic structures, JV and LP interests, and on and on.

Insurance portfolios aren’t as boring as they used to be, but they are still regulated on a state by state basis:

As you’d expect, being regulated by fifty different states with fifty different rules and fifty different priorities creates regulatory arbitrage.

Perhaps some state insurance commissions are equipped to handle the changes and properly evaluate the risks, but what are the chances that that is broadly true for a part of the market that barely existed a decade ago and has exploded in size? A Wall Street Journal article about Iowa, where “more life-insurance money is parked” than in any other state, delves into some of the issues, without digging into the state’s ability to assess the emerging risks.

Regarding those risks, dive into a posting from Nick Nemeth for Mispriced Assets and see what you think. At the very least, you’d hope that this whole question is getting a lot of attention from the managers of insurance portfolios, regulators, equity and credit analysts on the Street, and investors.

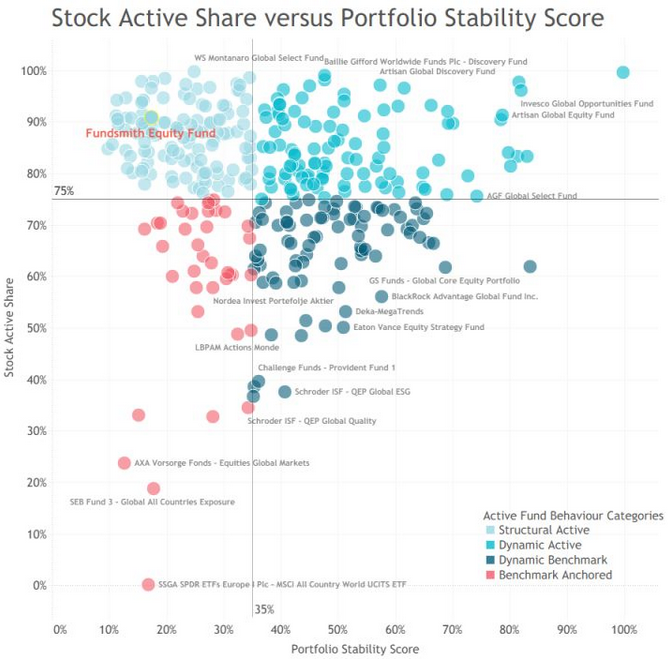

Fundsmith, et al.

Fundsmith has taken it on the chin the last few years, in the market and in the financial press.

When Terry Smith’s annual letter to the fund’s investors was published in January, a number of articles pointed out that it was its fifth consecutive year of underperformance. Joseph Wilkins’ commentary for FT Alphaville was particularly on the nose, pointing out that each year’s letter included essentially the same phrase:

Outperforming the market or even making a positive return is not something you should expect from our Fund in every year or reporting period . . .

Fair enough. Long-term investors should expect variability and periodic underperformance. But Smith’s firm hauled in £160 million or so in fees in 2025 (and similarly lofty numbers in the other years), so the system of rewards seems a bit off the mark. Then there is this from Wilkins:

In his letter Smith says he was “not seeking to ‘blame’ anyone or anything” for his recent results, but then blamed three things for coming up short: index concentration, passive flow dominance swamping active price discovery, and dollar weakness.

Robin Powell of The Evidence-Based Investor disputed Smith’s claim that indexation was the problem, writing that the fund is a factor bet: “When quality stocks outperform, Smith outperforms. When they don’t, he doesn’t.”

Which brings us to the fund’s philosophy (seen here on a placard at a fund meeting): “Buy good companies. Don’t overpay. Do nothing.” The “do nothing” part is shown in the image above from a LinkedIn note by Steven Holden of Copley, which shows that Fundsmith appears in Copley’s “structurally active” segment of managers, who create a “differentiated portfolio built around the same companies over long periods.”

{kind=link}

So how do you think about that when the numbers stay weak? Rupak Ghose wrote about Fundsmith:

Is one year of underperforming a blip? Likely.

Is three years of underperforming a blip? Perhaps.

Is five years of underperforming a blip? Probably not.

To be sure, there are other funds that have held the same general principles and have had similar results (and which have enjoyed the benefits of a lucrative fee model) while they wait for their favored stocks to return to glory. As an investor, dear reader, what do you do in these kinds of situations?

Overconfidence

At the start of a series on building a trading machine, Alexander Campbell referenced his experiences at Lehman and Bridgewater, two much different firms, each of which “beat the ego out of you” in its own way. Interesting cultural snapshots.

He then gets into the matter at hand, putting together a trading system using AI:

After spending what feels like years trying to build systems in conjunction with LLMs, here’s what I can tell you: they’re exactly like first-year analysts/quants/devs from really good schools.

Which brings him back to Lehman and the training he received there. To wit:

Training to say “I don’t know.”

Not because anybody told you to, but because you remembered what happened last time.

AI has no last time.

Which makes the endeavor something other than what people expect.

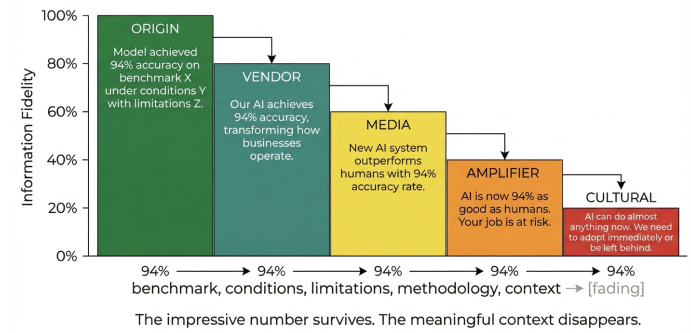

The number survives This image, from “The AI Intelligence Deficit” by Straven & Co., illustrates how a number can survive in popular discourse even as its context disappears. It’s presented here because this happens frequently in the investment world, where beliefs and propositions can be buttressed by numbers, which are often presented without the nuance or asterisks that they require. For a current example, see a piece by Tim McGlinn for TheAtlView regarding a BlackRock estimate that is spreading without its real meaning going along for the ride.

This image, from “The AI Intelligence Deficit” by Straven & Co., illustrates how a number can survive in popular discourse even as its context disappears. It’s presented here because this happens frequently in the investment world, where beliefs and propositions can be buttressed by numbers, which are often presented without the nuance or asterisks that they require. For a current example, see a piece by Tim McGlinn for TheAtlView regarding a BlackRock estimate that is spreading without its real meaning going along for the ride.

The diligence environment

DiligenceVault produced three postings that provide insight into the current due diligence environment:

~ Topics from investment due diligence and operational due diligence roundtables.

~ From the other side of the process, themes from meetings with asset manager investor relations pofessionals.

~ An overview of the vendors providing technology solutions to deal with RFPs and DDQs.

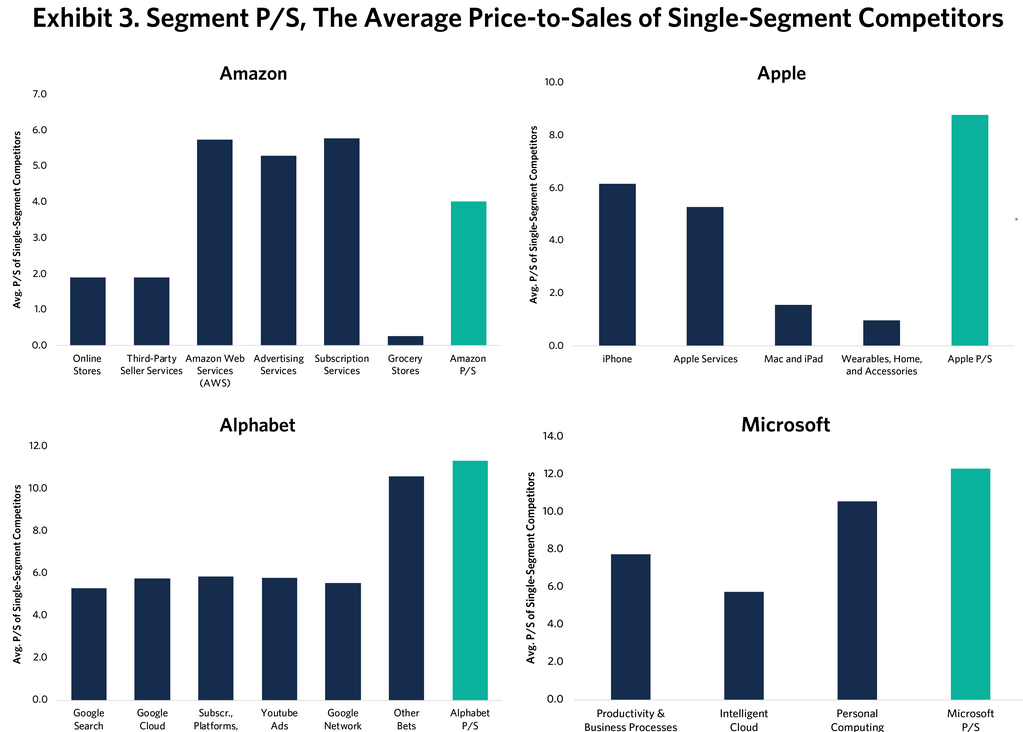

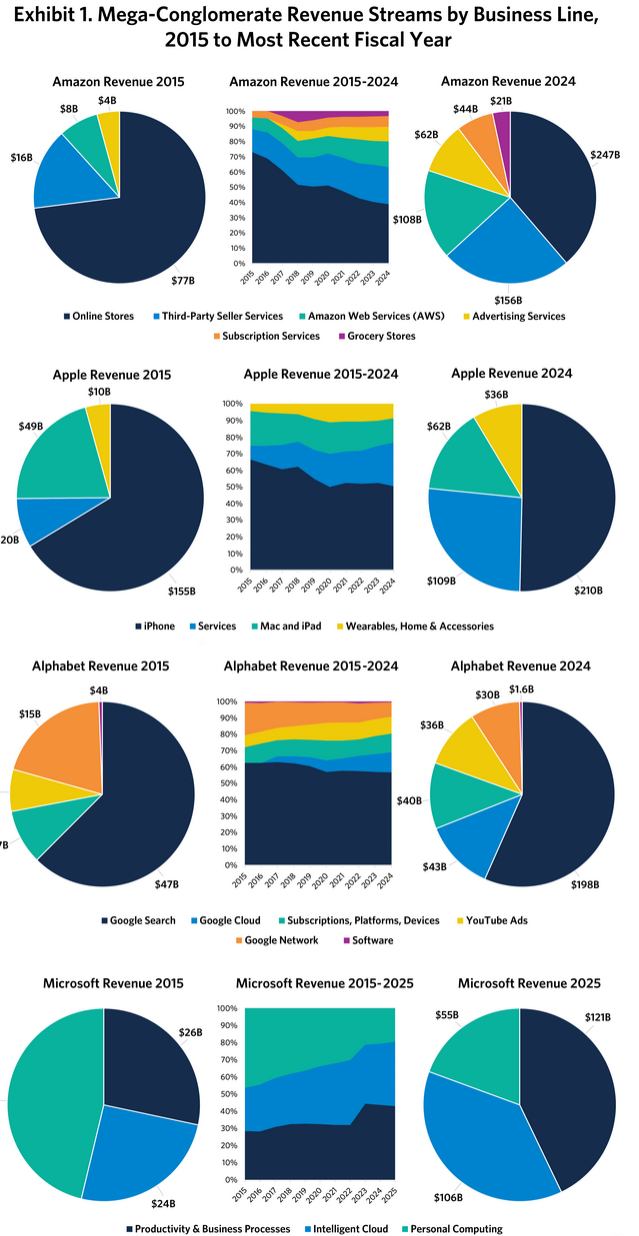

The new conglomerates

Noah Beck and Que Nguyen of Research Affiliates argue that, while conglomerates are generally maligned in today’s stock market, several of them are instead are leading lights within it.

That is a novel assertion, as the four companies in question, shown above, are normally just thought of as “big tech.” Another graphic illustrates how the composition of revenues for the firms changed from 2015 to 2024.

{kind=link}

Given that the tailwinds in technology seem to have abated for now — perhaps even switched to crosswinds or headwinds — will we see the conglomerate discount show up among this group too?

Other reads

“The Franchise Problem,” Earnest Sweat, Groundwork.

[Regarding venture.] What I look for now alongside the fundamentals is harder to put in a spreadsheet. Learning velocity. Proximity to customers. Ability to attract talent. Resilience under ambiguous conditions. Those are not metrics you calculate. They are things you observe over time, in how someone reacts when things break, in whether they are telling you what they think you want to hear or what they actually believe.

“Finding your investment lodestar: In search of an investment philosophy!” Aswath Damodaran, Musings on Markets. The updated third edition of Damodaran’s Investment Philosophies was released today; this posting provides a great overview.

“Ten Years Wasn’t Enough: The Continuation Vehicle Syndication,” Shahrukh Khan, Cash and Carried.

Continuation vehicles (CVs) have rapidly assumed a central role in private equity, transforming from episodic workaround to entrenched liquidity mechanism.

“Culture Is the Human Context Window,” WCM. As AI reshapes work, a look back reinforces what matters most in those kinds of transitions.

“The Architecture of Mutual Fund Pricing,” Stewart Brown, SSRN.

What is not in question is that sixty years of evidence comprehensively refutes the assumption on which current law rests: that independent directors will ensure equitable sharing of the scale economies that investors’ capital makes possible.

“One Risk After Another,” Joe Wiggins, Behavioural Investment. On the “conveyor belt of risks” and “availability cascades [becoming] more frequent and more impactful.”

“No BS: using corporate jargon is really giving you away,” Emma Jacobs, Financial Times.

It is no surprise that ambitious workers encouraged to “fake it till you make it” deploy strings of buzzwords in the hope of career advancement or to deflect attention from shortcomings. After all, the tone is often set from the top, with obfuscating CEOs.

“Anomaly-Driven Demand,” Anders Merrild Posselt and Mads Markvart Kjær, SSRN. On the price impact of anomaly-driven demand.

The course of study

“One could say that my whole career in Wall Street proved one long process of education in human nature.” — Bernard Baruch.

Flashback: Caribou?

A 1980 article by W. Anthony Hitschler in the Financial Analysts Journal was titled “To Know What We Don’t Know (or, The Caribou Weren’t in the Estimates).” It is available via CFA Institute or JSTOR.

Even in 1980 people were trying to figure out why portfolio managers underperformed. Despite the time and effort spent on forecasting, “we can’t forecast the future with enough accuracy to render any forecast more useful than an extrapolation of past growth rates” (which in itself is not that useful). From the abstract:

When investors’ earnings forecasts are close to the mark, they mean very little to the price of the stock; when they are wrong, they mean a great deal.

The caribou of the title refer to the unexpected and large impact on Atlantic Richfield stock because “the caribou’s migrations [required] redesign of the Alaska pipeline.” Hitschler:

The “caribou” eventually visit most stocks, and when they visit one with a very high P/E multiple the consequences can be severe. Yet analysts continue to ignore the great potential of low P/E stocks in favor of a set of forecasts extrapolated from past achievements.

In our era, when low P/Es are hard to find anywhere, the caribou can do a lot of damage.

Reciprocity

A 2023 essay, “The Pull of Reciprocity in Decision Making” — with the help of Cialdini, Munger, and others — explores how the trivial swag and fancy perks of the investment business can sway us. It ends:

Favors are powerful and reciprocity is a foundational aspect of human interaction. Our decisions can be affected in ways that we don’t understand.

Thanks for reading. Many happy total returns.

Published: March 30, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.