The modest entity that produces these postings is located in a suburb of Minneapolis.

The city has been headlining the news for weeks because of Operation Metro Surge (which, despite its name, includes not only the Twin Cities but small towns across Minnesota).

A paramilitary force whose mission is billed as apprehending the “worst of the worst” is doing nothing of the sort, and its extralegal tactics are making a mockery of the Bill of Rights.

That’s the sort of report that normally emanates from a banana republic. (Put that in your model.)

BDCs

Business development companies are in the spotlight these days, which makes it a perfect time for a new paper from David Robinson and Melanie Wallskog, “Why is Private Lending So Popular?” In it, the authors look at BDCs and find that “their growth is intimately connected to growth in private equity” (about 70% of the growth from 2001 to 2023).

The BDC category includes public, non-public finite-life, and non-public evergreen funds, but the authors focus on the public vehicles in their study. Surprisingly, about half of the average BDC portfolio is in “non-bank-like” investments, so they aren’t typical loan books, even though they are often described that way. They also include payment-in-kind vehicles, preferred equity, common equity, and warrants.

The title of a Wall Street Journal article by Matt Wirz describes the latest bit of BDC news to roil the market: “How a BlackRock Loss Reignited Worries About What Is Hiding in Private Credit.” BlackRock TCP Capital wrote down its net asset value by 19%:

BlackRock’s disclosure underscores the risks investors face inside the opaque private-credit world. It can be difficult to know what investments are worth at any given time, given that they hardly ever trade and instead are valued by fund managers using a mix of internal analysis and third-party pricing services. The way private funds mark their holdings determines the fees they charge clients.

A piece by Rod Dubitsky elaborates on BDCs’ reporting practices, the implications for their credit ratings (he believes BDCs are “uniformly mis-rated”), and that the BlackRock overvaluation “isn’t unique.”

In response to the news, Matt Levine fronted his Bloomberg column with a look at BDCs and private credit — and how the current “alts for the masses” push will change things:

Of course the classic buy-and-hold private credit model is supposed to be immune from bank runs, because it has long-term locked-up capital from patient investors. But that’s changing to appeal to retail. And as it changes, it becomes much more important that the marks be correct.

Creditor wars

A Financial Times article by Sujeet Indap begins:

Troubled companies that seek to avoid costly US bankruptcy proceedings by striking controversial deals with creditors overwhelmingly default within three years, new research shows, raising questions about whether the processes do more harm than good.

The research by Mark Roe and Vasile Rotaru takes a deep dive into so-called “liability management exercises,” whereby some creditors take advantage of other creditors through “non-pro-rata deals”:

The prospect of extracting value from others — and the risk of being left behind — distorts incentives. Deals can close even when they do not improve firm value — if the dealmakers gain from nonparticipating or coerced creditors.

Just don’t believe the stories that are told about likely outcomes to justify the transactions:

Non-pro-rata LMEs may well continue at their current pace. Even if they coerce minority creditors, their operational costs could be modest and, in some cases, they may indeed help distressed firms take off. That is the basic pro-LME story. But our results are largely inconsistent with this positive view; most coercive LMEs lead to bankruptcy anyway — the runway, even if extended, is short. LMEs’ promise to strengthen the capital base and prevent bankruptcy falls well short of its proponents’ predictions.

Hedge fund alpha

Rupak Ghose published a posting on “the hunt for hedge fund alpha.” Included is a list of the twenty managers ranked by profits last year:

At first glance, this appears to be a perfectly sensible list of top hedge funds. If you define a hedge fund as an exclusive club that only institutional investors or high net worth individuals can access rather than mom and pop, this list ticks that box. But when I think about what a hedge fund is, it is defined more by how it invests than who its clients are.

Ghose then covers some of the different flavors of hedge funds by looking at several systematic strategies, as well as traditional long-only funds and those that incorporate private markets.

Elsewhere, the title of a Wall Street Journal article by Peter Rudegeair, “Hedge Funds Are Back on Top After a Long ‘Alpha Winter’,” is a reminder that the perception of “alpha” availability going forward is formed by recent nominal performance as well as returns relative to other popular asset classes. The chasing never stops.

On the other side

In the latest report from Michael Mauboussin and Dan Callahan, they ask, “Who Is On the Other Side?” Included are refreshers of topics that they have addressed before, like “What game are we playing?” and the BAIT categories of inefficiencies (behavioral, analytical, informational, and technical).

Among the observations is that “who is doing the buying and selling matters.” Three big trends are covered, including “the massive flow out of actively-managed funds and into index mutual funds and ETFs,” the move to shorter horizons by active managers, and the rise in retail trading. The general principle to keep in mind:

The question you should ask every time that you anticipate excess returns when buying or selling is “who is on the other side?” The goal is to understand your counterparty’s motivation to act and assess whether you have an edge.

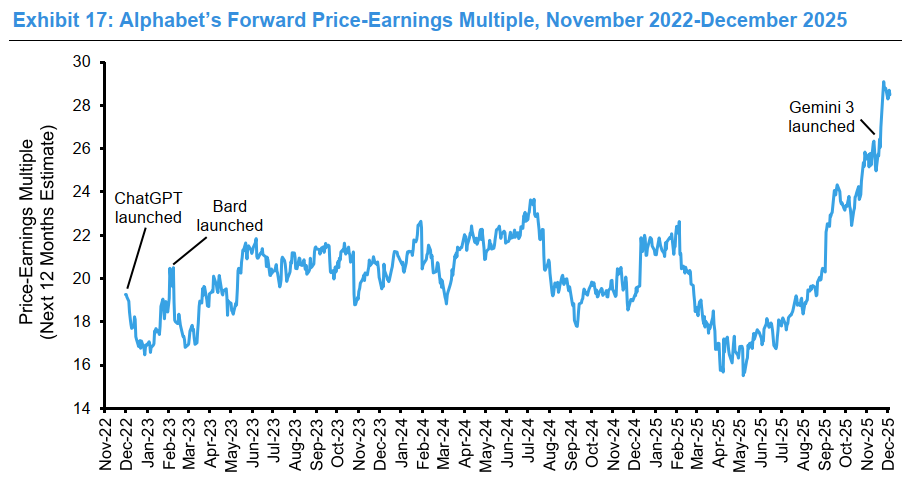

The chart above comes from a section on “the power of narratives,” about how even “very large companies, which are extremely well followed by analysts and reasonably predictable, can see huge swings in value.”

The coming-out party for ChatGPT led to concerns that Google’s dominance in search could be at risk, leading to pressure on the valuation of its parent company’s stock. Yet the multiple almost doubled in a few months last year as it became obvious to market participants that Google was very much a leading player in AI, causing a surge in the stock price. It was, as the authors put it, “a narrative swing from imminent obsolescence to one of inevitable dominance.”

Risks

A report from Harindra de Silva of AJO Vista enumerates ten risks under the title of “Structural Vulnerabilities & Liquidity Illusions.” The theme:

In 2026, the primary market risks are no longer defined solely by macro-shocks (inflation, geopolitics) but by market structure fragility and valuation discontinuities.

The short piece (four of the risks have a few bullet points and the rest are single sentences) is an effective prompt for discussions by teams and organizations regarding possibilities and beliefs.

Clippings

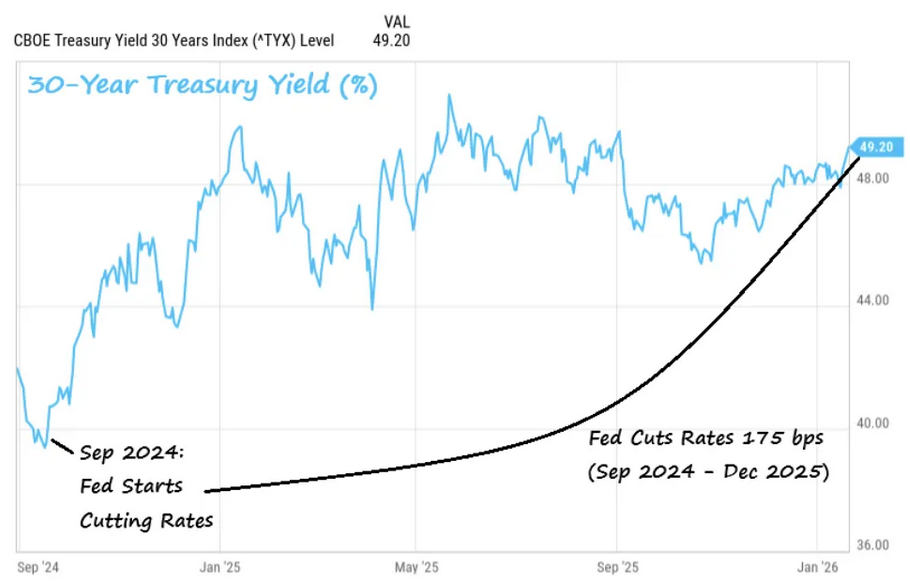

This chart led the most recent edition of Clippings, a Substack newsletter full of interesting snippets from around the ecosystem. (You may sign up for it here.)

The image, from Charlie Bilello, is a reminder that long-term rates, which drive much economic activity, don’t necessarily move in concert with short-term rates. Recent Fed cuts have led to higher bond yields.

Kevin Warsh, the new Fed chair, will have to wrestle with that fact — and with pressure to lower rates from politicians who don’t understand it.

Of related interest: “How the Fed makes decisions: Disagreement, beliefs, and the power of the Chair,” a posting from the Centre for Economic Development.

Other reads

“The quant shop — AI lab convergence,” Grant Stenger and Richard Dewey, FT Alphaville.

One optimises trading revenues, while the other optimises ad or subscription revenues. Under the hood, they share a pipeline — data, model, constraints, execution, feedback — and increasingly a talent pool, a hardware stack, and strict IP norms.

“Oblique Strategies, Giusppe Paleologo, At night we walk in circles and are consumed by fire. Three qualities needed in the AI age: abstract thinking; “people who are good at the human side of things: communication, motivation, and most important of all, listening;” and creativity.

“Fund-of-funds doing secondaries adds conflict on top of conflict,” Jessica Hamlin, PitchBook.

When a secondary investor is both an LP and a buyer in a continuation fund, the sales process needs to be squeaky clean. In many cases, it’s not.

“Winning and Losing,” Ian Cassel, MicroCapClub. Three tribes of losers and two tribes of winners.

“The Total Portfolio Approach Is Still a Human Framework — And That’s the Problem,” Angelo Calvello, Institutional Investor.

Strategic Asset Allocation failed because it treated a dynamic problem as static. Total Portfolio Approach represents incremental progress by acknowledging complexity and expanding the optimization surface, but it remains a more sophisticated hack, not a solution, as it is constrained by the same bottleneck: humans designing rules, selecting factors, and predicting correlations in environments too complex for their ex ante modeling.

“Why Private Equity Is Suddenly Awash With Zombie Firms,” Hank Tucker, Forbes. A tougher environment has stopped the momentum of a number of notable PE firms.

“Everyone Becomes a Bank Eventually,” Covenant Lite.

The last fifty years of non-bank history indicate liability design is crucial. Most non-banks eventually become banks, not by choice but by necessity, when a crisis forces them to seek stable capital and only banks can provide it.

“Worst to First: How IU Football Flipped the Script by Hiring Curt Cignetti,” Kent Wilson, Wilson Talent Solutions. It is arguably the greatest sports story in history — are there lessons to be learned from it that apply to other kinds of organizations?

“This Foundation Invests Almost Everything in Private Equity and VC. How Does It Work?” James Comtois, Institutional Investor.

While most endowments and foundations are working to ensure they have ample liquidity, The Dietrich Foundation is taking the opposite approach. Roughly 90 percent of its $1.6 billion portfolio is allocated to venture capital and private equity — and only 2 percent is in cash.

Reflexivity

“The participants’ views influence the course of events, and the course of events influences the participants’ views.” — George Soros.

Flashback: The yellow keys

Ted Merz was a long-time employee of Bloomberg. On LinkedIn and in his blog, he shares ideas about communication, his meetings with people creating interesting businesses, and, at times, stories from the history of Bloomberg.

He recently wrote about the yellow keys on the original Bloomberg machine, one for each investment category. When the firm was starting out, the only yellow key that worked was for government bonds.

Of course, in a few years the other areas of fixed income and the other asset classes got built out. For those of us that were early users of the Bloomberg, you could see the outline of the future if not the details of it. One of the great business stories of our time and its game plan was laid out at the start. Among many others, the dominant vendors at that moment should have taken the upstart more seriously.

The organizational hairball

A 2023 posting leveraged a “quirky little book with a quirky title,” Orbiting the Giant Hairball by Gordon MacKenzie, to look at how organizational baggage builds up over time and how it is hard to resist inertia even if it’s necessary for future success or even survival.

The posting concerned the need for creativity in the world of asset management. An excerpt:

The asset management business model has been so wonderful for so long that it seems stupid to rock the boat, even if accepting the current condition amounts to rolling the dice on the vagaries of performance-chasing clients in a business where results are dominated by noise.

One of MacKenzie’s concepts applies here. Like people within a bureaucracy, firms find themselves “wrapped in a cocoon of realities” that has evolved over time, which provides a sense of security. But that cocoon “is also a shroud that binds and cripples us.”

Thanks for reading. Many happy total returns.

Published: February 2, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.