“Active management” is a big tent that includes a broad range of strategies and organizations.

For the most part, stories about active management being under pressure concern traditional vehicles like mutual funds and long-only separate accounts. Underperformance versus benchmarks, the relentless shift of assets from active strategies to passive ones, and the increased adoption of alternatives have all eroded traditional active management franchises.

This year, the hundredth anniversary of the first United States mutual fund spawned articles (such as this one from the Financial Times) that were more focused on the passing of an era than a celebration of success. And Morningstar — founded and still best known as a rater of mutual funds — published a piece entitled “The Diminishing Role of Active Mutual Funds,” with a dour subheading: “Active offerings are in a downward spiral of underperformance and outflows.”

Large firms are pivoting into alternatives, firing staff (rarely investment professionals though), and seeking greater scale through mergers, which never seem to work. Smaller asset managers are even more at risk, but they have fewer options available to them (although their size does give them greater maneuverability — if they are willing to adjust what they do).

The problem

The active management business has been so good for so long that there is a strong bias to follow the same path as before. Although change is inherent in a complex adaptive system, other than an increased use of technology, active management looks much like it did a quarter century ago.

Active managers haven’t felt the need to innovate; given the profitability of the endeavor, there wasn’t any great advantage in bucking convention. Consequently, a remarkable sameness came to pervade the craft, with little differentiation from firm to firm and across time. That can be seen by looking at the marketing collateral across managers. It is mostly interchangeable in form, and the stories on offer often seem indistinguishable from one another.

Each manager promises a consistent, repeatable process, selling stasis instead of continuous improvement, as if the job involved pounding out widgets instead of making investment decisions. (That’s a bit unfair to widget-pounders, since the best of them are always figuring out ways to do it better.)

For their part, rather than seeking differentiation and ongoing evolution from their managers, asset owners mostly play the performance game, moving on from a manager who disappoints to another that appears (based upon the current numbers) to have cracked the code, fishing from the same pond in the same way as they have before.

Asset managers are faced with a problem. In the words of Abraham Maslow:

One can choose to go back toward safety or forward toward growth. Growth must be chosen again and again; fear must be overcome again and again.

He was referring to individuals, but the same goes for organizations. Active management, at least in its traditional form, is stuck in a rut, a victim of its own past success. We’ve seen this story before; firms and industries get caught up in their current vested interests and fail to innovate.

(A useful analogy comes from Ted Gioia’s description of the rise and fall of television and movie westerns. His synopsis of the genre’s transition from the dominant entertainment category to that which became old and stale should resonate with investment people.)

Hope springs eternal

“Is this the year for active management?” That is an evergreen question in articles, blog posts, and consultant reports — accompanied by analyses of the conditions that generally make for better or worse short-term active management results.

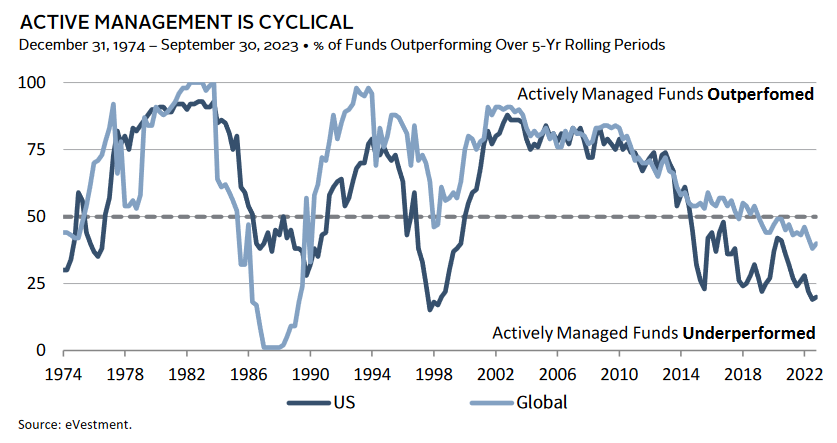

For example, this image is from Cambridge Associates’ 2024 outlook piece, which said, “We believe the landscape is ripe for active managers to reassert themselves in 2024”:

As the title of the chart declares, active management is cyclical. But, as widely practiced, the periods of outperformance are hard to predict, the base rate of success is low, and the results over the last couple of decades look more directional than cyclical. (The down-and-to-the-right slope of the lines over the last two decades is reflective of the compression chart used in our due diligence course. That image presents a stylized view of the wearing away of outperformance over time.)

{kind=link}

Fee alpha

In considering how to improve the results of active management, the easiest lever is the hardest one to pull.

Some refer to the improved performance that can be delivered to investors by lowering fees as “fee alpha.” It is more a release of alpha that would otherwise be retained by an asset manager, since (on average, in most categories) managers outperform gross of fees but not net of them.

Comparisons of low-fee to high-fee managers (again, on average) show better results are produced by those with lower fees. (One illustration of that comes from an exhibit in a Morningstar article.) Despite that relationship, there are plenty of investors who believe that “you get what you pay for.” Intent on chasing down the very best managers, they tend to be trigger-happy, having high expectations and a low tolerance for the normal variability of relative performance.

The ability to lower fees depends on the type of ownership of an asset management firm. Those that are public companies, divisions of public companies, or owned by private equity find it extremely hard to voluntarily reduce fees, while a firm owned by its founder and/or employees has greater flexibility to reposition the firm’s fee structure should they decide to make an active decision that, all things being equal, will improve performance.

Reinvention

The title of this piece is “The Active Management Reinvention Project,” but one size does not fit all, so it really should be “Your Active Management Reinvention Project.”

(“You” and “your” in this are for the readers who are active managers, but the concepts apply more broadly to other entities in the investment ecosystem — and they should be top of mind for those who allocate capital to managers.)

Such a project involves examining and potentially redesigning the interlaced models that define your organization — the investment, operating, client service, and business models which are comfortable and familiar, but which may be out of date and ill-suited to today’s environment, to say nothing of the ones to come.

The goal should not be to create a new state in one fell swoop, but rather to establish an evolutionary plan. Reinvention must be a continual process, not a discreet one. Some changes can happen quickly, but others will (and should) take considerable time. Of critical importance is the establishment of a culture and mode of operation in which innovation is viewed as an essential ingredient for active management success.

Elements

A holistic design needs to consider the full range of important elements, even if some of them are altered only in small ways or not at all. Among the key considerations:

Differentiation and edge. Any review must start with an honest assessment of the current situation, including the interrelated concepts of differentiation and edge.

What do you do that is different than what others do? Where and how do you add value for your clients?

Unfortunately, many managers claim to have an edge but can’t point to any specific differences in their approach that might lead to it. Nor can they persuasively posit why an apparent edge should persist in response to the changing circumstances of the future.

Flipping the previous questions: What do you do that is the same as what others do? Where and how do you fail to add value (or even subtract it)?

Looking forward, what do you think is possible for your organization in terms of differentiation and edge? There are initial limitations imposed by current resources, norms, narratives, and capacity for change, but each of those can be transformed over time. Aspirational goals require patience and persistence.

Dilemmas. Any change process must deal with the dilemmas that, unresolved, can impede excellence over time. Among them, how the goals of asset gathering and effective asset management will be balanced; the desired mix of consistency and change in regards to organizational risk taking; and how the dilutive effects of new product offerings on the resources devoted to existing clients are squared with the benefits of those introductions for the firm.

Culture. An agenda oriented toward change requires a culture that supports it, but many active managers are conditioned to resist bold moves on the organizational front even if that kind of risk taking is embraced within portfolios. There can often be a cultural divide between investment professionals and the rest of the firm — and an inherent tension between the autonomy prized by individuals and the teamwork it takes for substantive change. The pace and nature of developmental change depend on your (real, not advertised) starting-point culture and the gap between it and the desired state at any point in time.

Structure and process. These two need to fit together — and the process must drive the structure, not the other way around. That calls for more flexible and modular ways of structuring an organization so that it can change readily over time, allowing investment process to evolve as needed.

“Process” cannot be thought of as immutable — or marketed in that way. Continuous improvement is the gold standard when it comes to process; if you can’t point to specific ways in which your process has changed for the better over the last few years, it is deteriorating without you realizing it.

Technology. Rapid advances in technology capabilities have changed the possibilities when it comes to structure and process, most notably because of the noisy emergence of AI onto the scene. It would be a mistake to assume that AI will change everything — or that it won’t change anything. Each firm has to decide how to use the new tools, knowing that implementing them in ways that lead to investment or operational mistakes could damage your business.

At a minimum, there needs to be a recognition that the potential for a fundamental change in methods is greater than it has been in decades and — as with any vector of improvement — such potential shouldn’t be ignored, but rather investigated with a willingness to embrace beneficial alterations.

Human capital. Hand in hand with those new technological possibilities comes a requirement to rethink the makeup of roles within organizations and the types of skill sets that are needed. Training and retraining, areas of weakness at most investment firms, need to be invigorated, moving them from inconsistent osmosis-based approaches to ones that are more intentional and appropriate for future needs.

Incentives. Do the incentives in place reward the creation of long-term value for clients and the ongoing improvement of the organization’s capabilities? Or do they incent behaviors that are at odds with those goals?

Investor relations. Your communication efforts need to be reinvented too. You need to be able to break the mold of existing investor relations practice and be thoughtful about the ways in which you can communicate — to help you truly stand out from others and to reinforce the unique aspects of what you do.

There will be pushback by some clients and prospects who think that everyone ought to go through the same drill in the same way. If you can explain why you have chosen to break from convention — and how that relates to your organizational philosophy — you will a) be more memorable than others, b) stand out as a differentiated choice, and c) indicate the kind of independent thought that aids in the building of a long-term relationship that can better weather relative performance cycles.

As with truly active investing, truly active communication pays off. Every aspect of what you do should be reconsidered; differentiation yields dividends.

The power of transparency and authenticity should not be underestimated. Sharing the uncertainties and challenges of the active management endeavor indicates thoughtfulness and honesty, laying the groundwork for trust. Conversely, typical we’ve-got-this-figured-out messages might inspire temporary confidence, but they present an unrealistic picture and ring hollow over time. Every organization has things it needs to do to get better; if you can’t or won’t share what they are with clients and prospects, you aren’t helping them understand who you are as fully as they should.

Of utmost importance is the qualifying of potential clients by giving them a clear picture of what to expect, especially regarding the variability of future performance and the orientation to improvement that will lead to noticeable changes in process and organizational attributes over time. Don’t let the goal of winning the business today get in the way of building a mutually beneficial partnership. That aspect of the typical active management model leads to fragility, not strength.

Advocacy

Asset managers and their advocacy organizations have been stuck defending active management as it is (and has been), not as it could be. For example, although the Active Managers Council of the Investment Adviser Association doesn’t seem to be particularly active itself, it does at times respond to articles that question the worth of active management. But those efforts are sparse and, more importantly, ineffective. (As of this writing, the group’s 2020-2021 communications plan is available online; a permanent link is here.)

A more helpful approach would be to highlight the many ways in which (some) active managers are innovating and how investors can identify them amidst the mass of sameness and mediocrity. Advocacy for active management as we have come to know it is a losing cause, since it doesn’t discriminate between those who are diligently trying to improve and those who are content with the status quo, in which active management is something other than what it ought to be.

Reinvention

Starting with a blank slate is a laudable goal, but you must begin where you are (thus the comments above about current assessments of differentiation and edge). However, having a blank-slate mindset is critical, in that everything should be on the table for reconsideration.

The process will necessarily vary from firm to firm, since there is no single answer to be had. You can’t just grab an apparent success story and try to replicate it. To reiterate: Your goal is to establish a new way of being that is ever-changing and ever-improving, in order to thrive in the ever-evolving marketplace of ideas and investments. That’s what the next era of active management is going to be about.

In every organization there are people who are eager for change and who can see the small things that might make a difference (and the big things too). A (sincere) process of reinvention that is responsive to bottom-up ideas — instead of relying on top-down edicts — rejuvenates an organization and unleashes its latent capabilities.

To be sure, there is risk in change, but there is plenty of risk in not changing, especially when the old model is worn out. It is time to get started on your reinvention project.

If you want to go beyond this high-level summary of the need for change to some practical steps, please get in touch.

Published: July 30, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.