If you aren’t currently receiving these updates via email, you can sign up here. Also, if you are interested in seeing an eclectic mix of charts every now and then, check out our “clippings” Substack, which has a separate subscription. (Both are free, so treat your co-workers too; then you don’t have to keep sending them things to read.)

The self-driving portfolio

Here’s the abstract for a new paper from Andrew Ang, et al.:

Agentic AI shifts the investor’s role from analytical execution to oversight. We present an agentic strategic asset allocation pipeline in which approximately 50 specialized agents produce capital market assumptions, construct portfolios using over 20 competing methods, and critique and vote on each other’s output. A researcher agent proposes new portfolio construction methods not yet represented, and a meta-agent compares past forecasts against realized returns and rewrites agent code and prompts to improve future performance. The entire pipeline is governed by the Investment Policy Statement — the same document that guides human portfolio managers can now constrain and direct autonomous agents.

The opening sentence:

The most binding constraint in institutional asset management is not data availability or model sophistication, but the finite bandwidth of human decision-makers.

Gulp. Well, we knew this was coming. To be clear, there is no proof to be found here (or even the common “proofiness” of returns that are well short of statistical significance but relied upon nonetheless). And the authors point out the risks — including “automation surprise” — from delegating strategic asset allocation to a team of non-human agents.

But this short paper does make you think about new possibilities and the implications for organizational design and the need for different kinds of talent:

The human’s role is not diminished; it is elevated, and the human becomes the architect of designing and overseeing an investment workflow.

Also, it’s worth wondering whether we might be better at analyzing and arranging bots than we are at doing the same with humans; how often does this “guiding principle” really guide our design behavior now?

The guiding principle for when to decompose a single agent into a team is the same one that governs organizational design in human institutions: decompose when the task requires genuinely distinct expertise that benefits from independent reasoning before aggregation.

The spreadsheet challenge

Despite the promise described in the previous section, one big problem needs to be addressed: most nitty-gritty details of investment analysis reside in spreadsheets. Until AI can effectively analyze that source material, the implementation of agentic solutions will be delayed.

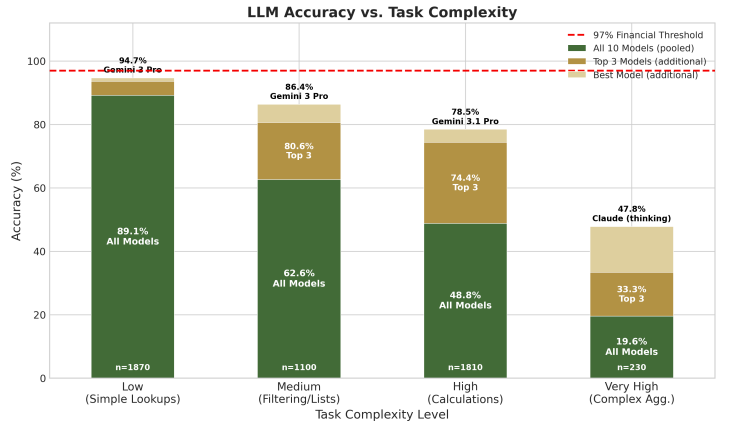

Another paper, “FinSheet-Bench: From Simple Lookups to Complex Reasoning, Where LLMs Break on Financial Spreadsheets,” from Jan Ravnik, et al., studied the current generation of generative AI tools and found them lacking when it comes to spreadsheet analysis:

No standalone model achieves error rates low enough for unsupervised use in professional finance applications.

The authors looked at the process of alternative investment due diligence:

While LLMs can significantly accelerate text-based diligence tasks (document review, clause comparison, compliance checking, and memo generation), a persistent challenge is the extraction of structured financial data from Excel spreadsheets.

The image above shows how their tests of ten current LLM models did on various types of challenges. The dashed red line shows an accuracy threshold for “automated financial workflows,” although that 97% level seems too low when it comes to making calculations.

Judging the implementation of AI within an organization — whether your own or a counterparty’s — means determining what kinds of tasks are being automated and whether the tools available are really up to the job.

The problem with brainstorming

In summarizing a problem with brainstorming sessions, Sunita Sah captures the core issue with meetings in general (yes, including those of investment committees, etc. within our industry):

Traditional brainstorming rewards a very specific skill: thinking while talking. But thinking while talking isn’t the same as thinking well. It just looks like thinking because words are coming out.

In actuality:

The first idea isn’t usually the best idea. It’s just the most available one — whatever was already floating near the surface. Speed retrieves what’s familiar. It doesn’t generate what’s new.

When we reward quick responses, we’re selecting for a very particular kind of thinking: associative, reactive, anchored to what’s already known.

In a meeting, those first ideas (especially if they are delivered by the most senior person in the room) tend to frame the discussion and put it on a trajectory along which other notions are easily dismissed or even left unspoken.

The goal is for exemplary investment ideas to win out in the end, but meetings are often conducted in ways that inhibit idea creation and good decision making. It seems obvious that organizations should want to be good at meetings given their importance in the scheme of things, but they rarely get much attention at all.

Much ado about private credit

The number of pixels published concerning private credit has exploded of late. Here are just a few of the pieces that are worthy of your attention, starting with a memo from Howard Marks, which covers the history of credit investments since the 1970s, the attributes of newly popular strategies that engender overinvestment, and the state of direct lending today.

Areas of concern:

~ “This is What Systemic Risk Looks Like: Athene’s $30B Exposure to Junk Loans,” Rod Dubitsky.

~ “The Hole,” Nick Nemeth, Mispriced Assets.

~ “Private Credit Unfiltered: What’s Behind the Gate,” JunkBondInvestor.

Not to worry:

~ “Why the Private Credit Boom Isn’t the Next 2008,” Larry Swedroe.

~ “Private Credit, Balance Sheets and Financial Stability,” Gregor Matvos, et al., SSRN.

Also:

The US Treasury [on April 1] said it would meet domestic and international insurance regulators over the risks in private credit after recent upheaval in the multitrillion-dollar market.

A certain risk mindset

Alex Turnbull of Syncretica wrote about “non-recourse national strategy,” referencing the risk-taking framework that’s endemic to the venture capital industry:

People who thrive in limited recourse environments develop a very particular relationship with risk. They learn, through repetition and reward, that bold bets on low-probability outcomes are structurally advantaged because the payoff on the upside is uncapped while the downside is bounded. They learn that hesitation is expensive, that deliberation is for people who don’t have conviction, and that the main failure mode is not swinging. They are, in the language of behavioral finance, calibrated to be systematically overconfident in their own ability to identify signal in noise, and structurally indifferent to path dependence because in their world, paths don’t particularly matter — if this startup dies, you do the next one. The option resets.

Turnbull sees the same mindset at work in the United States’ approach to foreign relations. That connection fits with the increasing number of asset owners speaking out about a change in the investment environment, specifically related to geopolitical risks. As one example, Top1000Funds reported that Prakash Kannan of GIC believes that such risks are “no longer episodic or peripheral, but structural, persistent, and deeply intertwined with the functioning of global markets,” with the effect of changing “the operating system of how we think about asset allocation.”

Other reads

“The future of asset management,” Phil Bak, BakStack. A vision of the prospective evolution (revolution?) of the industry, with no fewer than twenty “Then comes . . .” to call out the stages of change.

“The Map That Stopped Working,” Rayna Lesser Hannaway, LinkedIn.

Success is the enemy of curiosity. The longer something has worked the harder it is to ask whether it still will.

“Beware PMs who lack these 3 traits,” Algy Hall, CityWire Selector. Ideas from Clare Flynn Levy, including “the big mistake,” found in Stock Market Maestros, which she authored with Lee Freeman-Shor.

“A Family Office’s Honest Take on Fund I Investing,” Domilė Juozapaitė, Commonplace.

The opportunity is real. Fund Is remain systematically underallocated not because the analysis doesn’t work out — but because most LPs never attempt it. The reason is discomfort. And discomfort is something that can be worked on.

“Are You an Analyst or an Investor?” Ian Cassel, MicroCapClub. Conviction, sizing, and cutting losers; lessons from legendary hedge fund managers.

“Swinging for the Fences: How Do CEO Mega Grants Pay Out for Companies and Shareholders?” David Larcker, et al., Sanford Business.

Companies that award mega grants to their CEO exhibit highly divergent outcomes, with a significant number underperforming and with only a small number outperforming common stock-market benchmarks.

“Unlocking the Answer Library: Turning Institutional Knowledge into a Firmwide Strategic Asset,” Dave Paolisso, CENTRL. Dealing with the bottleneck in client communications for asset management firms.

“Detecting Skilled Bond Fund Managers,” Ron Kaniel, et al., SSRN.

We identify a small fraction of actively-managed bond funds that outperform systematically on a risk-adjusted basis, and a much larger fraction of funds that under-perform.

What matters

“A small bunch of people who know what they are doing can accomplish more than a big group of people who don’t know what they are doing.” — Attributed to Robert Noyce.

Flashback: The right stuff

More than fifty years after we quit sending astronauts to the moon, the crew of Artemis II did a drive-by last week. They landed safely in the Pacific Ocean, but before they did a New York Times article explained that a successful return was dependent on a heat shield that was like the one on the unmanned Artemis I flight, which incurred unexplained damage during its reentry. While the crew was “aware of the flight’s risks,” what could they have been thinking when the capsule hit the atmosphere?

For a story of courage in the face of uncertainty, nothing is quite like The Right Stuff, Tom Wolfe’s book about the first seven astronauts. Most of them had been test pilots who, along with Chuck Yeager, risked their lives to push the boundaries of what was possible. The arresting opening chapter of the book tells the stories of the men who died in the process, one after another, and the wives who answered their doors to receive the bad news. Each time, those that remained “brought out the bridge coats and sang about those in peril in the air” — then went right back at it the next day.

The book provides a mix of the rivalry that drove the space race (the Russians were always ahead in the early days); the competition and comradery among the astronauts; the technical challenges; and the effects of sudden fame (and its unequal apportionment) on them and their families. And their bravery.

At the time, what most people knew about the early space program was all of the rocket failures that had occurred leading up to the first manned flights. So the general impression of the astronauts was visceral:

The main thing was: they had volunteered to sit on top of the rockets — which always blew up!

Imagine being willing to do that.

Explanatory depth

A 2022 essay on this site, “The Goal of Explanatory Depth,” considered the challenge at the heart of due diligence practice — the need for real discovery rather than the acceptance of the narrative that is provided.

The lack of explanatory depth is compounded when that narrative is passed along to others (via an investment memo or presentation) as if it was the product of thorough due diligence rather than a mere repetition of the story that had been offered.

Thanks for reading. Many happy total returns.

Published: April 13, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.