If you’re new to this blog and find it interesting, you can subscribe to receive all new postings via email.

A relatively new sister site provides compilations of good charts and graphs from around the investment world. It’s designed to be viewed in a minute or so. The most recent posting featured the stocks of private asset managers, CMBS delinquencies, and the AI prisoner’s dilemma among other timely images. (A subscription to that site is also available.)

On to the readings.

Thought exercises

For decades, the markets fed on press releases from companies and governments; reports from investment organizations; and stories by mainstream and investment-oriented media outlets. But over time the landscape has changed, principally because of the ease with which individuals and small organizations can put forth ideas online. They can get traction and move markets in ways that wouldn’t have been possible before.

Last week, Citrini Research published a Substack posting, “The 2028 Global Intelligence Crisis.” Billed as “a thought exercise,” it caused downdrafts for stocks in companies that Citrini mentioned as having business models that are at risk from the increased capabilities of AI. The piece amplified an emerging market concern that had already smashed established narratives (and stock prices) across several industries.

Citrini’s thesis has received considerable pushback in the intervening days, including from economists who find its macro assumptions unrealistic. For example, Citadel Securities provided an alternative view of the future, concluding:

For AI to produce a sustained negative demand shock, the economy must see a material acceleration in adoption, experience near-total labor substitution, no fiscal response, negligible investment absorption, and unconstrained scaling of compute.

In addition to reactions to the substance of Citrini’s imagined future, there were comments on the changed information environment. Rupak Ghose reviewed the ways in which sell-side research has a leg up over independent analysts, but also identified six “major competitive advantages” of the independents: internet distribution; broader brand equity (a big change from the days when a number of Wall Street analysts had fame and clout); vastly better storytelling skills; the ability to move across investment themes versus a reliance on “siloed industry verticals;” regulatory arbitrage; and different incentives.

Marc Rubinstein, writing for FT Alphaville, focused on that regulatory arbitrage:

Markets have always found their way around the structures regulators build, and research is no different. Citrini is just the most dramatic expression of where that migration ends up: market-moving distribution with zero disclosure architecture.

One point that should be made: Thought exercises like Citrini’s ought to be part of risk management — and return-seeking — practices within organizations in order to avoid the hardened expectations and narrowed perspectives that limit discovery.

Creatures of the system

The subtitle for a recent interview with Kyle Tucker published on Shahrukh Khan’s Cash and Carried:

What do non-traditional pools of capital in the private markets look like? What long-standing cultural assumptions drive our understanding of “success” in this industry?

The discourse speaks to the dynamics of the institutional investment world and the demands on individuals who find themselves chafing at playing the game as it is structured — a common feeling among professionals that is usually shared only with trusted friends. For Tucker:

I just had a sense that I wasn’t right for the institutional environment. . . . I could fake it for some time, but eventually my motivation would wane, and the wheels would come off.

He bemoans practices on both sides of the table. The gathering of assets is the motivating force of asset managers as they mature (“I’m not sure if the active investment management industry cares about long-term compounding or ever has.”), which necessitates “trying to divine LP astrology” and to “manufacture social proof” to get allocator commitments:

At first, I assumed that the most important thing to investors was money-making. That is, answering and acting on the fundamental question: is this bet a good risk-reward? But I think this is often more like a top two, maybe top three consideration.

One interesting section is in regard to how much to reveal to prospective investors in a business where the narrative is usually burnished to a high sheen:

My solution has basically been (1) to overshare and be transparent as possible (especially the losses, the indignities of firm building, etc.) and (2) try to be as likable as possible (earnest, self-aware, self-deprecating, good-natured, vulnerable, etc.).

Re: oversharing. I think I’m okay with folks seeing too much because I like what we are, and I think we’re really good at what we do (did I mention we’re also humble?).

“We got this right, this wrong. We have this issue” sort of thing.

But candidly, we’ve gotten mixed results here. Some of our LPs love this. But in many ways I underappreciated how much institutional folks value things like tightness of narrative over candor and transparency and oversharing.

Fascinating throughout.

The GP clawback

Adam Schwab published a short piece, “The Next Problem for Private Markets: The GP Clawback,” that warns about a coming “headache for LPs.”

Early wins in 2018-2022 vintages that cleared the preferred return requirement led to carried interest being paid to general partners. But now prospects for many of those funds don’t look so good:

This isn’t a short-term liquidity/uncertainty/volatility issue as claimed by GPs. It’s a “mediocre companies bought at high prices” issue. Many funds are stuck, GPs and LPs know it, and now it’s just a game of when the pain is realized.

The pain involves clawing back those previous payments. For more information, Schwab includes a link to his paper, “GP Clawback Provisions in Private Equity Funds: A Comprehensive Guide.”

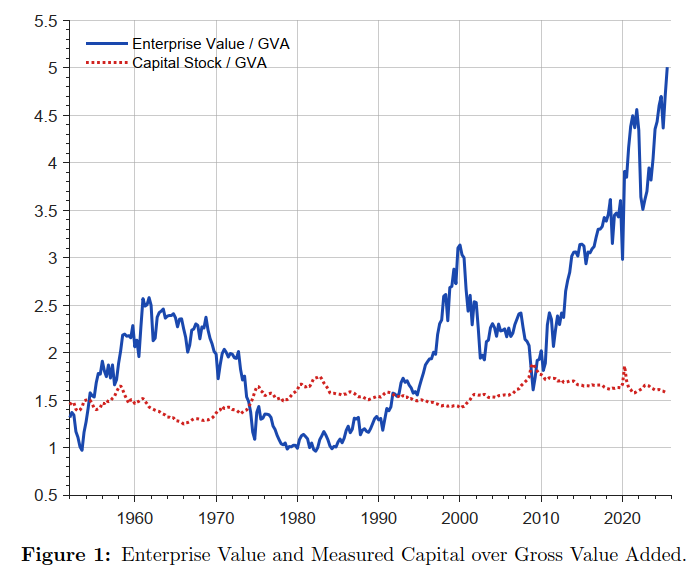

Capital light

This chart was in a report from the Minneapolis Federal Reserve, “A Macroeconomic Perspective on Stock Market Valuation Ratios.” It shows that “the ratio of measured capital to output in the corporate sector has remained relatively stable while the ratio of enterprise value to output has boomed.” From the abstract:

We use macroeconomic data to argue that the observed decline in labor’s share of corporate output in conjunction with relatively weak corporate investment mechanically generates a persistent rise in the ratio of corporate valuation relative to corporate earnings, even absent any changes in expected returns or growth rates.

The same authors — Andrew Atkeson, Jonathan Heathcote, and Fabrizio Perri — also published “Why People Disagree About What Drives Stock Prices,” concluding, “Disagreements about stock market valuation therefore reduce to disagreements about long-run expected returns.”

Guy Spier

The Aquamarine Fund 2025 investor letter starts out as most do, with a review of performance. But then the founder and managing partner Guy Spier admits:

This is not the letter I wanted to be writing — but it’s the one I have to write.

Because of a health issue, Spier decided to return outside capital. The rest of the letter includes an explanation of his medical circumstances, the approach to liquidating the portfolio, a look back at the history of the fund (and the people who inspired and helped him), and his framework for selecting stewards of capital.

Then there are reflections on his health situation, friendships, “how to talk about health to someone who is sick,” and lessons he has learned, making it much more than an investor letter. Ultimately, Spier invokes Hineni (“Here I am”):

I was prepared to play the music of compounding capital for decades to come, but that is not the music I have been given.

Other reads

“Portfolio Design as Gesamtkunstwerk: The Total Portfolio Approach,” Inigo Fraser Jenkins and Alla Harmsworth, AllianceBernstein.

At its heart, TPA is a holistic approach to allocation that rejects the primacy of the asset class or public versus private split as the basis for allocation. Instead, it recasts the task of an allocator to being the curator of return streams.

Manager benchmark strategies, Robert Doyle, bfinance (via LinkedIn). Three kinds of managers and how they act.

“Are Family Offices Trading Freedom for Structure?” John Crabb, Institutional Investor.

The market is evolving, and who’s making that noise about evolution? It’s the usual suspects, the big financial market advisors that worked out the private equity world was saturated, and that families are actually the new golden geese of the investment world. [Quote from Gilles Erulin.]

“Practical Guidance for Fund Directors on Oversight of Alternative Investments,” Mutual Fund Directors Forum. Recommended questions for those providing oversight on alternative funds in mutual-fund wrappers (that may aid those doing due diligence on them).

“Why Static Portfolios Fail When Risk Regimes Change,” Bruno Buriozzi, Enterprising Investor.

Here’s the uncomfortable truth: most institutional portfolios operate under a dangerous fiction — that risk relationships remain stable enough to justify fixed allocation frameworks.

“There’s a punt factor in stocks that investors might be missing,” Rob Mannix, Risk.net. Has the performance of crypto become a significant factor in how stocks move?

“Financial Market Commentators Need the Skills of a Psychic,” Joe Wiggins, Behavioural Investment.

Financial market commentators face a similar challenge to psychics. They are expected to be able to predict the future, but as that is an impossible task they instead have to develop strategies that make it appear as if they can.

“Hidden alpha,” Manuel Ammann, et al., Journal of Financial Economics. Do hidden ties between fund managers and corporate officers result in alpha generation?

“The Empathy Delusion: Why Many Financial Advisors May be Making the Riskiest Bet of Their Careers,” Dan Haylett, LinkedIn.

The advisors who survive and thrive will be the ones who treat AI not as a threat to defend against, but as a capability to master.

“The New Leadership Equation: The Market Rewards Results-Oriented CEOs with a Collective Focus,” Receptiviti. Among public company CEOs, “high agency is effectively universal,” while “communion” varies widely and “correlates with value creation.”

A real team

“A team is not a group of people who work together. A team is a group of people who trust each other.” – Simon Sinek.

Flashback: A rigged Nasdaq

Byrne Hobart wrote an interesting post on Capital Gains, revisiting a time when stocks were traded in eighths of a point and Nasdaq market-makers wouldn’t quote the odd-eighths so that they could enjoy fatter margins. He provides links to an academic paper and an SEC report about the practice.

For the most part, person-to-person trading seems like a long-ago thing, although there are still some markets where it comes into play. Here is some good prospective from Hobart about the differences in “market color” between the two types of trading:

Manual trade execution is a job where information gets transmitted in two forms: by prices, and by people sharing interesting tidbits with one another over the phone. For a market-maker, these rumors are generally about who’s selling and how much. If you’re a buyer, you care whether the big seller who’s pushed the price down this morning is a random fat-finger trader or a big fund exiting a position. You aren’t supposed to know the details, but “market color” is a fuzzy concept. In the voice trading era, it was more common for this to leak out directly, and to go to favored counterparties. Today, the same kind of information still exists, but it’s in aggregated, anonymized from — prime brokers produce reports on positioning, sentiment, and general market behavior, which puts individual counterparties on a more level playing field.

The corporate life cycle

A book by Aswath Damodaran triggered a posting a year ago about the corporate life cycle. One snippet:

Walking through the life cycle, Damodaran covers a range of investment strategies, providing evidence about their effectiveness and observations about the gaps between theory and practice. For instance, in venture investing, pricing mistakes tend “to spiral up and down the pricing chain,” so that “one new round of overpricing or underpricing can spawn many more rounds of overpricing or underpricing.” (That “me-too” behavior in corporate finance? It’s endemic among professional investors.)

Thanks for reading. Many happy total returns.

Published: March 2, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.