In addition to content, The Investment Ecosystem offers consulting, training, coaching, and facilitation for investment organizations and professionals. For more information, see our website to schedule a virtual meeting.

The most recent posting on the site, “The Advisory Dilemma: Personalized or Systematic?” deals with the important decisions that advisory firms must make in terms of the nature of their services.

A blank slate

Here’s your assignment: Manage a pool of $47 billion, starting from scratch.

That’s the job that John Barker, chief investment officer of the Mastercard Foundation, has, as outlined in an article from Institutional Investor. Not only constructing the portfolio but building the organization.

What would you do if you were in his shoes? How much would your solutions to this unique opportunity mimic what everyone else is doing?

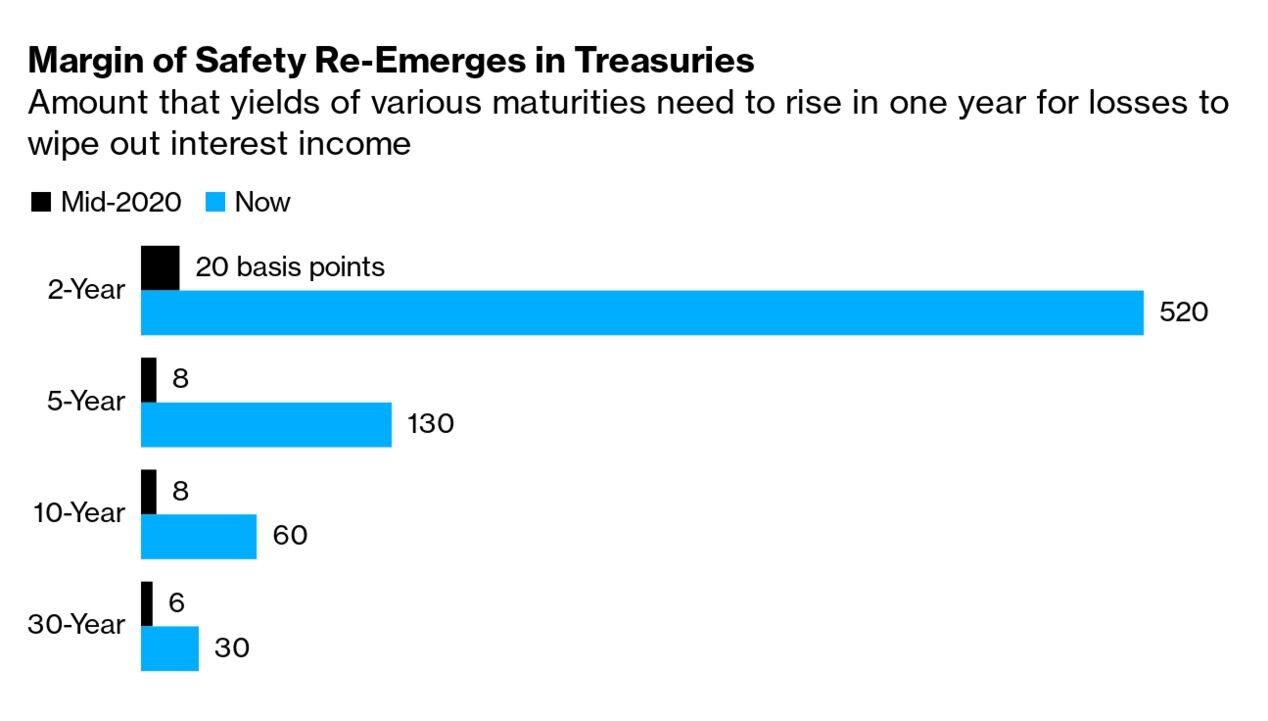

Changing circumstances We all know that markets are continually evolving, even though we sometimes act as if we can lock down an approach that will work for all time. The above image came from Bloomberg. It shows the dramatic change versus four years ago in terms of the effect of increases in Treasury yields on the prospect for positive (nominal) returns.

We all know that markets are continually evolving, even though we sometimes act as if we can lock down an approach that will work for all time. The above image came from Bloomberg. It shows the dramatic change versus four years ago in terms of the effect of increases in Treasury yields on the prospect for positive (nominal) returns.

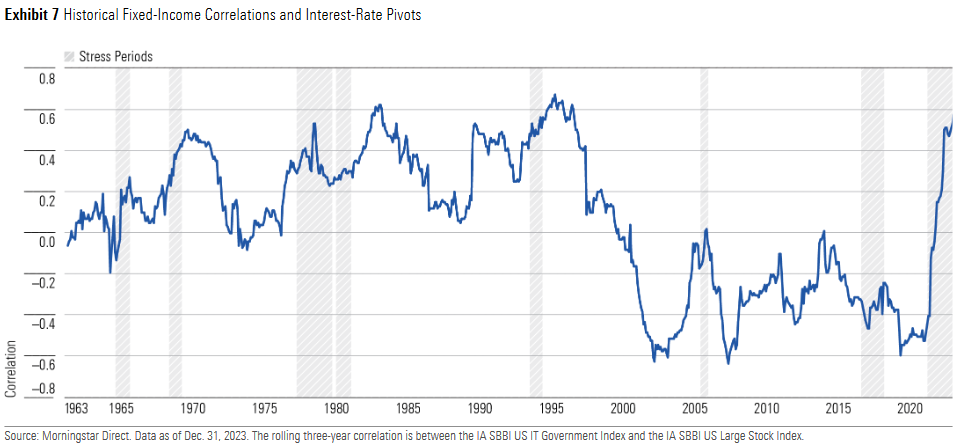

Other reminders of fundamental changes come from Morningstar’s “Diversification Landscape 2024” report. Here’s its sixty-year look at the correlation between Treasuries and large stocks:

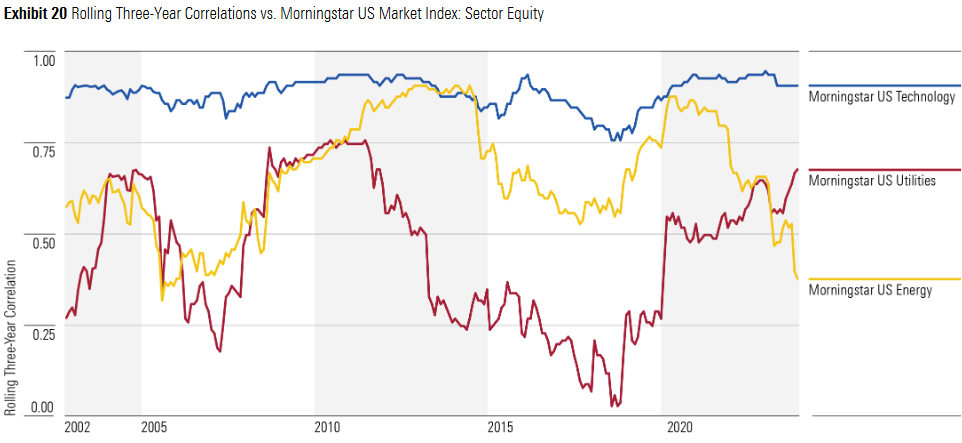

And one since 2002 that shows how significantly two equity sectors have varied in correlation to the market (and that technology has not):

For a longer view, Bryan Taylor went back to 1251(!) to divide the past into five financial eras and twenty historical periods. (Paper here.)

For a longer view, Bryan Taylor went back to 1251(!) to divide the past into five financial eras and twenty historical periods. (Paper here.)

Each period is separated by geopolitical events, such as the end or beginning of a war (1815, 1914, 1945), a stock market bubble (1720, 1929, 2000), a secular low or high in interest rates (1896, 1981, 2020) or similar events. These events signal a change in the zeitgeist of the period and consequently a change in the returns to stocks, bonds, bills and the equity risk premium.

We have found that high returns in one period are followed by low returns in the next period and vice versa.

Taylor places us in the era of globalization, which he has beginning in 1982. However, he breaks that era into three periods, the latest starting in 2020, the title of which heralds a potential shift to a completely different era: de-globalization.

Deepfakes

Angelo Calvello wrote an opinion piece for Pensions & Investments, “Deepfakes — the next threat for investors.” A video example created for demonstration is included, plus some plausible scenarios in which a deepfake could be used to fool investors. Particularly troubling:

Deepfakes are created by using deep learning technologies (hence the “deep” in “deepfake”), often generative adversarial networks (or GANs). Yet, despite the complexity of the underlying technologies, almost anyone can manipulate videos, audio and images to create deepfakes without the need for extensive programming skills.

The emerging risks point out the need for good operational due diligence:

Because allocators and managers depend on third parties (custodians, fund administrators, brokers, etc.) to provide critical services, their due diligence process should include a rigorous assessment of the vendors’ digital security policy and procedures.

Legends

Jim Simons, the iconoclastic founder of the mysterious and wildly-successful Renaissance Technologies, passed away at 86. Gregory Zuckerman, who authored the book The Man Who Solved the Market about Simons, wrote a remembrance for the Wall Street Journal. Ted Merz summarized Simons’ five very short guiding principles. (In 2017, the New Yorker published a very good article on the research center Simons created after leaving the active management of Renaissance.)

“Woodstock for capitalists” — the Berkshire Hathaway annual meeting — was held on May 4. The absence of Charlie Munger (who, according to Warren Buffett, was peaking when he died at “the age of 99.9”) and Buffett’s own advanced age gave the meeting a different feel than in years past. In a poignant moment, a boy asked the question, “I’m wondering if you had more day with Charlie, what would you do with him?” Here’s the video.

Debt

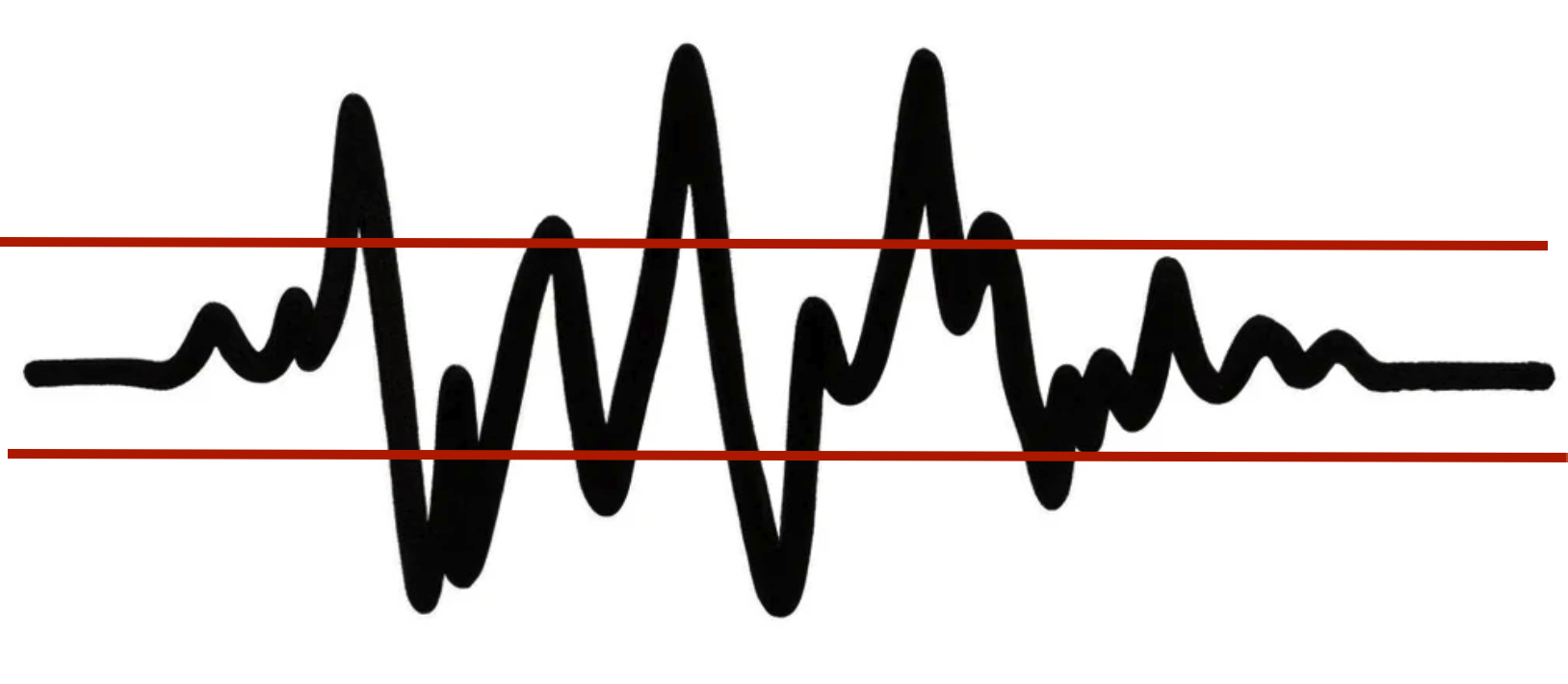

Morgan Housel wrote a posting about debt and the volatility of life (“Not just market volatility, but life world and life volatility: recessions, wars, divorces, illness, moves, floods, changes of heart, etc.), using a series of simple images, including this one:

The black lines stay the same, but one image has very wide red bands (representing how low levels of debt mean that the effects of the volatility are largely a non-issue) and one very narrow ones, which present a different state entirely.

Seeing the posting prompted Howard Marks to write a short essay on “The Impact of Debt.” The use of leverage is a factor in the management of companies and of portfolios, and attitudes about it vary significantly over time in response to changes in the environment.

Other reads

“The Curious Case of Catalysts,” Joe Wiggins, Behavioural Investment.

There are problems in each of these components — we are poor at making predictions about future events, we aren’t great at forecasting the reaction of other investors, and things are never constant. Other than that, we are all set.

“Big Tech Capex and Earnings Quality,” John Huber, Base Hit Investing. How will the huge increases in capital expenditures by the big tech companies affect their returns (and investor perceptions of them)?

“The OCIO Mirage & Investment Office Costs,” Charles Skorina.

If the goal is to deliver superior performance, service, and solutions and be there for multiple generations and perpetual institutions, who is most likely to endure and deliver?

“Looking for the exit: Oregon battles overweight allocations to illiquids,” Sarah Rundell, Top1000funds. One example of how a fund adjusts its portfolio construction in response to the denominator effect (private market assets at the Oregon Public Employees Retirement Fund are now 55% versus the target of 40%).

“Don’t tell me how I am doing,” Joachim Klement, Klement on Investing.

Your performance tends to improve if you stop comparing it to other investors or some arbitrary benchmark. If you focus only on your investment process and what you can control, you are less stressed about your investments and give them more time to create long-term performance. You are less likely to sell assets that may go through a temporary drawdown, and you feel less pressure to just invests in what has worked most recently.

“These 4 pillars are the ‘SOUL’ of organic growth,” Joe Duran, Citywire RIA. A simple framework for the next generation of advisory firm leaders.

“Carried Interest: Assessing Current and New Methodologies on Valuation,” Johnson Associates.

By understanding the current value of carry awards, firms will be able to more accurately determine all-in economics across traditional compensation and carried interest.

“Can Machines Time Markets?” AQR. Thoughts on whether “small, simple models — not complex machine learning models — are best suited for market timing applications,” or whether “astronomical parameterization” offers new possibilities.

“Common Investor Relations Representation,” David Volant, SSRN.

I find common IR representation increases common institutional investor ownership, overlap in sell-side analyst coverage, and similarities in guidance practices across clients — even among economically dissimilar firms that operate in different industries.

“IFRS Accounting Standard Will Support Better Investment Decisions,” Nick Anderson, Enterprising Investor. Companies subject to IFRS will be rolling out changes to their financial statements over the next three years.

Success

“If your work is unfulfilling, the money will be too.” — Jerry Seinfeld, via Ben Carlson.

Flashback: A tsunami of change

The brokerage industry underwent a time of significant change in the late 1990s. Once upon a time there were mid-sized firms who were very influential with asset managers and instrumental in bringing firms public. Most of the notable ones were gobbled up by banking firms in a relatively short period, including these which agreed to be acquired in 1997 alone: Alex. Brown (by Bankers Trust); Robertson Stephens (BankAmerica); Montgomery Securities (NationsBank); Wheat First (First Union); and Piper Jaffray (U.S. Bancorp).

Within a couple of years, the dot-com boom had turned into a bust and the banks were cutting back on those research operations (and in some cases being bought themselves).

In 1999, Goldman Sachs said goodbye to 130 years as a partnership and became a public company. An article by Joshua Franklin details some of the twists and turns in its quarter century, including the switch from a brokerage firm to a bank holding company during the financial crisis.

Postings

The archives include all of the previous editions of the Fortnightly, as well as essays on important ideas from different pockets of the investment ecosystem. Here’s an example of an posting from December, “Identifying Unrealistic Expectations in Manager Selection.”

Thank you for reading. Many happy total returns.

Published: May 13, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.