A new series of postings, “Three Books about Capital Allocation,” has started with an essay about Ana Marshall’s The Climb to Investment Excellence. Two other books will be covered, each different in content, style, and perspective.

To get email notices of future postings, sign up here. You may comment (for the editor’s eyes only) by responding to an email or sending a note. And now, some great things for you to read.

Conviction and Quality

Josh Tarasoff of Greenlea Lane Capital Management wrote a wonderful piece about conviction and quality. The first part explores two kinds of conviction — explicit and implicit — which “often exist in tension.” Tarasoff clearly explains and provides examples of each type, detailing how they can come into conflict in investment decision making by supporting “opposite conclusions.”

In practice:

It isn’t difficult to see why the investment industry is inhospitable to implicit conviction, and why its partner rules the roost. Implicit conviction forms of its own accord and cannot be planned. It defies quantification, eliciting the charge of being too “fuzzy” to matter. Nor can it be fully captured in words. Implicit conviction is impossible to transmit from analyst to portfolio manager or from portfolio manager to client, which is highly inconvenient for the business of managing money. It is primarily personal. It is quiet. By contrast, the appeal of the explicit is clear.

Tarasoff then links that dichotomy to explore a related concept:

I will use “Quality” (capitalized to distinguish it from the ordinary sense of the term) to indicate the deeper-something on which implicit conviction is based.

Using the term in that way “pays homage to the work of Robert Pirsig,” the author of Zen and the Art of Motorcycle Maintenance. (A series on a predecessor site to the Investment Ecosystem connected challenges in the investment world to the themes of the book.) Tarasoff covers the role of intuition and pattern recognition; “the complexity inherent in any company”; and how the superficial and ephemeral aspects of a firm conveyed in words and schematics are ultimately less important in the long term than the cultural values that drive it.

Theory and practice

The latest research from Michael Mauboussin and Dan Callahan is “Cost of Capital and Capital Allocation,” which focuses on the theory of corporate behavior regarding those topics as compared to actual practice. To illustrate the discrepancies, they use the “easy money” period of thirteen years ending in 2021 with the similar time frame that preceded it.

The authors bifurcate charts into the two periods to show the actions of companies regarding investment activity, debt to total capital, excess cash and marketable securities, and buybacks. The evidence supports the belief that “executives make financial decisions that stray from the ideal of creating long-term value for continuing shareholders and instead focus on maximizing earnings per share.”

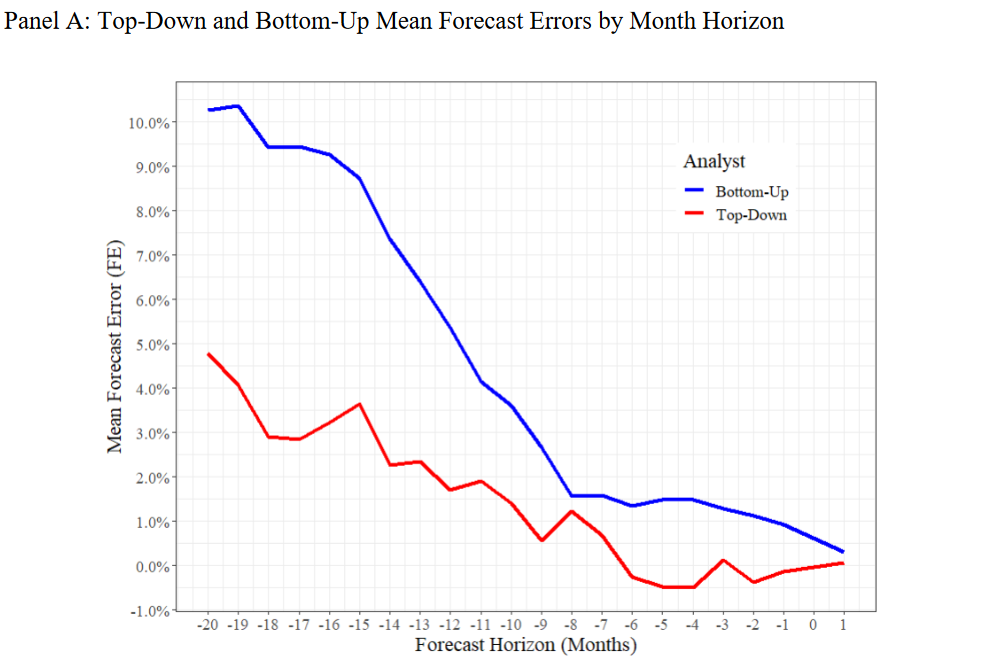

Top-down versus bottom-up

Markets are forward-looking and, while changes in valuation often drive prices in the short term, earnings are the ultimate anchor for returns. Therefore, a lot of energy goes into forecasting earnings for the S&P 500 and other indices.

Two types of numbers are quoted by professionals: Top-down projections by strategists and the bottom-up aggregation of analyst estimates for individual companies. Which is more accurate? That’s the topic of “Top-Down vs. Bottom-Up Index Forecasts: Are Market Strategists Strategically Pessimistic?” by Min Park, et al. Both kinds of forecasts err on the high side, but strategists as a group are somewhat more pessimistic, as the chart above indicates.

The degree of that relative pessimism varies over time, because the forecasts of strategists are more sensitive to the macro environment. As a result, the relationship between the two series “has significant information content in predicting future earnings surprises and stock returns.”

Factor dustup

Mary Childs and Justina Lee published an article for Bloomberg, “Upstarts Challenge a Foundation of Modern Investing.” It concerns changes in the famous Fama-French historical data that underlies much factor investing — and the academic dustup surrounding it, specifically a couple of papers published by a trio of University of Toronto researchers. The debate about it spilled over onto what’s left of Twitter, with Cliff Asness calling the authors “pissant nobodies” while referring to Fama and French as “OG finance researchers.”

It all is a reminder that the evidence for “evidence-based investing” changes over time, mostly because of evolutions in the market but also due to adjustments to historical information, especially from much-earlier periods.

(One sidebar to the story is the involvement of Dimensional Fund Advisors in the data updates. Also of interest: Dimensional commissioned famed filmmaker Errol Morris to create a ninety-minute documentary about the fund company, “Tune Out the Noise.” The access code is MARKETSWORK.)

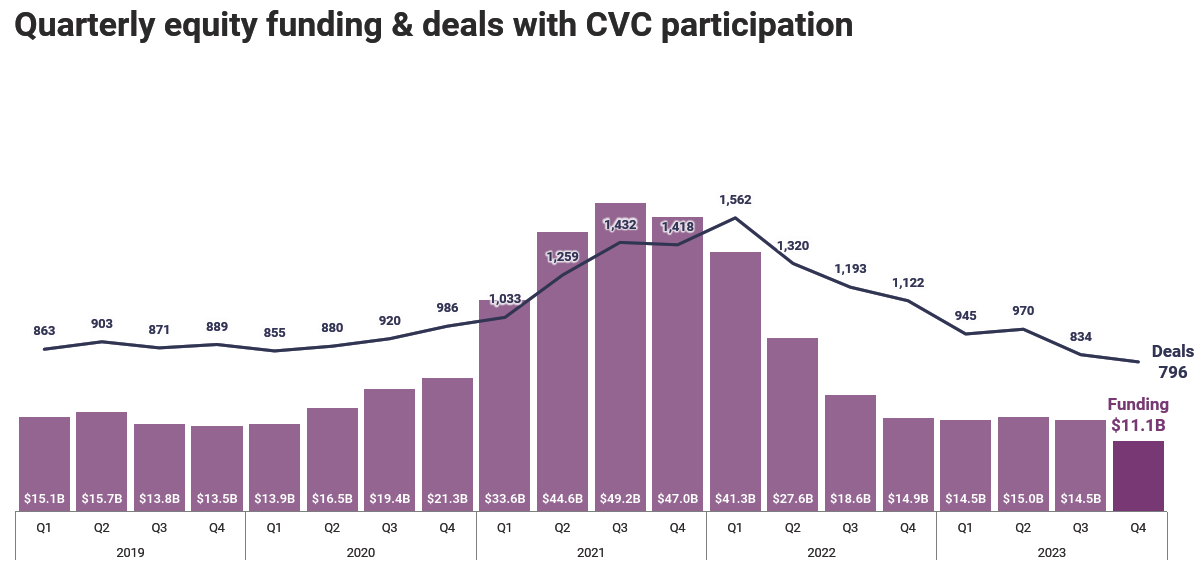

The pig(s) in the python

This image comes from a CB Insights report, “State of CVC” (corporate venture capital). It looks like most every other chart of VC investment, with a huge bulge in 2021 and the first part of 2022, as everyone rushed to the trough at once.

This image comes from a CB Insights report, “State of CVC” (corporate venture capital). It looks like most every other chart of VC investment, with a huge bulge in 2021 and the first part of 2022, as everyone rushed to the trough at once.

In addition to the corporate investors pigging out, there were the VC funds (and their limited partners) and a number of mutual fund and investment trust managers. In response to the news that Scottish Mortgage was buying back its own shares because of the discount to stated NAV, Robin Wigglesworth of FT Alphaville wrote:

If the Baillie Gifford-managed investment trust was so concerned about share price-NAV discounts, perhaps the better move would have been to mark down the value of its huge private company holdings to something closer to what the market clearly thinks they’re worth?

Related: One working paper found that from 2000-22, “All the performance metrics examined show that funds incorporating VC fail to outperform.”

Risk management

Risk management is often viewed as a quantitative activity, but forward-looking, qualitative imaginings should be at the heart of it. A question: Is the sun on your list of concerns? (Yes, that giant ball in the sky.)

Homework for your next risk management meeting: “What a Major Solar Storm Could Do to Our Planet,” an article in the New Yorker by Kathryn Schulz. The electronic world that has come to envelop our lives is ill-suited for one aspect of the natural world we inhabit.

An important case study of historical precedents, changed circumstances, odds, and possible consequences.

Other reads

“Memos,” Sriram Krishnan. A great collection of examples.

I’m fascinated by interesting memos written for an internal audience — a company, a campaign or even for the President. Raw, not smoothened over for PR departments, they help shed light on how people really think inside institutions.

“The Outsourcing of Kodak’s Pension: “They Worked Themselves Out of a Job’,” Alicia McElhaney, Institutional Investor. The outsourcing of the function once headed by the legendary Rusty Olson illustrates how the investment of corporate defined benefit plans has changed.

“Growth Equity,” Lubomir Litov and William Megginson, SSRN. This short paper provides a reminder that new categories of investment are always emerging — and addresses how the use (and study) of this one has evolved.

“Lifetime Financial Advice,” Thomas Idzorek and Paul Kaplan, CFA Institute Research Foundation.

This book proposes a practical, integrated three-stage model for financial planning that not only embraces life-cycle finance but also integrates it with single-period optimization models.

“The NACUBO Endowment Study: A 50-Year Retrospective,” Commonfund. Documenting “a period of unprecedented change,” including shifts to total return investing, different kinds of external managers and advisors, alternative investments, and “responsible investing.”

“Times Change: The Era of the Private Equity Denominator Effect,” Massimiliano Saccone, Enterprising Investor. Thoughts on the traditional playbook for those who are overweight (and overcommitted for the future).

“The Great Paradox of the U.S. Market!” Jeremy Grantham, GMO.

[Investors are] predicting near perfection; yet we face in reality not just a very risky disturbed geopolitical world, with growing concerns about democracy, equality, and capitalism, but also an unprecedented list of long-term negatives beginning to bite.

“What’s on the Minds of ODD Professionals,” DiligenceVault. Among the issues: cybersecurity, fee structures and disclosures, Gen AI, and ripple effects from changes in lockup provisions and continuation vehicles.

“Prime brokerage: the multi-billion dollar cash cow redefining banks’ trading divisions,” Christopher Whittall, IFR.

Despite the vocal scrutiny from the regulators, we’re surprised to still see some fairly aggressive behaviour from banks competing on margin terms that we wouldn’t agree to. We don’t think that’s prudent or sustainable in the long term.

“Is There A Way out of the ESG Rock Fight for Boards?” Lawrence Cunningham and Anna Pinedo, Across the Board. The “polarized debate . . . obscures the genuine and legitimate benefits of longstanding ethical business practices.”

They come with the territory

“Never promote a man who hasn’t made some bad mistakes, because you would be promoting someone who hasn’t done much.” — Herbert Henry Dow.

Flashback: Explosions on Wall Street

We’re not referencing stocks that explode higher or those that explode into nothingness, but real explosions. In 1891, according to Wall Street: A Pictorial History, a Boston broker “entered the office of Russell Sage, the millionaire moneylender,” and demanded more than a million dollars or he would set off ten pounds of dynamite. Sage refused and the man followed through on the threat, killing two and seriously injuring five (but not Sage, who had “made a dash for the door).”

In 1920, a horse-drawn wagon filled with a hundred pounds of dynamite and an estimated five hundred pounds of metal was blown up in front of the J.P. Morgan building at 23 Wall Street as the noon bells of Trinity Church finished ringing. 38 people died and hundreds were injured in what is considered one of the first terrorist attacks, which was believed to be perpetrated by Italian anarchists.

In 1993, a bomb was set off in the World Trade Center and eight years later the Twin Towers were destroyed as terrorists once again targeted the locus of American financial power.

Postings

The archives include Fortnightly postings like this one, plus in-depth postings on important investment topics.

For example, check out a couple of postings from two years ago, “Building an Organization Oriented to Improvement” (picking up on research by Michael Mauboussin and Dan Callahan) and “Angles of Discovery for Due Diligence,” which uses that foundation as a way to understand how (or if) an organization is getting better all the time.

Thank you for reading. Many happy total returns.

Published: March 18, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.