The last posting here, “Inside a Powerful Narrative Creation Machine,” is one of the most popular ever. It concerns Bridgewater, a fascinating case study of leadership and organizational behavior. While it is unique in many ways, questions about analyzing that firm apply equally to other asset managers.

To receive emails whenever a new posting is released, subscribe here.

And now, a great crop of readings for you.

Investment motivation

Christopher Schelling wrote an intriguing posting on LinkedIn, “Theories of (Investment) Motivation,” that provides a series of interlocking ideas for assessing private asset managers.

The first part of it involves the never-ending question of whether to rely on historical performance for selection decisions. Schelling:

One tenet of investing which we are all taught is that past performance is not indicative of future returns. That may be true; however, past behavior is the strongest predictor of future behavior.

Regarding the decline in persistence for buyout firms over the past two decades, Schelling thinks that the academic work illustrating that downtrend is flawed, since those responsible for the initial returns often leave to start their own shops; following the people rather than the brand is a better way to judge persistence.

For all involved (and, for all of us, period), there are intrinsic and extrinsic motivations that drive behavior. On the extrinsic side of things, the paydays come from performance on the one hand and asset fees on the other. Schelling argues that managers should be evaluated on what he calls the “X Ratio” (for extrinsic), which compares the variable compensation and capital gains of the general partner to its cumulative fixed fee income (historically and/or prospectively), in order to assess the proclivity for a performance orientation versus an asset gathering one.

He also calls for the use of an “i Ratio” (the small i standing for intrinsic), based upon the personality profiles of the general partners involved (ascertained through online tests). That kind of assessment is uncommon and, for some at least, controversial. But Schelling uses the output of work he has done in that regard to show how personality profiles vary across venture capital, buyout, and growth equity firms. Importantly:

There was often a high degree of correlation between the i Ratio of the team and the relative contribution of the respective driver of returns, and the higher that correlation, it appears the higher the persistence of return for those managers.

Put together, these thought-provoking ideas should prompt further examination by those involved in due diligence and manager selection.

Technological disruption

A new paper from Alistair Barker, Ashby Monk, and Dane Rook is titled “Technological Disruption and Long-Term Investors: Managing Risk and Opportunities.” For most asset owners, technological disruption “has no consistent role in their core processes for assessing, monitoring, and handling risks to their portfolios.” The emergence of artificial intelligence as a potential disruptive force highlights the ongoing need to consider how incumbent positions in a portfolio might be affected negatively and new exposures might be added when such dislocations occur.

Four significant hurdles impede the implementation of a coordinated approach to anticipating and dealing with disruptions: disengaged leaders, who don’t see how disruptions can be tracked, managed, and capitalized upon; the prevailing mindset (“institutional investment organizations are rarely set up to be innovative; their governance and resourcing structures are geared around incremental changes to the portfolio and organization”); fragmentation of portfolios and teams; and misaligned incentives.

The authors outline a framework for going beyond conventional industry, sector, and asset class categorizations to establish a research function that acknowledges the way technological disruptions can fundamentally change the investment landscape and shatter the boundaries of existing practice.

Private credit gaps

A decade ago, you couldn’t find a bucket for private credit in the asset allocation schemes of hardly any asset owners. Now it’s the talk of the town.

Many smaller allocators of capital continue to ramp up their exposure or are just getting started. And even some behemoths are still adding; Reuters reported that six of Canada’s biggest pension funds (more about them in the “other reads” section below) “have begun a major expansion into private credit.” According to the FT, wealthy individuals also are investing more in the area, in part because “real estate does not have the shine it had before.”

But there are reservations and differences of opinion about how the strategies (there’s a mix of them under the broad umbrella) will perform in different interest rate environments; an FT article includes conflicting views from some large pension plans.

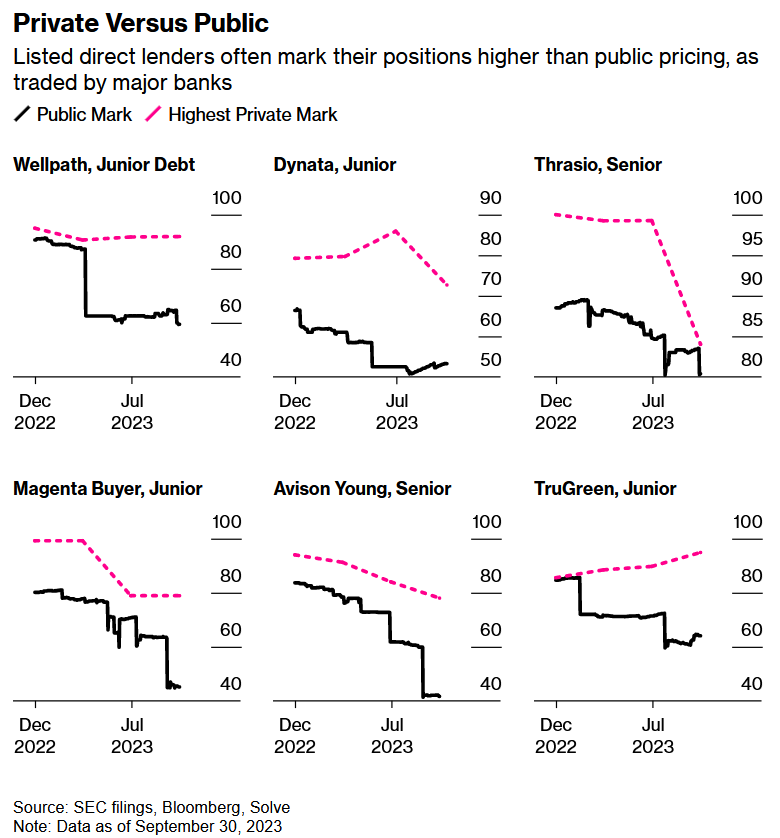

Of great interest is a recent Bloomberg piece, “Flawed Valuations Threaten $1.7 Trillion Private Credit Boom,” which includes the above illustrations. The gaps speak for themselves.

Crypto factors?

Sparkline Capital’s latest research report concerning “crypto factor investing” contends that the debut of Bitcoin ETFs “marks a symbolic embrace by the financial establishment,” signaling that “Crypto is now for adults.”

That said, “As skeptics are quick to point out, the small-cap space is rife with hype, vaporware, and outright scams.” Nonetheless, Sparkline parses the universe and charts four factors akin to those popular in the equity realm: market, momentum, small-cap, and intangible value.

At FT Alphaville, Robin Wigglesworth takes the other side of the trade, calling it all “deeply silly” (while complimenting Sparkline’s other research output). As to the rush from big name firms to get a piece of the action:

It’s incredible that this needs to be spelt out, but the only reason why the likes of BlackRock, Fido, JPM and the Big Board have gotten involved is because they are in the money extraction business.

Place your bets.

Evolving perceptions

Vontobel published an article, “A question of perception: how quality investing evolves over time,” that tracks how the notion of “quality” has changed over the years. As the chart’s title notes, perceptions change, “adapting to the market sentiment of the time” — a foundational principle of investment behavior.

Other reads

“Private Equity’s Second(ary) Act,” Phil Huber, Cliffwater, via LinkedIn.

The secondary market has matured over the last several decades into a robust and dynamic ecosystem fueled by growing investor demand for liquidity, portfolio optimization, and strategic capital deployment.

“A Perspective on Private Equity NAV Loans,” Peter von Lehe, et. al, Neuberger Berman. This includes descriptions of generally positive, neutral, and negative examples of usage of NAV loans for acquisition financing, capital infusion, and accelerated distributions.

“On the Sustainability of the Canadian Model,” Eduard van Gelderen, SSRN. Investment beliefs, asset allocation groupings, and some possible changes ahead for the “Maple-8.”

“Embracing difference: Why investment teams must be cognitively diverse,” Simon Hoyle, Top1000Funds.

Cognitive diversity does not automatically arise in a team just because it has a range of subject-matter experts. And sometimes it’s a diversity of cognitive skills that allows specific subject-matter expertise to be linked together in new and productive ways.

“The Ripple Effect – Finding Company Connections from Detailed Estimates,” Liam Hynes and Temilade Oyeniyi, S&P Global. Can alpha come from something as simple as leveraging the co-coverage of firms by sell-side analysts?

“Buffett and Three Hedge Funds,” Roger Lowenstein, Intrinsic Value.

[Citadel, Millennium, and Point72] regard investors not as partners but as pigeons. They practice their own form of socialism (socialism to benefit the privileged, mind you), extracting a tax on the owners of capital. Berkshire is different.

“A Structural Alpha Opportunity,” Ben Nabet and Joe Auth, GMO. Mismatches in credit ratings versus default risk in securitized credit, including three case studies.

“How to Overcome Performance Pressure,” Brett Steenbarger, TraderFeed.

The higher profile the trade — i.e., the greater the perceived opportunity — the more room there is for performance pressure. As Epictetus observes, the issue is not the “real problems” about the trades, but rather the “anxieties” about those trades.

“Seasons of Finance,” Byrne Hobart, Capital Gains. The day-to-day workings of many investment jobs change throughout the year according to regular patterns, as exemplified by this posting regarding stock analysts.

‘You Have Time,” Ian Cassel, MicroCapClub.

We sprint at new ideas like it’s the last cup of water in a desert. The result is most microcap investors rush into things too soon.

“2023 RIA Risk Survey,” Golsan Scruggs. This well-conceived document shows survey results regarding ten risks, plus short definitions of each one, questions regarding the management of the risk, and the legal substantiation for paying attention to it.

The whole problem

“The whole problem with the world is that fools and fanatics are always so certain of themselves, and wiser people so full of doubts.” — Bertrand Russell.

Flashback: Robert Noyce

In 1997, Forbes ASAP published “Robert Noyce and His Congregation,” a piece by Tom Wolfe which included a new introduction fronting an excerpt from a 1983 Esquire article by Wolfe about Noyce’s pivotal roles at Fairchild Semiconductor and Intel. (The Internet 1.0 look of the article is appropriate — long-dead ASAP was one of the earliest magazines devoted to the “Information Superhighway.”)

Wolfe found his theme in the mores of Noyce’s hometown of Grinnell, Iowa and of the Congregational Church, where, “To all intents and purposes, there were only two social classes: those who were hard-working, God-fearing, church-going, and well educated and those who were not.” The contrasts between the culture that was created in Silicon Valley — “paved entirely by geniuses from the Midwest and farther west” — and the prevailing model of corporate leadership and hierarchy of the day were sharply drawn by Wolfe.

The article ends with this summary of Noyce:

He wasn’t a boss. He was Gary Cooper! He was here to help you be self-reliant and do as much as you could on your own. This wasn’t a corporation . . . it was a congregation.

Postings

In the archives, you’ll find all of the previous editions of the Fortnightly, as well as essays on important ideas from around the ecosystem. For example, a series of postings about Talent, a book by Tyler Cowen and Daniel Gross, and ideas regarding human capital in the investment world.

Thanks for reading. Many happy total returns.

Published: March 4, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.