The last posting covered the evolution of the institutional investment consulting business, as reviewed by Richard Ennis in his book Never Bullshit the Client. It also touched on his views about a number of topics of importance to asset owners, which will be further explored here.

Since 2020, Ennis has written a large number of articles that challenge the assumptions of investment practice as commonly implemented. Most of them can be found in the blog section of his website and on his SSRN author page; some of the links below are for articles that appeared in academic journals.

A critique

The first article, coming a decade after his retirement from EnnisKnupp, appeared in the Journal of Portfolio Management: “Institutional Investment Strategy and Manager Choice: A Critique.” It begins:

Institutional investors speak in reverent terms of the importance of sound policy as the foundation for their work, but that is not what drives them. Institutional investors’ passion has always centered on identifying profitable opportunities and having the skill to exploit them.

That tension is at the heart of Ennis’ body of work, especially as it relates to the widespread use of alternatives — and the philosophical allegiance to the endowment model by almost all asset owners (and their advisors) today:

Diversification, per se, is not the problem. Institutional trustees are fiduciaries, and prevailing diversification patterns are a manifestation of how they interpret their fiduciary duty. In other words, observed diversification is an institutional fact of life. The problem is the combination of extreme diversification and high cost: a recipe for failure.

The article presaged many of the themes to come in later pieces, including the data shortcomings that make it difficult for clear and consistent evaluation of performance of alternatives, the disappearance of their diversification benefits over time, and their lagging performance versus passive exposures over the ten years ending in 2018 that were the subject of the study. (As he would in subsequent writings, Ennis used returns-based style analysis to evaluate performance.) Of the 46 public pension funds analyzed, one had statistically significant positive alpha while seventeen had statistically significant negative alpha. In aggregate, the funds underperformed by 0.99%. Educational endowments also trailed, by 1.59%. (An October 2023 piece, “Endowments in the Casino: Even the Whales Lose at the Alts Table,” furthers the analysis of them.)

Debates with Siegel

In 2021, Ennis exchanged a series of articles with Larry Siegel — two each that were published in the Journal of Investing (all included together here) and one each in the Journal of Portfolio Management (here are the pre-print papers from Ennis and Siegel). Quotes below (and characterizations of the content) come from those six sources.

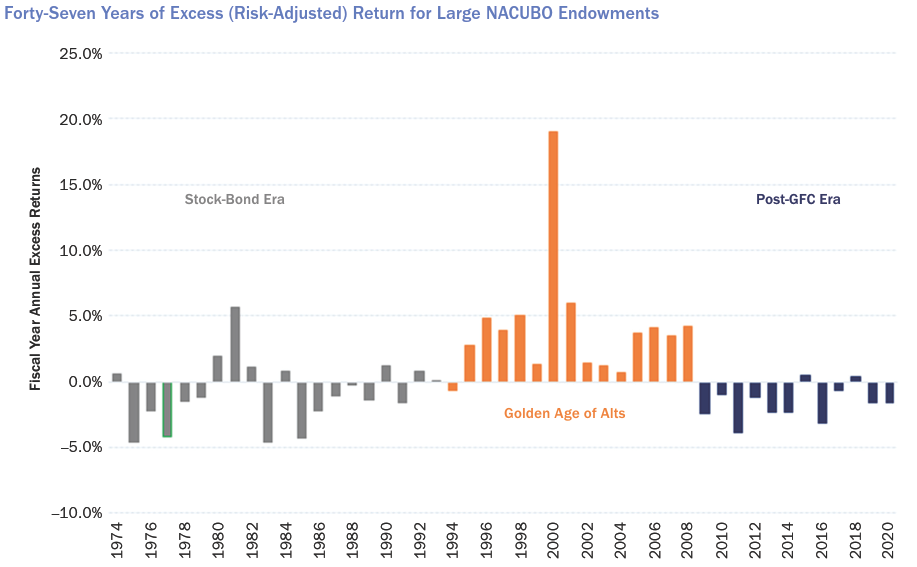

Ennis argued that there was a Golden Age of Alts that essentially ended with the financial crisis. Here’s what the yearly excess returns looked like for large endowments:

During that time there were huge increases in assets under management in alternative investments. Ennis wrote, “As a result, pricing in all three of those markets [hedge funds, buyout funds, and real estate] became better aligned with public-market pricing.” That speaks to one of the most overlooked aspects of investing, that not only do investor flows follow performance, but performance follows investor flows, as buying pressure changes the valuation of the underlying assets (and thereby affects prospective returns). Investors who focus on performance often miss the transitory nature of that effect. It was during that Golden Age when the belief in the endowment model spread in earnest.

According to Ennis:

Trustees of public pension funds and large endowments in the United States are in a bind. With the help of staff, consultants, asset managers, assorted pundits, and a media chorus, they have rationalized dividing their portfolios into as many as a dozen subportfolios . . . [and] made allocations to so-called alternative investments, or alts, that are vastly disproportionate to the alts’ representation in the marketplace, . . . with more than 100 investment managers, which they compensate to the tune of 1% to 2% of the value of their assets each year. None of this is working for them, and certainly it is not working for the stakeholders of these funds.

In contrast to the conventional wisdom, Ennis wrote that there was no diversification benefit and no alpha contribution from those alternatives after the financial crisis. But there were high costs, plus over-diversification from a proliferation of managers, which led to a cancelation of active bets across portfolios and little chance of finding enough outperformers.

Siegel acknowledged the post-financial crisis underperformance, but held that the advantages offered to those who embrace the endowment model argued for a return to better days:

Endowed institutions and other investors, if they choose to be active rather than indexed, can benefit by considering as potential investments every asset class and strategy in the world. Such unconstrained investing is supported by finance theory, which says that constraints on active bets are always costly in terms of return, conditional on the active management in question being successful (adding alpha) in the first place.

As they say, there’s the rub. Who really meets that condition? What percentage of those who are practitioners of the endowment model can pass that test?

Siegel does a good job of explaining that you need to believe that successful managers exist and that you have the ability to identify them. If that’s the case, you should take every advantage of your skill and opportunity, willingly investing in vehicles and strategies that are difficult for others to take on, including those “between the asset classes or outside of them.” (And, if not, he like Ennis favors indexing.)

His careful defense of the endowment model is a limited one, dependent on prerequisites, and he knowingly cites the “parody version” of it: “Anything worth doing is worth overdoing.” Whether we are at (or past) the point of overdoing is a valid concern.

In response, Ennis said that Siegel tried to make “a case for endowment exceptionalism,” which he thought was suspect based on both theory and evidence. The overall discourse between them provides a useful debate for asset owners and their agents to consider.

Benchmarking

Ennis took on the “black art” of benchmarking in “Lies, Damn Lies and Benchmarks: An Injunction for Trustees.” Of asset owners:

They use benchmarks of their own devising, typically referred to as strategic (or custom) benchmarks. Most exhibit significant benchmark bias, meaning the chosen benchmarks underperform ones that, in fact, better represent a fair economic return given observed market exposures and risk characteristics.

The purpose of a strategic benchmark evolved over the years: “Its original intent was not to supplant the passive benchmark, but to augment it for insight into the merit of strategic decision-making and execution.” But,

As practice evolved, passive benchmarks have largely gone by the wayside in public reporting. They have given way to a new breed of strategic benchmarks, which are often highly customized to fit portfolio circumstances.

Ennis recounts the long list of problems with many of those benchmarks, including complex constructions, inconsistent practices, the mixing of different kinds of return measures, lagged performance of some asset types, non-investable components, and benchmark changes directly derived from the weightings of the asset components themselves:

Strategic benchmarks are invariably subjective in their construction, often complex, ambiguously customized, fluid in composition, opaque, and all but indecipherable to readers of financial reports.

In addition, many funds are “chasing slow rabbits,” since the overall risk of the benchmarks they use are persistently out of whack with that of the plan assets.

Another problem:

Having the CIO and/or consultant, who are responsible for designing and implementing the investment program, also do the benchmarking and reporting is a clear conflict of interest and a sign of weak governance. As a gauge of financial performance, strategic benchmarks are an economist’s worst nightmare.

And those benchmarks and their subcomponents are usually used to determine bonuses for the CIO and other staff members (and influence whether a consultant continues to be retained).

Ennis included tables that compared the reported benchmark returns for representative pension plans and endowments, which are below those of returns-based style analysis by more than a percent, allowing for easy performance comparisons — and an appendix that looks specifically at CalPERS. (See also a recent study by other authors regarding private equity portfolios, which indicated that over the last two decades “benchmarks for US public pension funds have become easier to beat.” Moving the goalposts.)

Bringing it together

As part of a story by Douglas Appell in Pensions & Investments, Ennis bemoaned the groupthink of the “chief investment officer-consultant-asset manager complex.” All of those actors benefit from increased complexity — the question is whether the addition of alternatives and other kinds of complexity add value for the ultimate beneficiaries of the assets.

In “Excellence Gone Missing” (link), Ennis recounted the progression of the investment profession over the last sixty years, and repeated his beliefs, highlighted above and in the previous posting, concluding:

Missing from institutional investing today is excellence. Complexity and supposed sophistication abound. But these are not the same as excellence.

“Hogwarts Finance” (link) also detailed the “magical thinking” involved in common asset allocation policies today. An appendix gives the recent history of the benchmarks for the New Mexico Public Employees Retirement System, which illustrates some of the issues noted previously.

“Disentangling Investment Policy and Investment Strategy” (link) addressed the distinctions that Ennis has made throughout his career between those two things. He quotes a 1977 Financial Analysts Journal article by Doug Love to make the distinction:

Investment strategy presumes that markets are not efficient and concentrates on which risks to take and when in exploiting perceived inefficiencies. A strategy has value for as long as it takes for it to be employed by others. An investment policy, on the other hand, is a decision with an indefinite (though not infinite) time horizon, taken with regard to the ability to assume investment risk. The investment policy task is to determine how much risk to take as a matter of principle, independent of current outlook.

Without a clear distinction between investment policy and investment strategy, however, it is not possible to effect a meaningful division of labor between professional investors and their clients.

The emphasis was added by Ennis, who wrote:

Investment policy is the domain of trustees. It is the expression of the institution’s risk tolerance and liquidity requirements. It describes what an investment manager needs to know about its client before embarking on portfolio management. Investment strategy is the domain of investment professionals attempting to add value through various forms of active management. The two should not overlap.

He thinks that the proper division of duties is lacking at most asset owners. And, perhaps surprisingly given his former role as the head of a prominent investment consulting firm:

I do not believe any funds should operate with the traditional trustee-consultant model, in which the consultant advises trustees in connection with strategic decisions (as well as policy) and in performance evaluation. Under this arrangement, the consultant faces insurmountable conflicts.

Instead, he thinks that “all trustee groups, regardless of asset size or the sophistication of their investment staff or OCIO, should use an independent consultant” to advise the trustees on policy, aid in the selection of an OCIO if one is needed, identify an appropriate passive benchmark, monitor performance and compliance with the policy statement, and provide unconflicted education to trustees. And stay out of the strategy business, which has proven to be irresistible:

Like moths drawn to a flame, consultants have long been eager to have a hand in strategy. Many among them now quietly acknowledge the conflicts of interest they face, realizing that they have been co-opted professionally by a combination of forces: (a) clients’ unceasing eagerness to beat the market and (b) the awesome power of the investment management industry in selling its services.

Finally, in “An Open Letter to Investment Consultants” (link) Ennis provides a summary of advice for the consulting profession, which “can play an important role in helping its clients improve performance.”

Questions

The P&I story said:

Some asset owners view the rethink Ennis is almost singlehandedly pushing for now as a useful, much-needed exercise after a decade or more when allocations to hedge funds, private equity, infrastructure and now private debt have continued to accelerate at the expense of traditional exposures to publicly traded stocks and bonds.

Others see Ennis as more Don Quixote, tilting at windmills, than caped crusader.

Whether your inclination is to agree or disagree with his views, the ideas put forth by Ennis are of great importance and should be front and center for fiduciaries. Here are some questions worth asking at your next meeting:

Factoring in all costs, why do we think that alternatives will outperform going forward? Are our views distorted by one “golden age” of performance and/or the pressure of institutional behavior?

Given the lack of consensus about how to judge the performance of alternative assets, does our current approach for doing so make sense?

How have our alternatives and overall portfolio performed in comparison to passive portfolios with similar risk profiles?

Are we among the group of allocators that can identify managers who will outperform? Is there evidence of that? What will allow us to do so in the future? What will inhibit us?

Do we use a consistent benchmark of passive vehicles that reflects the overall volatility preferences identified in our investment policy?

Do we need to rethink our governance approach?

What common practices of asset owners are leading us to unwise decisions?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Published: December 10, 2023

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.