This edition of the Fortnightly is a week late (we took the show on the road for a bit), but it has a full load of great reads for you from around the investment ecosystem. Back on schedule; you’ll see the next version in two weeks.

NAV loans

The opening line of a posting from Ted Seides speaks to an evergreen investment industry experience:

Financial market participants tend to stretch at the end of a cycle in ways that look silly in retrospect.

The topic is NAV loans, via which private equity sponsors borrow against their funds, a practice that is suddenly in vogue given changed circumstances in the industry. The title of the piece asks, “Canary or the Gold Mine?”

Given that first sentence, you think the answer must be “canary,” but then Seides relates some examples that make you think he’s going to come down on the “gold mine” side. Before choosing, he puts forth both the “pro” and the “con” arguments, making the case that NAV loans might work out well in some cases and be disastrous in others. That said, Seides comes down on the side of listening to the canary; he echoes the words of Ana Marshall of the Hewlett Foundation that “anyone hearing about a NAV loan should shout out a warning from the mountaintop.” Attention must be paid.

For more on this topic, see a Financial Times article which reported that the Institutional Limited Partners Association is drafting recommendations that “call for the industry to provide justification for the loans and more disclosure of their costs and risks to investors.” And a Bloomberg piece throws shade on NAV loans and other borrowing tactics that are becoming more prevalent by referring to them as “backroom financing.”

Due diligence

Hilary Wiek of PitchBook has issued a report, “An LP’s Guide to Manager Selection,” which delves into some of the nuances of due diligence and manager selection in private strategies. She follows the industry preference for “the Ps,” offering six of them as the foundation of her approach — people, philosophy, process, portfolio construction, performance, and pricing — while adding a seventh, potpourri, that allows her to include some other important points.

The report is full of good questions to pose to general partners, including some that are “culturally delicate to ask.” Wiek stresses that “all [of a manager’s] responses must form a holistically coherent picture” and gives some examples of ways in which they often don’t. Each of the seven sections includes helpful perspective for the diligence quest.

In the end, it is critical to remember that “there is no one right answer to any of the areas of due diligence” and that “it is the allocator’s fiduciary duty to perform its own due diligence, even if it seems like smarter investors have already done so.”

CEO rewards

FCLTGlobal published “The CEO Shareholder: Straightforward Rewards for Long-term Performance.” According to the paper:

Companies need to reward leaders who create long-term value, but focusing on short-term returns as the primary metric in remuneration keeps companies stuck in short-term behaviors.

It argues that total shareholder return — which has been institutionalized as the primary approach to incentivizing CEOs (and others at a firm) over the last few decades — is a poor way to align the interests of managers with those of investors. The organization’s theory of “remuneration design” is explained in the body of the report; a five-part “toolkit” at the end provides a nice summary of the practical application of it.

Charles Feeney

A remarkable life, making money and giving it away.

Other reads

“Generative AI: Overview, Economic Impact, and Applications in Asset Management,” Martin Luk, SSRN. The table of contents to this long piece offers codes for the sections to indicate “must-read,” “read if you can,” and “helpful to read.”

“Investing Is a Science, an Art, and a Practice,” David Booth, Dimensional.

Financial economics is a social science. Unlike math, which demands proofs and delivers exact answers, research in finance yields insights. These insights allow room for interpretation. And putting theory into practice requires judgment. In many ways, it’s similar to medical science.

“Doing this will improve and accelerate your analysis,” Stephen Clapham, Behind the Balance Sheet. Analysts, when was the last time you read an audit report?

“Hedge funds do not offer value to pension funds and other investors,” Michael Rosen, Angeles.

There is no combination of stocks and high-yield bonds that did not outperform hedge funds.

Fees are simply too high a hurdle for hedge fund managers to offer an attractive return to investors.

“10 Quotes That Shaped My Investment Philosophy,” Barry Ritholtz, The Big Picture. Only one of these is specifically about investments, yet they represent a solid philosophical foundation for investing.

“The Business of Annual Letters,” Byrne Hobart, Capital Gains.

A company has a story to tell that’s best told in the form of a serialized short-term company history with near-future speculative fiction elements. But all of those stories come to an end sooner or later.

“Politics rivals profits for portfolio influence, says Bridgewater co-CIO,” Aleks Vickovich, Top1000funds.com. This was written before the recent events in the Middle East; even now, are politics more import than profits? Over what time horizon?

“Adapting to Growing Private Markets: A Playbook for Practice Success,” Asher Cheses and Daniil Shapiro, Cerulli. “Advisors can use alternative investments to differentiate practices and attract, consolidate, and retain client assets.” (Note that the belief that a “lack of correlation to public markets” is given as a selling point.)

“The paradox of private credit,” Jared Gross, J.P. Morgan Asset Management. (Also see: “Insurance Companies Binged on Private Credit. Moody’s Is a Little Worried About It.”)

Private credit has “grown up” in a period of low interest rates, inexpensive leverage and limited defaults but must now adapt to an environment of high rates, costly leverage and rising credit risk.

“The alpha of ugliness,” Robin Wigglesworth, Financial Times. Thoughts on some academic papers comparing the looks of portfolio managers and analysts with their performance. (Maybe AI tweaks can help the prettier among us come across as “ugly beta nerds.”)

Topics of interest

“Great minds discuss ideas; average minds discuss events; small minds discuss people.” — Eleanor Roosevelt.

Factors over time

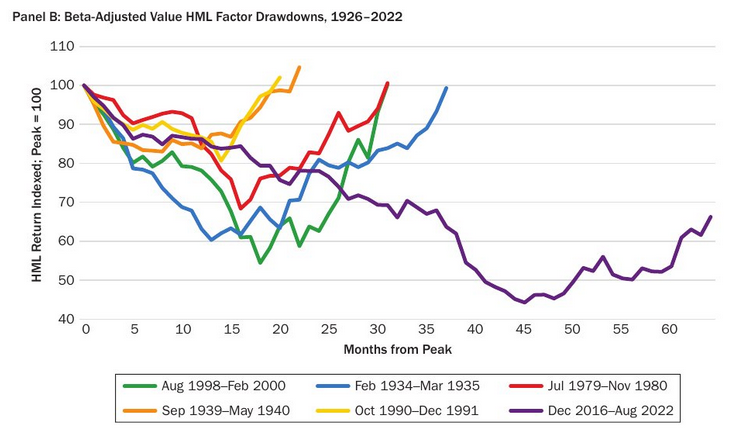

In “Trends and Cycles of Style Factors in the 20th and 21st Centuries,” an article in the Journal of Portfolio Management, Andrew Ang looks at the “time-varying trends” of the most widely-accepted style factors (size, value, quality, momentum and low volatility).

Ang uses the breakpoint of 2001 as the dividing line between the centuries of the title and finds significant differences in the returns, variabilities, and Sharpe ratios of the factors from one time period to another. Potential causes of the changes are mentioned but not explored by the author, including “macro variables,” “constraints that induce investors to act in certain ways,” and “investor behavior biases.” (The effects of popularity would seem to be ripe for analysis too.)

The image above shows the different behavior of late in the value factor on which so many investors have relied — a deeper and longer drawdown than those witnessed in previous history is causing debates about the nature of historical evidence and how to interpret it.

Postings

All of the content published by The Investment Ecosystem is available in the archives.

Thanks for reading. Many happy total returns.

Published: October 16, 2023

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.