It has been a year since the publication of the popular posting “The Active Management Reinvention Project.” What attempts at (real) reinvention have you made or seen made by others? (Time marches on.)

A modern financial tale

In a new article, The Terminalist examines the “LSEG saga,” wherein the London Stock Exchange Group purchased a collection of financial data assets that had been assembled by Thomson Reuters, including Eikon, its terminal offering.

The conglomeration of assets, put together over the last three decades, “carried extensive technical debt from years of underinvestment, representing a rushed merger of two different product roadmaps, operating architectures, and technology stacks.”

Before LSEG became involved, Blackstone carved out those assets from Thomson Reuters (calling them Refinitiv), using a little equity and a whole heap of debt. So, despite the firm having “decaying infrastructure while losing market share to better-capitalised rivals,” the cash flow was needed to pay interest, not to invest in the business.

In short order, before the folly of the endeavor was apparent, Blackstone talked LSEG into buying Refinitiv, “tripling the equity value in less than a year, when the core business was still incinerating capital.” The Terminalist calls it “a staggering wealth transfer from LSEG shareholders” and “a loot like none other.”

There is much more to the story, including LSEG’s liberal use of adjusted measures and EBITDA to make itself look better. For now:

When boards reward executives for performance that excludes the costs of poor judgment, they don’t just enable bad decisions; they guarantee them. When private equity extraction mechanisms go unchallenged, public company balance sheets become extraction targets and shareholders unwitting ATMs. When financial engineering surpasses operational excellence, valuations become inflated by metrics that obscure their true value.

Succession

Permanent Equity rolled out a series of seventeen emails earlier this year, all on the topic of succession, a vast collection of information that is now available in one spot. Included are the core questions that need to be addressed, useful resources from elsewhere, and a cast of characters to illuminate the ideas, from Augustus Caesar to Willy Wonka, Vito Corleone to Steve Jobs, and Spiro Agnew to Logan Roy.

The firm invests in long-horizon private equity, but the content is more broadly applicable. There are succession issues in every organization, including all the ones you invest with and your own.

That time of year

As July turns into August, things get quieter at many firms and the markets slow down. Until something happens.

The August to October period has featured many of the more notable market spasms over the years. Owen Lamont of Acadian provides historical context for the seasonal patterns that existed when the United States was an agrarian nation. Now he chalks it up to summer vacations.

Byrne Hobart agrees: “The mechanism for these summer losses is, at least in part, a matter of tracking down the person who’s in a position to make an authoritative decision.” That contributes to the “slow-then-fast nature of a summer slump.”

Meanwhile, who is minding the shop at the asset managers you use? That’s the question asked by Joseph Eden in a Citywire Selector article, “What really happens when fund managers go on holiday?”

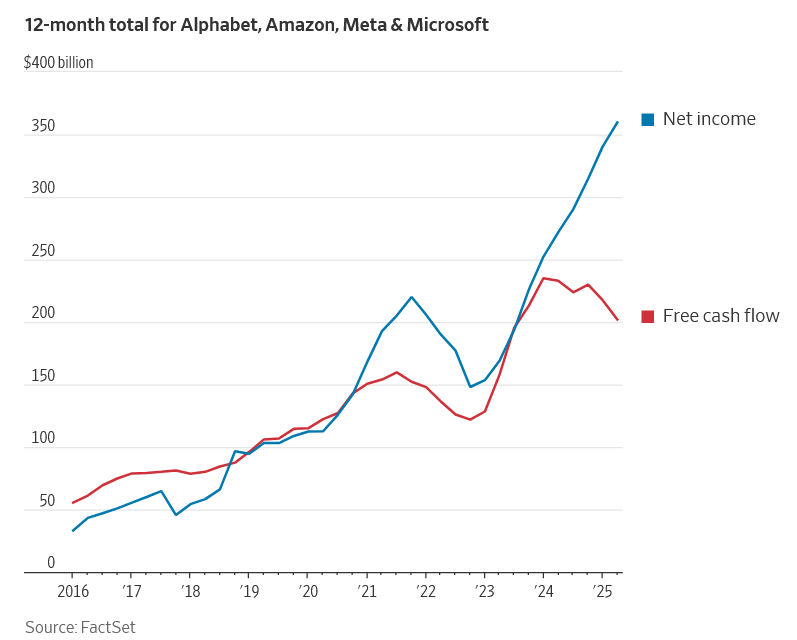

Data centers

The last two editions of the Fortnightly have included pieces on data centers from Paul Kedrosky. His latest, “The Kanye/Data Center Crossover,” deals with the sudden change in interest in the topic. (The title comes from a comparison of search volumes for data centers and for Ye. Unfortunately, the posting is behind a paywall.)

To his point, stories about implications of the massive capital expenditures being funneled into data centers are now proliferating elsewhere. For example, the illustration above comes from a Greg Ip piece in the Wall Street Journal (“The AI Boom’s Hidden Risk to the Economy”). See also “Will data centers crash the economy?” by Noah Smith.

Given the potential economic impact (and portfolio impact, due to the number of investment strategies tied to the trend), it ought to be near the top of the research agenda.

Memorable answers

Anthony Hagan of Freedomization shares interesting perspectives week in and week out regarding the relationships between general partners and limited partners.

One example: “Memorable GP Answers To Common LP Questions.” Note that all of the situations involve general partners being clear about who they are and what they are trying to do, rather than shading their spiels to try to please.

Housing

Matt Zeigler put together “five cool charts” regarding the housing market for Epsilon Theory, identifying narrative shifts regarding that key part of the economy. The charts concern where bargaining power is now (it’s turned into a buyer’s market); the effects of climate, tariff, and zoning changes; and how “housing as an investment” has varied in narrative intensity over time.

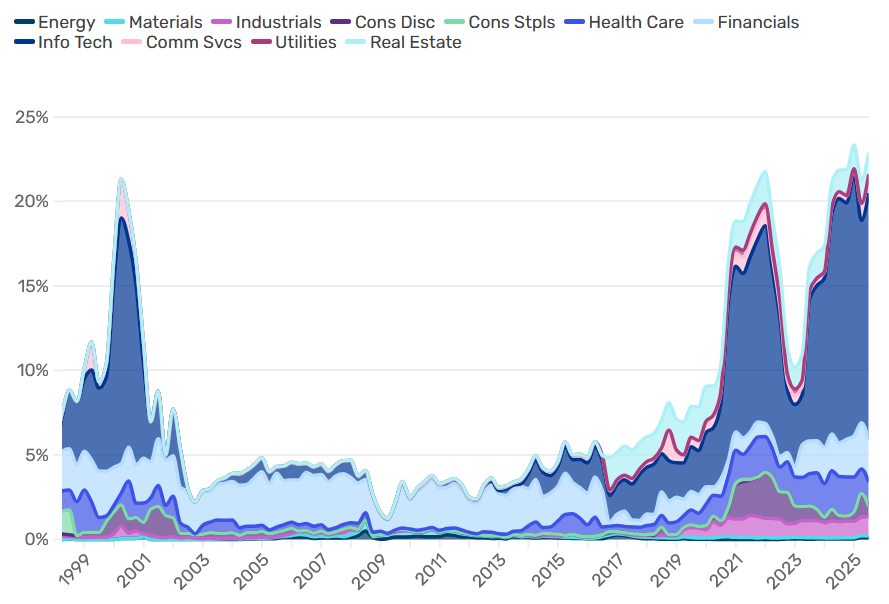

New heights

This image from the Man Group shows the share of MSCI World stocks trading at more than ten times enterprise value to sales. Its conclusion:

While AI-driven enthusiasm has pushed valuations to extremes, history tells us that stocks trading at these multiples rarely deliver the returns needed to justify their price tags. Caution is warranted. Fundamentals still matter.

What’s yours?

Other reads

“Buffett’s Intangible Moats,” Kai Wu, Sparkline.

Buffettʼs long-term success is largely driven by systematic exposure to two key factors: Intangible Value and Quality.

“KKR recut terms with big backers to hand rich investors larger share of deals,” Alexandra Heal, Financial Times. The push to market private assets to individuals — and to put that money to work right away — is leading to changes in terms for institutional asset owners.

“More Meetings Means Less Thinking,” Joe Wiggins, Behavioural Investment.

Even when the process to reach a decision takes time and spans multiple meetings, it doesn’t mean that there has been space for measured thinking. It is more likely just a chain of meetings where instinctive, system one thinking has been the guiding and dominant influence.

“Four Mantras from the Endowment: A Personal Journey,” Ted Karns, LinkedIn. Lessons from “debates, cycles, mistakes, crises, recoveries, and conversations around conference tables” at the Princeton endowment.

“How GenAI-Powered Synthetic Data Is Reshaping Investment Workflows,” James Tait, Enterprising Investor.

Investment professionals routinely face limitations: historical datasets may not capture emerging risks, alternative data is often incomplete or prohibitively expensive, and open-source models and datasets are skewed toward major markets and English-language content.

“Two lesser-known factors behind David Swensen’s success at Yale,” Charley Ellis, Financial Times. Organizational alpha, internally and in dealings with asset managers.

“Nothing Works All the Time,” Ben Carlson, A Wealth of Common Sense.

Just because something worked in the past doesn’t mean it will work in the future.

“The $2 billion (plus or minus) marketing boost that helped mainstream ETFs,” Pat Allen, Finfluential. Why you see all of those advertisements for QQQs.

“What A World (A Few Stories),” Morgan Housel, Collaborative Fund.

BlackRock CEO Larry Fink once told a story about having dinner with the manager of one of the world’s largest sovereign wealth funds.

The fund’s objectives, the manager said, were generational.

“So how do you measure performance?” Fink asked.

“Quarterly,” said the manager.

The gap between ideals and reality.

Asymmetry

“Our knowledge can only be finite, while our ignorance must necessarily be infinite.” — Karl Popper.

Flashback: Entrepreneurs

Saras Sarasvathy’s 2001 paper “What makes entrepreneurs entrepreneurial” became widely known because of a copy that included notes attributed to the venture capitalist Vinod Khosla. Below the title he wrote, “First good paper I’ve seen.”

Sarasvathy contrasted the “effectual reasoning” of entrepreneurs and the “causal rationality” that dominates most business thinking. While causal rationality “tends to focus on the avoidance of surprises as far as possible”:

Great entrepreneurial firms are products of contingencies. Their structure, culture, core competence, and endurance are all residuals of particular human beings striving to forge and fulfil particular aspirations through interactions with the space, time, and technologies they live in.

Causal reasoning: “To the extent that we can predict the future, we can control it.”

Effectual reasoning: “To the extent that we can control the future, we do not need to predict it.”

Much different mindsets. And while it is not the point of the paper, the exposition helps to explain why so many established firms have a hard time innovating.

Capital allocation

Three postings from early 2024 reviewed books that dealt with capital allocation problems: The Climb to Investment Excellence (Ana Marshall), The Rebel Allocator (Jacob Taylor), and The Counting House (Gary Sernovitz). An index of the series provides short descriptions and links to the postings.

Thanks for reading. Many happy total returns.

Published: August 11, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.