The most recent posting on the Investment Ecosystem, “The Active Management Reinvention Project,” addresses the lack of differentiation across much of the active management universe. It’s worth your time and attention. (If you have feedback on the piece, please send it along.)

On to the readings.

AI roundup

It seems as if there are new AI applications coming out every day, and there are a significant number of websites dedicated to keeping track of all of it. For example, the Wolfram LLM Benchmarking Project ranks the performance of more than sixty large language models.

Investment organizations are experimenting with new applications, such as the “research analyst chatbot” at J.P. Morgan. A U.S. Senate report on “AI in the Real World” is based on “information from six hedge funds, each with different structures and who utilize AI in different ways.” It touches on issues of importance to individual organizations, as well as potential systemic risks. Among the concerns:

If an investment advisor utilizes AI to inform or make trading decisions, it could amplify the traditional risk of conflicts of interest. AI systems may make decisions that benefit the advisor but are hidden within the AI systems such that investment advisors are not able to identify and thereby disclose them to clients.

Angelo Calvello provides advice to capital allocators on dealing with “AI washing.” (For one thing, don’t rely on regulators to do your job for you; move up the learning curve and do your own work.) Stepstone Group has issued a report, “Do no harm: how GPs and LPs can use Responsible AI to build trust,” which includes sections on the key risks involved and the global regulatory frameworks that are emerging.

NAV loans

The last Fortnightly featured an image of the various ways that leverage is introduced into a private equity investment program. A new “visual story” from the Financial Times (sorry, a public sharing link is not available) covers much of the same ground in an expanded fashion.

Among those leverage options are NAV loans. The Institutional Limited Partners Association (ILPA) released new guidance for dealing with those loans. It provides an overview of the ways the borrowings can result in “perverse incentives” and a “misalignment of interests” when used by general partners for early distributions or portfolio support. The report includes recommendations for improved transparency and engagement, as well as suggested legal documentation.

Which way from here?

The old saying is that “demography is destiny.” A defining feature of the United States economy has been the movement of people and businesses to the South. In a recent report that looks at the implications for several industries, Lawrence Hamtil and Douglas Ott call that movement “a strong trend that shows no sign of slowing down.” And the title of a Business Insider article claims that “the future of the US economy is in the South.”

In a paper from the Federal Reserve Bank of San Francisco, Sylvain Leduc and Daniel Wilson take the other side of the argument, seeing changing dynamics, probably because of rising temperatures:

The weakening Snow Belt to Sun Belt migration pattern is broad and holds across counties, commuting zones, and states, as well as for both rural and urban areas. In some cases, the direction of migration has even reversed.

Whether this trend continues or turns around will have significant economic repercussions.

Eating the bond market

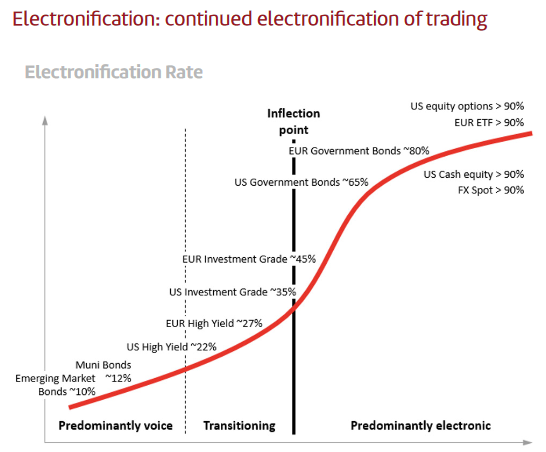

The Financial Times published an article by Robin Wigglesworth and Will Schmitt that declared that “ETFs are eating the bond market.” It quotes a “bond ETF specialist” as saying, “The evolution of fixed income ETFs and electronic trading in bonds are inextricably linked and have been for over a decade.” The article includes the image above, which shows where different markets are in the migration from voice to electronic trading. (It comes from a Flow Traders report that can be found here.)

The theme of the article is that “fixed income ETFs — now a $2tn asset class — are shaking up the old order in a shadowy but important pillar of finance that has long been ruled by big banks and investment groups.”

Equity options strategies

Fidelity published “Liquid alternatives: The power of equity options-based strategies.” It focuses on the “key benefits that equity options may uniquely provide to investors,” arguing for a strategic allocation (while not really addressing the disadvantages or possible risks):

We believe that strategies prioritizing diversification, discipline, and active management, while also ensuring a consistent investor experience, are essential in helping investors achieve their desired investment outcomes.

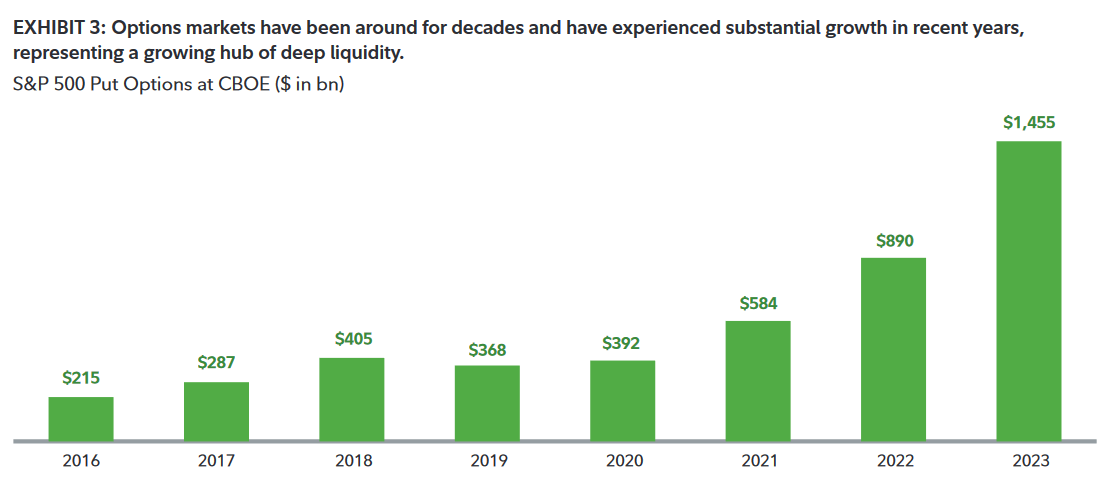

The chart above shows the explosive growth in S&P 500 put options volume over the last few years, which is representative of the escalation seen in other kinds of options strategies over that time. There are signs that market behavior has changed as a result of the increased use of options — will the performance of these strategies do so too?

Responsible investing

A trio of papers on SSRN have the word “responsible” in their titles. “ESG” is referenced in them, but perhaps “responsible” is gaining favor as a headline description as a part of the ESG backlash. Here they are:

“Styles of Responsible Investing” (Stuart Jarvis) examines “the extent to which [the various types of funds] involve differentiated portfolio construction” and whether those distinctions have driven performance.

“Window Dressing Among Responsible Investment Funds” (Huiqiong Tang, et al.) finds that “window dressing” by funds isn’t limited to past winners — in some cases funds shift their investments toward their “ethical index just before reporting their holdings.”

“Responsible Asset Managers” (Ke Shen, et al.) investigates whether the asset management firms that manage ESG portfolios score well on ESG criteria themselves.

Other reads

“A Private Equity Liquidity Squeeze By Any Other Name,” Markov Processes.

How the anemic deal climate, record low distributions and massive unfunded capital commitments are pushing endowments further into illiquid private equity & venture capital, increasing risk & leverage in portfolios (and markets broadly).

“Voting machines vs. weighing machines,” Joachim Klement, Klement on Investng. On the best time horizons for market-based and accounting-based decision making.

“PMs need to be more Bueller, less Rooney,” Simon Evan-Cook, Citywire.

There are two types of competitive people. One type is competitive in a way that enables long-term success; the other type, in contrast, is childish, destructive and usually fails.

“Investment Manager Selection Is Hotting Up. Are You Ready for the Tough Questions?” Clare Flynn Levy, Enterprising Investor. Some questions to ask managers, from Evan Frazier and Joe Wiggins.

“The Multi-Family Office of Tomorrow — Simplifying Complexity for Families of Significant Wealth,” Charles Schwab. The characteristics, services offered, and opportunities for four different types of MFOs.

“The Negative Impact of Crowding on Active Fund Performance,” Larry Swedroe, Alpha Architect.

Relative to traded index funds, funds in the top decile of crowding underperform passive benchmark funds by a statistically significant (t-stat= -4.5) and economically significant 1.4% per annum.

“The Fees on These Funds Will Leave You High and Dry,” Jason Zweig, Wall Street Journal. Some interval funds are “designed to harvest fees that mutual funds and exchange-traded funds don’t have the chutzpah to charge.”

“RADTEC: A Framework for Managing Downside Risk,” Campbell Harvey, et al., Research Affiliates.

The widespread adoption of tracking error as a measure of risk is one of the most significant errors in the practice of finance.

“How to Design a Secondaries Portfolio,” Preqin. This primer covers the basics, including that “transparency is a key challenge” and “LPs have to adjust performance metrics.”

“More on pass the parcel deal making,” Chris Addy, LinkedIn.

There are so many conflicts in intra fund transfers — it seems inevitable that at least some deals across PE/venture land will turn south and end up in regulatory fines, lawsuits and a decade to clean up the mess.

It’s hard to see the big picture

“It is easier for a man to be loyal to his club than to his planet; the bylaws are shorter, and he is personally acquainted with the other members.” — E.B. White.

Flashback: Selling by not selling

In 2009, Brookvine (since acquired by Associate Global Partners) published a piece by Jack Gray, “Selling by not Selling.” It opens:

Successful selling to the institutional investment market requires almost Tao-like contradictory characteristics of patience and impatience, empathy and persistence, integrity and commerciality, discipline and opportunism. Their confluence describes the complex art of selling by not (explicitly) selling.

Among the challenges (especially when dealing with public entities):

Managers are selling an uncertain, intangible service in a compliance-driven, public environment through layers of agents, where each italicised word is a cause of friction and delay. Uncertainty exposes buyers to the risk of underperformance. Intangibility of investment strategies means they can’t be touched or tested unlike concrete products. Layers mean many eyes (CIO and staff, CEO, Board, Investment Committee, Consultants, . . .) must see if not approve transactions. A compliance-driven culture causes delays on non-investment issues. A public environment entails added aversion to headline risk. Agents create misalignments and an emphasis on the shorter-term.

Postings

Explore the archives to find ideas for continuous improvement no matter what kind of organization you inhabit. For instance, see a posting on due diligence, “The Dawning Era of Qualitative Analysis”:

Allocators are sitting on a gold mine of information that can be analyzed. Materials sent by managers across the years can be studied in ways that they couldn’t be before — and the same can be done with investment memos about those managers. What would such an analysis reveal about the process of selection by allocators and the attributes of manager success?

Thanks for reading. Many happy total returns.

Published: August 5, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.