A previous edition mentioned an upcoming posting about “the active management reinvention project.” It’s still coming! (Reinvention takes time.)

Subscribe to get that posting (and others to come) in your inbox.

The energy transition

Larry Siegel wrote a piece, “A Realist Assesses the Energy Transition,” for Advisor Perspectives. In it, he summarizes the work of Mark Mills, “a physicist, venture capitalist, and energy and technology expert,” and concludes:

If Mills is correct, then preparing to adapt to climate change, rather than trying to prevent it, becomes the most important priority.

Siegel argues for a go-slow approach to energy transition, thinking that it is preferable to actions that limit economic growth too much (and he cites a quote attributed to Tyler Cowen: “We’re going to see how hot it gets”).

That sparked a response from Sloane Ortel of Ethical Capital, “A Subtle Rebuttal to an Energy ‘Realist’.” She writes that “the dichotomy between sustainability and prosperity that [Siegel] presents is false. And his logic is not just flawed, but also seductive and therefore dangerous.”

While Siegel had acknowledged that the continued increase in temperatures presents risks, he felt the trade-offs were worth it because greater prosperity would help to lift the poorest around the world out of poverty. But Ortel pushes back on that, in that the effects of climate change on the largest equatorial cities will be profound, and therefore not the net-positive that Siegel thinks it will be for the masses. In any case:

For as long as the world remains imperfect, it’s incumbent upon analysts like me and Larry to embrace the reality that many things can be true at once. There is no “magic bullet” solution waiting in the wings to relieve our planet’s many stresses, nor a simple tradeoff between economic growth and sustainability.

We are, Ortel says, in “the messy gray area where progress actually happens,” but where we are also at risk from “the malignant overconfidence with which us finance types can sometimes trod through thorny ethical terrain.” (Which happens to lead nicely into the next topic.)

A business of uncertainty

In his latest memo, Howard Marks writes:

Investors and others who are subject to the vagaries of the macro-future should avoid using terms such as “will,” “won’t,” “has to,” “can’t,” “always,” and “never.”

Yet the investment business is fueled by confidence and bold predictions rather than intellectual humility and probabilistic thinking. It’s what those who are selling their services do — and what clients have been conditioned to expect.

Marks cites two observations from John Kenneth Galbraith about perennial weaknesses that pervade the investment endeavor — “the extreme brevity of the financial memory” and “the specious association of money and intelligence.” The bottom line for Marks:

Making predictions is largely a loser’s game.

Model validation

CFA Institute Research Foundation released a monograph, Investment Model Validation: A Guide for Practitioners, authored by Joseph Simonian. The need and the problem are summarized early on:

To ensure that asset owners have access to investment products that possess the requisite level of robustness, investment firms must have in place a comprehensive model validation process. However, as critical as model validation is for the reliability and effectiveness of investment strategies, it is remarkable how decidedly unscientific investment strategy development and model validation often are.

The report covers a wide range of issues and practices. It would be even better if it was separated into two sections for the different audiences it tries to address. There is much here for non-professional investors such as asset owner trustees, including important caveats and precautions that ought to accompany presentations of strategies by asset managers. But the text frequently veers into formulae that are only of interest to specialists, so it’s unlikely that trustees (and many investment professionals who aren’t specialists) will wade through it to get to the essential points.

Private equity leverage

Steven Starr of Seward & Kissel posted this chart and comments about it on LinkedIn. Each of the blue boxes represents a lending arrangement that could add leverage to a private equity investment:

In this hypothetical, there is leverage up and down the structure, but no single lender has the full picture of the multiple levels of leverage. And while this may be an extreme example, this is not science fiction.

Starr explains some situations that he has observed, and has good suggestions for lenders and allocators alike.

Two related items from the Financial Times:

~ Blackstone “has become one of the biggest buyers of a type of bank loan that has become a lifeline for the private-equity industry,” including those on its own buyout funds.

~ In a rare instance of investors apparently influencing PE fund behavior, the volume of NAV loans has dropped precipitously after pushback from them.

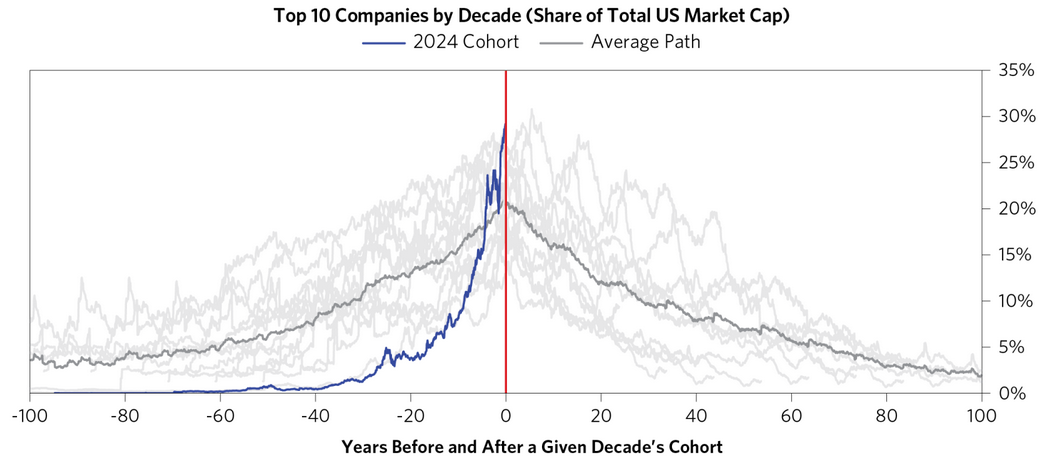

In and out of favor

This comes from Bridgewater’s piece on “The Life Cycle of Market Champions.” It shows how the dominant companies from each of the last twelve decades have fared over time — a good visual of how the market favorites come and go in dramatic fashion. The report also includes charts of individual industries that illustrate some notable cycles.

Other reads

“The Right Kind of Stubborn,” Paul Graham.

The reason the persistent and the obstinate seem similar is that they’re both hard to stop. But they’re hard to stop in different senses. The persistent are like boats whose engines can’t be throttled back. The obstinate are like boats whose rudders can’t be turned.

“How GIC’s Cautious Experimentation Is Paying Off,” Alicia McElhaney, Institutional Investor. The large asset owner tries to take a “rifle-shot, cannonball approach” to new organizational and investing initiatives.

“The Venturification of Research & The Resulting Prisoner’s Dilemma,” Michael Dempsey. Changed dynamics along the spectrum from pure research to startups.

“Can Equal Weight Solve Our Concentration Crisis? Not So Fast…” Ryan Giannotto, Enterprising Investor.

Specifically, equal weight suffers from significant operational costs, underperformance, questionable assumptions, and skewed risk bets.

“Finding Ideas Before Others,” Ian Cassel, MicroCapClub. How you find ideas — and how ideas find you.

“Old School FX Traders Are Being Replaced by Algos With Names Like Viper,” William Shaw and Alice Atkins, Bloomberg.

As they try to keep up, there’s been a sea change in the type of talent that banks rely on to staff their trading desks.

“All or Nothing — The Importance of Data in Secondaries,” Clipway. An analysis “underscores the importance of thoroughly examining an entire portfolio during due diligence, especially in the LP-led secondary market, to understand the risk and return profile of the bottom 30% of NAV.”

“Should Canada Require Its Pension Funds to Invest More Domestically?” Keith Ambachtsheer, et al., SSRN. The Canadian fund business model “has performed remarkably well to date,” but faces outside pressure due to the reduced exposure to Canadian equities over time.

“Have value investors been hindered by this quirk of accounting?” Joseph Taylor, Firstlinks.

Maybe this quirk of accounting goes some way to explaining why systematic low P/E, low price to book strategies haven’t worked as well as they did in the past. A whole swathe of companies may have been excluded for being too expensive when they weren’t. A lot of companies only look cheap in hindsight and never at the time.

“Quantifying Sequence-of-Returns Risk for Institutional Investors,” Kevin Machiz, Callan. Sections include specific looks at the risks for Taft-Hartley plans, public DBs, corporate DBs, nonprofits, and target-date funds.

“Real-Estate Meltdown Strains Even the Safest Office Bonds,” Matt Wirz, Wall Street Journal. CMBS is the acronym that first comes to mind regarding real estate worries. Make room for SASB.

“Does ‘Skin in the Game’ Really Matter?” Joe Wiggins, Behavioural Investment.

Skin in the game is an important idea but also one we can get wrong by misjudging where it exists, what it is telling us and when it might be a problem.

The dilemma

“You have two options. You can stay the same and protect the formula that gave you your initial success. They’re going to crucify you for staying the same. If you change, they’re going to crucify you for changing.” — Joni Mitchell.

Flashback: Copying your neighbor

The abstract from a 2003 paper, “Thy Neighbor’s Portfolio: Word-of-Mouth Effects in the Holdings and Trades of Money Managers,” by Jeffrey Kubik, et al.:

A mutual-fund manager is more likely to hold (or buy, or sell) a particular stock in any quarter if other managers in the same city are holding (or buying, or selling) that same stock. This pattern shows up even when controlling for the distance between the fund manager and the stock in question, so it is distinct from a local-preference effect. It is also robust to a variety of controls for investment styles. These results can be interpreted in terms of an epidemic model in which investors spread information about stocks to one another by word of mouth.

Anecdotal evidence (and common sense) indicate that this effect didn’t disappear upon publication of the study. Decisions by asset managers (and asset owners, advisors, etc.) are influenced by those in their network, especially those with whom they have in-person contact.

Postings

Explore the archives to see the back catalog of evergreen essays, including “When Analysts Throw in the Towel”:

Analysts are expected to be industry experts, but some aspects of the job are performative in nature: hold recommendations that are implicitly something else; reiterations done for promotional purposes only; earnings estimates that have over time become more and more “adjusted” in order to support a position; and target prices with varying time horizons and no clear delineation of embedded market expectations or stock-specific risk adjustments.

Thanks for reading. Many happy total returns.

Published: July 22, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.