In upcoming months, paid subscribers will receive postings that focus on the future of work in the investment world. Changes in technology, demographics, and employee preferences will transform every organization. New practices will be needed to compete effectively.

The postings will examine the implications of those changes and provide ideas that will help you to navigate them. The content on the site won’t be exclusively devoted to related topics; it will be interspersed with the broad range of material that readers have come to expect.

(If you’re not a paid subscriber already, please consider a monthly and yearly plan. It’s a small price to pay given the importance of your mission.)

Meanwhile, our “interesting times” continue in the markets, as reflected in this edition’s readings.

Crypto questions

Campbell Harvey is the lead author (with six others) of “An Investor’s Guide to Crypto,” a report which provides a tidy overview of the major investment considerations regarding cryptocurrencies.

They divide the “investible universe” into six categories. (So-called stablecoins were left out, for reasons explained; the paper appears to have been completed prior to the Terra/Luna lunacy during May.)

A section titled “The Challenges of Valuing Crypotocurrencies” examines “some popular approaches to valuing cryptocurrencies such as bitcoin. None of these approaches are satisfactory.” They include Metcalfe’s Law, Bitcoin as “digital gold,” value in relationship to mining cost, a flow-versus-stock analysis, and relative value approaches.

The next part looks at performance and risk characteristics — and how crypto might be used in a portfolio. The lack of historical data is a problem, but some conclusions can be drawn, including that

in normal times bitcoin has limited correlation to other assets often used as multi-asset portfolio building blocks. However, as we move further into the left tail of the return distribution, the correlation with some of the naturally riskier assets rises dramatically.

One odd aspect of it all is that custodial and regulatory issues are backwards from those for most alternative investments: “For cryptocurrencies . . . retail investors have easy access, and it is professional asset managers that face substantial hurdles.”

Elsewhere:

PGIM has released a white paper, “Cryptocurrency Investing: Powerful Diversifier or Portfolio Kryptonite?” It sees “no compelling case for direct ownership of cryptocurrencies as a meaningful share of an institutional portfolio,” but argues that “there are attractive institutional investment opportunities in the broader crypto ecosystem.”

A paper on “How the Cryptocurrency Market is Connected to the Financial Market.”

In a New Yorker column, John Cassidy wrote that “ever since big money got in on the crypto game — venture-capital firms, hedge funds, and, lately, some of the big Wall Street banks themselves — there has been a great deal of expensively produced puffery and flimflam surrounding the entire industry.”

Valuation uncertainty

Everyone’s trying to figure out valuation and how much overshoot might have occurred during the last few years.

“Are Stocks Undervalued Yet?” asks the Wall Street Journal. The article by Mark Hulbert has this conclusion for a subhead: “Eight valuation models suggest that even after recent declines, the stock market isn’t a good value.” Seven of them are just 2-16% off of their historic highs; the lone exception, P/E ratio, is around 60%, but that benefits from margins that are, yes, historically high themselves.

(One of the models is the “Buffett indicator.” A recent study corroborates that it “explains a large fraction of ten-year return variation for the majority of countries outside the United States.”)

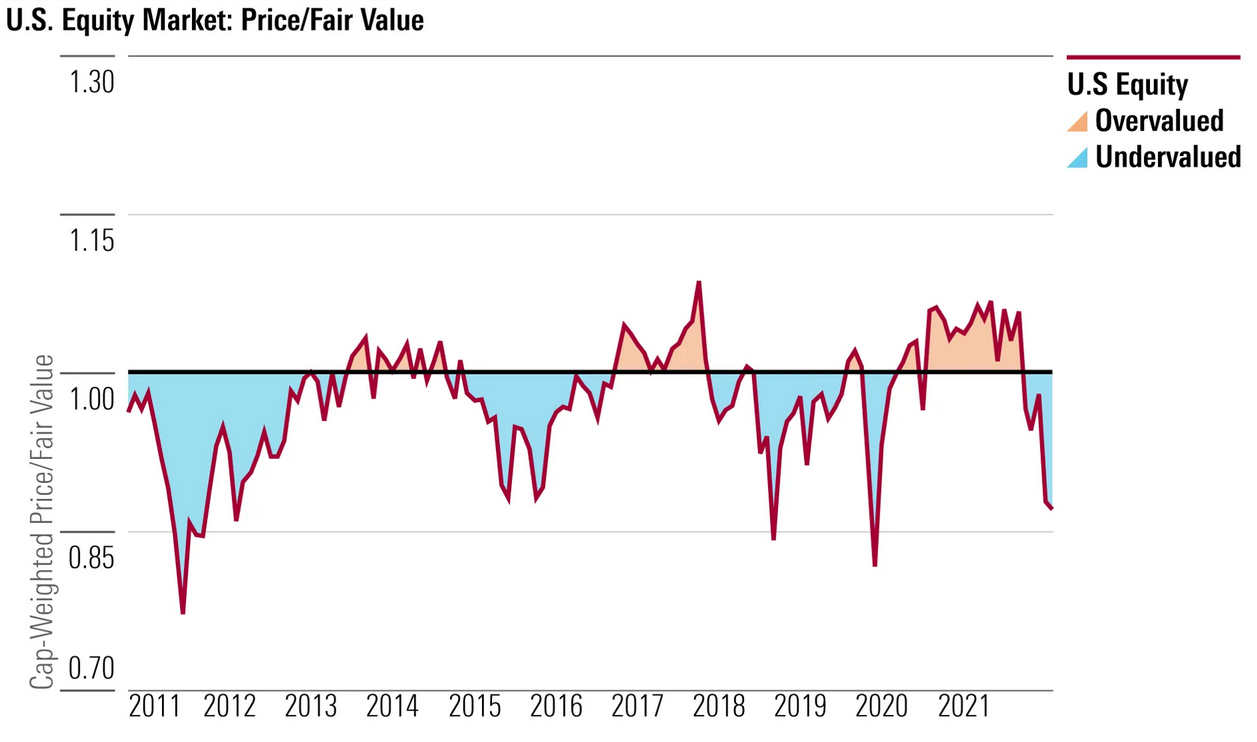

A different view is put forth by Dave Sekera of Morningstar, who thinks that stocks “are trading at a rarely seen discount.” The firm has a disciplined process that focuses on price-to-fair-value, a much better approach than using target prices. Here’s some history of that measure:

The big question is whether the Morningstar analysts’ fair-value models have unrealistic expectations about margins, growth rates, and discount rates given a much different macro landscape now than has been seen in a very long time.

In the realm of private assets, where valuation marks are a quarterly affair, it’s not so much a question of whether today’s price is a good one but what today’s price should be.

Jeffrey Diehl of Adams Street published a posting on “The Impact of Public Market Dislocations on Private Markets.” He put a stake in the ground regarding valuation: “Based on what we have seen in past market cycles, we estimate our private holdings will likely decline by about 60% of the fall in public markets.” (Since most down moves have been short, the quarterly marks never quite catch up. A lengthier retrenchment might show a different pattern.)

Compare that to a Bloomberg article about D1 Capital Partners, which said that its public securities holdings were down 44% so far this year, while its private ones were only off 8%. It feels like there are a lot of shoes yet to drop.

Free money

The legendary venture capital firm Sequoia put together a presentation for the founders of its portfolio companies titled “Adapting to Endure.” It captures the abrupt change in attitude that is reflected in valuation uncertainty in VC land and real cutbacks among the unicorn crowd and those that thought they were on track for that status.

The message is clear; “the removal of free money” changes the calculus. (Cue a song from a stagflationary era long ago.)

Other reads

“Diversity Matters: The Role of Gender Diversity on US Active Equity Fund Performance,” Stephen Lawrence, SSRN.

Maximizing gender diversity in active equity investment teams correlates with as much as a 38.9 basis point improvement in fund performance after controlling for characteristics of the fund and its investments as well as other dimensions of diversity.

Quality and diversity of education are strong indicators of fund outperformance but cannot explain the unique benefit that gender diversity brings to a team.

“Everything old is new again: The FT reports EY may spin off its audit arm,” Francine McKenna, The Dig. “We’ve seen this song and dance before,” says the subtitle. “Wanna bet which entity gets out from under all the bad vibes of Wirecard, Luckin, NMC, and all the independence issues pending at EY US?”

“Bull Market Rhymes,” Howard Marks, Oaktree.

Does it really matter whether the S&P 500 is down 19.9% or 20.1%? I prefer the old-school definition of a bear market: nerve-racking.

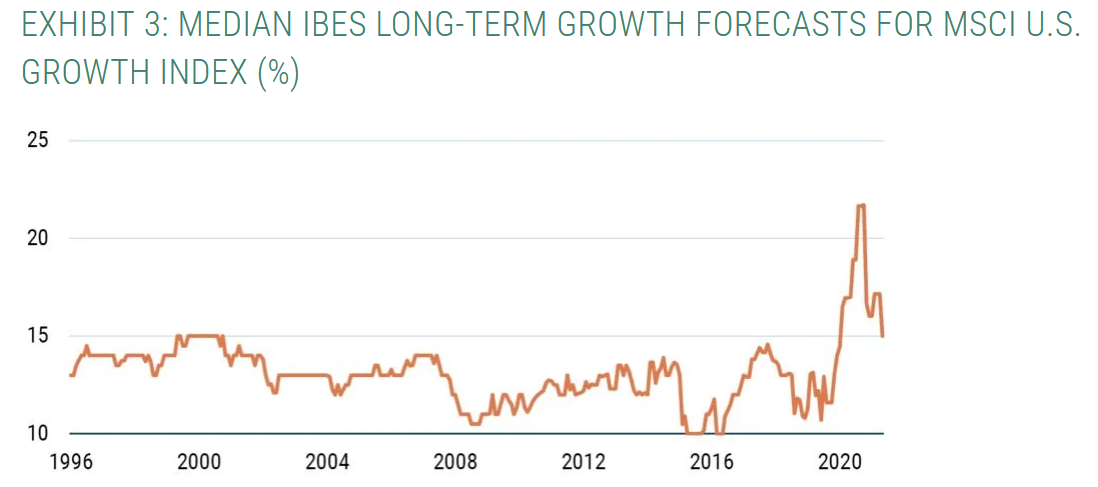

“Growth Traps Snap Shut,” Ben Inker, GMO. A “quick refresher” on the less-talked-about cousins of value traps, which includes this chart of how far expectations got out of whack this cycle:

“A Pension Fund That Lost Billions in Allianz Funds’ Collapse Is Now Pointing Fingers,” David Voreacos and Neil Weinberg, Bloomberg. An asset owner and a consulting firm argue about who didn’t fulfill their duties regarding a very large, disastrous bet.

“Understanding,” Tim Quast, Modern IR. “The sellside is so yesterday.” Today, investor relations professionals need to “go where the money is, by becoming what it wants.”

“Bond trading 3.0,” Robin Wigglesworth, Financial Times.

Fixed income is now in one of those classic flywheels beloved by consultancies, where more electronic trading begets more adoption, liquidity and innovation, and in turn even more electronic trading.

“Value Investing Is Not All About Tech,” Cliff Asness, AQR. “Perhaps not surprising, when investors are willing to pay a relative ton for the ‘hot’ industries, they are also in the mood to pay a relative ton for the ‘hot’ companies within each industry.”

“Asset Managers Say Your DDQ is 50%+ Duplicative,” Castle Hall.

At present, we have a smorgasbord of different questionnaires and templates by asset class which materially hinders efforts to create a consistent diligence process for all plan assets.

“Private Equity Headhunters: Pathway Providers or Unethical Gatekeepers?”

Powers of selection

“In a world that changes more swiftly than we can perceive there is always the danger that our powers of selection will be mistaken and that the vision we serve will come to nothing.” — John Cheever. (He was referring to fiction, but it applies to our business of uncertainty as well.)

Slashed expectations

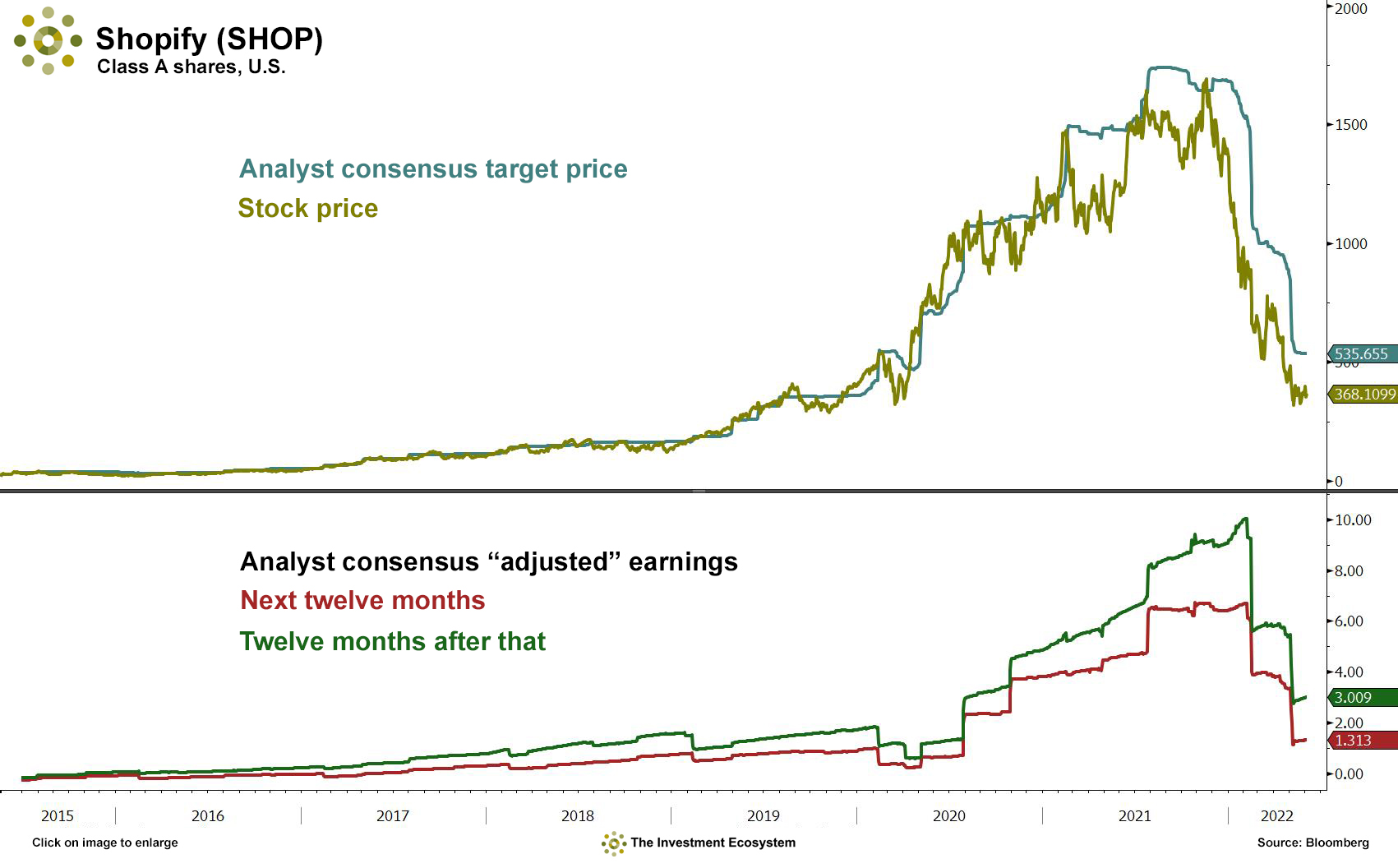

Shopify is one of those stocks that had extraordinary gains which is now deep down the back side of the mountain. The top panel shows the stock price, as well as the consensus target price. From the peak, the stock is down 78%. The bottom panel shows the sharp rise and fall of earnings expectations.

All of that makes for interesting timing for a shareholder vote on whether to preserve Shopify founder Tobi Lutke’s voting power. Advisory firms ISS and Glass Lewis are opposed, and CalPERS is voting against the proposal; Bloomberg has the story.

Postings

Here are links to three postings of late. The first is a long-form look at one of the most important topics there is:

“Revisiting Beliefs about Private Equity.” Despite the popularity of private equity, beliefs about its performance attributes vary dramatically, while the investment characteristics of the holdings are much different than in the past. That calls for a reassessment.

The other two are the first of a new format called “Four for Friday,” which feature several angles on a theme.

“More on Private Equity” was a natural follow-on to the piece above, including items on certainty versus uncertainty, access and analysis, the impact of a large class of investors, and PE investments in RIAs.

“The Role of Sell-Side Analysts” covered a famous phrase — “Great quarter, guys” — plus robot analysts, non-deal roadshows, and the mix of “investing” and “the game” in sell-side roles.

Follow us on Twitter to see the Charts of the Day, which range from investment strategies (like the Freedom 100 Emerging Markets) to individual securities (what a move in this energy bond) to asset classes (how long did it take for stocks to out-return corporate bonds?).

All of the content published by The Investment Ecosystem is available in the archives.

{kind=link}

{kind=link}

Published: June 6, 2022

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.