A series of short postings about core concepts for evaluating investment organizations continues on LinkedIn. The topics covered during the last two weeks: change, compression, maps, and mess. (The concepts are used extensively in the Investment Ecosystem Academy’s course, “Advanced Due Diligence and Manager Selection.”)

If you’d like to get postings like this Fortnightly and original pieces on interesting ideas in the investment world, you may subscribe here.

On to the readings.

The conviction mirage

In the wake of the DeepSeek hit to Nvidia and other AI stocks, Kris Tuttle wrote a posting on Random Candy that recounted a situation when he was a sell-side analyst in the 1990s and one of his favorite stocks came under a lot of pressure.

As the drop escalated, so did the interaction with a key client (at one point during which it occurred to him “that the largest institutional shareholder doesn’t know what the company does”). The lesson:

When stocks go up, everyone feels firm in their convictions. But when something happens, and stocks fall sharply, their ability to articulate and believe in their own convictions often goes out the window.

(For his part, Tuttle thinks the DeepSeek developments are “a big deal.”)

Ted Merz focused on how the story “flew under the radar” for seven days before having an outsized impact:

It’s arguably the biggest dropped ball in memory on the part of financial journalists, traders and money managers.

A number of people have pointed to “The Short Case for Nvidia Stock,” published by Jeffrey Emanuel on January 25, as precipitating the big drop when stocks reopened two days later. Why did it take so long?

As Aswath Damodaran has explained in his book Narrative and Numbers (reviewed here) and in his other writings, he links the components in his valuation of a company to its story (as he sees it) at any point in time. He is very willing to reexamine that story and therefore the valuation (often in significant ways) as circumstances change. In practice, his approach is quite different from the journey of faith that ensnares many professional investors.

In a recent posting, Damodaran differentiates between story breaks, story changes, and story shifts — and places the effects of DeepSeek on leading AI companies as being in the story-change category, denting the existing “happy talk” narrative. (Although he has been an owner of Nvidia, his valuation of it is now substantially below the current stock price.)

The larger question here is how and when investors change their minds about something. It can take a very long time for reactions to occur in real time that seem obvious in hindsight. For example, think of the snail-paced recognition of risk as the coronavirus spread. Even as the news grew worse and worse, there wasn’t much change in the market. Until there really was.

For much of the investment ecosystem, risk management is statistical rather than qualitative and anticipatory. With that approach, until the market tells you it’s problem it’s not a problem.

Pretzel logic

In a column, “Maybe ESG Is Illegal Now,” Matt Levine wrote at length about the puzzling court decision involving a defined contribution pension plan of American Airlines. This paragraph points out the inanity of the ruling:

The result is apparently that investors are not allowed to consider risks if those risks are politically disfavored. If you base your investment decisions on reading financial statements or drawing lines on stock charts or tracking sunspots, a judge will not demand that you prove that those techniques lead to higher returns. But if you base your investment decisions on a theory like “climate change will lead to more forest fires that will be bad for insurance companies,” a judge will suspect that you are lying and demand that you prove it. Some kinds of risk analysis are left to the business judgment of professional investment managers. But some, now, are not.

Primitive portfolios

In an opinion piece in Institutional Investor, Richard Ennis bemoaned the state of institutional investment management. As private investments soared in popularity, “the nature of investment supervision changed.” Most “alternatives” are not really alternatives now, but the foundation on which portfolios (and behavioral norms) are built.

The result is what Ennis calls “scattershot diversification”:

There is nothing elegant about portfolio construction today. In fact, it seems almost primitive. Institutions own a jumble of equity things — nearly countless, largely illiquid, and beyond their control.

That stage of the market

Owen Lamont of Acadian capitalized on a David Einhorn phrase to write a piece about “the Fartcoin stage of the market.” He sees “market nihilism;” virus-spreading memes (which he cops to contributing to himself: “As you read these words, the idea of Fartcoin is burrowing deeper into your mind.”); stupidity; and “smart money selling to dumb money at the peak”:

I can’t believe I’m saying this, but the current meme coin mania makes the bubble of 2021 seem like a relatively sober exercise in rational valuation.

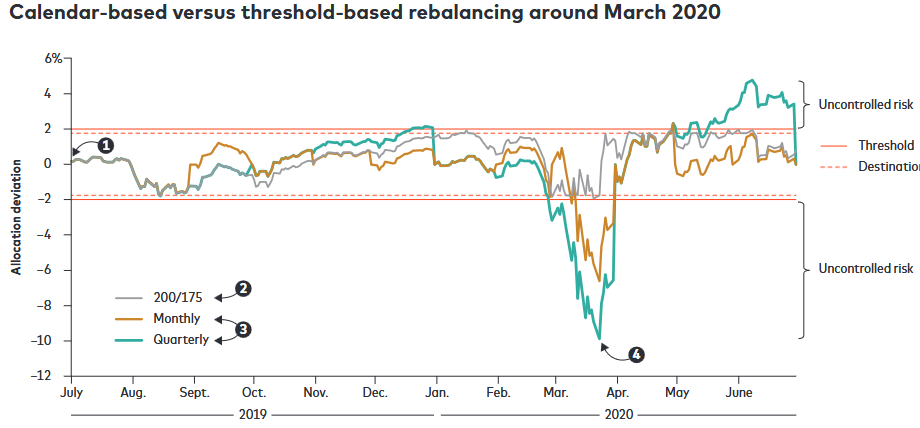

Rebalancing

This image comes from Vanguard’s report, “The rebalancing edge: Optimizing target-date fund rebalancing through threshold-based strategies.” It illustrates what it calls a “200/175 strategy,” whereby there is a threshold of 200 basis points away from a target allocation, from which the rebalancing dials the exposure back modestly to 175 basis points from target.

The analysis is accompanied by various warnings about the shortcomings of simulations, but the firm concludes that compared with calendar-based approaches, threshold-based rebalancing results in smaller deviations from target allocations, higher annual returns, and lower costs.

While the piece directly referenced target-date funds, similar rebalancing issues are also faced by advisory firms and institutional asset owners.

Active management

Clare Flynn Levy of Essentia Analytics writes that “the investment management industry is, at its essence, selling decision-making as a service.”

Passive investing has been a juggernaut, but Levy warns that “market cap-weighted indices are becoming dangerously concentrated and no longer fit for purpose — whether that purpose is to serve as a benchmark or to provide diversified returns.” And the historical information upon which investors base their assumptions has become “significantly less reliable” given the change in market structure. She thinks there is hope for the beleaguered advocates of traditional active investing:

For active managers, the path ahead is narrower and more demanding, but those who can align with evolving investor needs and deliver tangible value will find that their relevance, though tested, is not obsolete. The industry’s challenge is not survival — it’s transformation.

(See also “The Active Management Reinvention Project.”)

OCIO performance

CFA Institute released its “Guidance Statement for OCIO Portfolios,” part of the Global Investment Performance Standards (GIPS), which dictates how asset managers report their results. An Institutional Investor article by James Comtois reported that the statement has received “mixed reviews.”

There was nothing mixed about the reaction of Brian Schroeder of OCIO Monitor. He sees a number of problems with it, including the degree of latitude in selecting a composite range within which to compete and the ability to classify assets in a variety of ways — the end result being the ability of providers to game the system. The statement “will muddy the waters and create false trust in OCIOs that wear the halo of being GIPS compliant.”

Other reads

“Artificial Intelligence and the Risks of Harking (Hypothesizing After-the-Fact),” Larry Swedroe, Alpha Architect.

The takeaway then is that because AI systems can produce hundreds of seemingly coherent theoretical explanations for mined empirical results, investors need to establish high hurdles before allocating to anomaly-based strategies.

“Rise in Creditor on Creditor Violence,” Ironshield Capital Management. Subtitled, “A European perspective,” this includes explanations for the different strategies in the escalating creditor wars around the world.

“What’s Predicted Funds’ Performance? The Thing That Wasn’t Supposed to Work,” Jeffrey Ptak, Basis Pointing.

Pre-fee past performance did a very good job of predicting funds’ subsequent performance, on average, over the past few decades, almost no matter which way you looked at it.

“The Future of Venture,” Seth Levine, VCAdventure. More and more, “fund size is fund strategy.”

“How the role of the gatekeeper is evolving,” Tania Mitra, Citywire Pro Buyer.

Part of the reason why the gatekeeper job has changed is due to the evolution of the investment industry itself. The mutual fund is no longer the only vehicle to consider. Product innovation has ballooned, ETFs have risen in prominence and popularity, and alternative investments are becoming more mainstream.

“Fund finance: NAV financing unlocked, Christopher Bone, et al., Partners Group. Three perspectives on NAV financing: LP, GP, and NAV lender.

“A decade in need of a course correction,” Roger Urwin, Top1000Funds.

Can we expect the asset owners and corporations to do the right things in the coming years? The increasing pressure from civil society on these organisations raises my expectations that they will follow the purposeful road.

“Human traders are valuable, actually!” Robin Wigglesworth, FT Alphaville. Is the NYSE floor “a very elaborate TV set for CNBC” or is there still something special about it?

“I am leaving my buy-side job and am fed-up with the nepotism,” Anonymous, eFinancialCareers.

It’s not just relatives of senior employees. We’d also employ the sons and daughters of key clients. Another graduate I worked with was the son of the CEO at a client firm. His dad knew our senior management team.

So much for best practices

“Recognize that many of your best practices were designed for a world that no longer exists. In the face of rapid change, past patterns don’t predict the future.” — Adam Grant.

Flashback: Trilogy Systems

Ever since semiconductors became a thing, investors have thirsted after the companies that make the latest and greatest kinds of chips. And after entrepreneurs who have been proven money-makers.

Those two strands came together when Gene Amdahl — a leading computer designer for IBM and the founder of Amdahl Corporation — started Trilogy Systems in 1980. Its IBM-compatible machine was to be more affordable and more powerful. The secret? Wafer-scale integration (WSI).

Investors ate it up, with substantial venture funding followed by a splashy IPO in 1983 that drew the biggest road show crowds during a time of hot new issues. Unfortunately, the stock fell more than 95% in the next year, as it became clear that WSI wasn’t going to work.

More than forty years later, Cerebras has filed for an IPO. The prospectus leads with pictures of its “wafer scale engine” and the very-large-font promise: “Bigger chips are faster and more efficient for AI.”

(For much more on Trilogy, see part one and part two of a piece by The Chip Letter.)

Postings

All of the postings may be found in the archives. Each posting is put into a category, but they tend to be universal and evergreen. That way you can see possibilities across the ecosystem.

For example, “Essential Elements in External Networks,” from 2022, addresses issues regarding those networks:

In our investment-related duties, we have external networks as well as internal ones. While a few organizations could be considered isolationist in their approach, in general the range and quality of those external networks are critical factors in determining what ideas are considered. They also are a main driver of the social pressure that motivates many decisions.

Thank you for reading. Many happy total returns.

Published: February 3, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.