AI this, AI that. You can’t get away from it.

And it is featured in the most recent essay on the site (“Humans, AI, and Organizational Upheaval”), which deals with a critical topic that is conspicuously absent from almost all discussions about the investment applications of AI:

While the natural (and necessary) inclination will be to build AI expertise in your organization, laying the groundwork for a new cultural and collaborative framework will be just as important.

More broadly, machines are affecting the nature of organizational learning; insights from a recent book about those dynamics are included in the posting. Needles to say, important stuff.

IRRational comparisons

A recent paper by Simon Hayley and Onur Sefiloglu, “Bias in IRRs,” examines problems with the internal rate of return measure:

We identify two separate biases, resulting from variation in the periods over which assets are held, and their covariance with the returns achieved. These biases raise IRRs compared to the returns on other asset classes.

The use of IRRs makes a “Quit-Whilst-Ahead” option available to private equity managers, since exiting strong early investments can lock in high IRRs. That further obscures the already difficult evaluation of whether a manager is lucky or skillful — and it allows the manager to more easily market its next fund. A robust IRR is marketing gold.

The biases lead to attractive comparisons for PE returns versus the annualized rates of return on other kinds of funds:

The notably higher average IRRs generated by PE funds (13.2% per annum compared to a total return on the S&P500 of around 10%) can largely be accounted for by bias, and hence would be entirely consistent with there being no outperformance by the PE sector.

But rather than recognizing the biases and being skeptical of advertised numbers, professional investors overwhelmingly take IRRs at face value. “Surveys clearly show that investors continue to rely on IRRs,” something which is evident to anyone who has been in investment committee meetings. Such reliance “is likely to lead to misinformed asset allocation decisions,” although that never seems to be discussed by those involved.

Early in the paper, the authors write, “The IRR is known to be a problematic measure.” Perhaps that ought to be stamped in a large, bold, red font on investment memos, although dependence on IRRs is so embedded in practice that such warnings might be ignored.

An Enterprising Investor posting by Ludovic Phalippou, “The Tyranny of IRR: A Reality Check on Private Market Returns,” takes up a similar theme. The first of three promised articles, it focuses on “the source of the belief,” using news items and practitioner publications to show why “most investors believe that private capital funds are such clear outperformers.”

The use of since-inception internal rate of return (IRR) as the industry’s preferred performance metric and the media’s coverage of the sector’s performance are to blame.

The myth of the Yale model — a belief of superior returns stemming from a heavy allocation to private equity funds — is based solely on a since-inception IRR.

Whether these ideas ring true to you or not, they are of utmost importance to institutional asset owners, who have established ways of analyzing private asset returns, and for advisory firms that expect to ramp up the exposure to such funds for their clients. The topic ought to be at the top of investment committee agendas.

Impact venture capital (and the big picture)

An article by Alan Gutterman, “Impact Investment Funds,” offers a good framework for investments “made with the intention to generate positive, measurable social and environmental impact alongside a financial return.”

But the piece comes across differently today than it did just a week ago. The political winds have changed (at least in the United States), prompting a “Now what?” question.

Prohibitions against non-financial considerations by governmental pension plans (even when those “non-financial” considerations are directly related to long-term risks and returns) seem sure to spread. And litigation will likely be more prevalent against asset managers, owners, and intermediaries that use ESG/sustainability/impact criteria in their selection processes. Debates within organizations will intensify.

It was easier to hold beliefs about impact investments with the wind at your back; with a fresh wind in your face, it is a whole different story.

A Bloomberg piece by Frances Schwartzkopff covers a recommendation that “all ESG fund managers . . . have a lawyer on the team, or on speed-dial.” Over the last two decades, ESG has become integrated into the investment system, and now there is likely to be a backlash quite beyond the one seen in the years leading up to the election.

Consider a couple of publications from CFA Institute released in the last two months: How to Build a Better ESG Fund Classification System and Net Zero in the Balance. Again, “Now what?” How will the political environment change the path of investment practice?

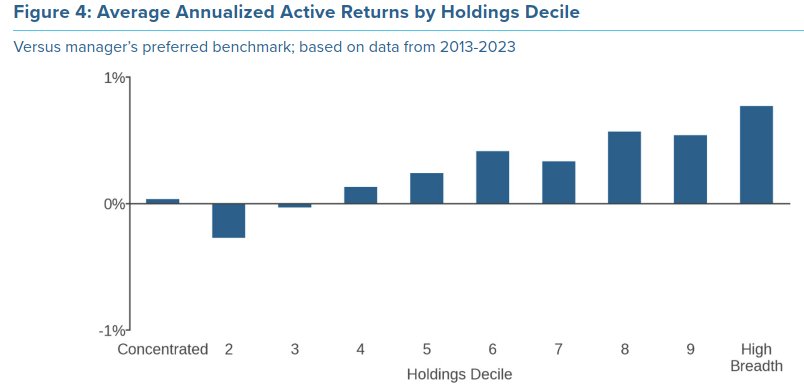

Practice versus premise Acadian Asset Management is a systematic manager which invests in very diversified portfolios. Therefore, the conclusions of its report “Concentrated Equity: Practice Versus Premise” might be expected. As for the premise referenced in the title:

Acadian Asset Management is a systematic manager which invests in very diversified portfolios. Therefore, the conclusions of its report “Concentrated Equity: Practice Versus Premise” might be expected. As for the premise referenced in the title:

For asset owners under pressure to meet high absolute returns targets and frustrated with active fees charged for closet indexing, the premise of investing with stock pickers who focus on a limited set of “high conviction” holdings has intuitive appeal as well as support from academic literature on the performance of mutual fund managers’ largest active positions. But does the approach work in practice?

The chart above shows the results of the Acadian study. The first decile (encompassing the most concentrated funds) shows a slight outperformance, although that was driven by good results “only in the late teens and through mid-2021.”

And, while “investors scanning track records for exceptional performance are inordinately likely to find it produced by concentrated managers,” the same can be said for those trying to identify laggards. Higher active risk means a higher dispersion of returns — and “the noisiness of concentrated strategies’ returns raises the stakes in distinguishing skill from luck, since it increases the likelihood of exceptional performance that results from chance.”

Thematic funds

Morningstar has issued its “Navigating the Global Thematic Fund Landscape.” The survey includes an informative look back at the history of thematic funds (starting in 1948!), an in-depth classification system, and analyses of asset levels and results for the funds in major markets around the world. The charts tell the story: Most thematic funds don’t survive for fifteen years and only a sliver of the original cohort actually outperform.

A crack in the model?

The widely-admired “Canadian model” includes both investment and organizational attributes. Regarding the latter category, one of the tenets is the lack of political interference. That makes a recent action by the province of Alberta a surprise: It removed the board, the CEO, and three other executives of the Alberta Investment Management Corporation (AIMCo). Details in a CBC story.

Other reads

“Misaligned Incentives, Jamin Ball, Clouded Judgement.

I’m not meaning to imply big funds = bad. But there is a culture and mindset that starts to creep in the larger and larger funds get, and it’s up to founders to determine which investor falls into which bucket.

“Forget Hedge Fund Strategy Labels – Here Are Three Groups that Matter,” Toby Goodworth, bfinance. Grouping the many hedge fund types into convex/divergent, market independent, and directional strategy buckets.

“Past, Present, and Future of Modern Finance,” Rob Arnott, Research Affiliates.

[Historically] Innovative concepts are challenged, then accepted as fact, eventually becoming received wisdom, even dogma.

[Now] Both the academic and practitioner communities in our industry are perhaps too complacent, and too invested in maintaining the current equilibrium or paradigm.

“AI: Your New Investment Guru or Overzealous Intern?” Ken Akoundi and Kartik Uchil, Institutional Investor. On the possibilities for an investment office when artificial general intelligence is available — including the importance of “a ‘human-in-the-loop’ system.”

“Debunking a View on Performance of Long-Short Equity Managers,” Brendan James, et al., Evanston Capital.

Active managers on average tend to de-risk during a drawdown which can lead to names with heavier active manager ownership falling more than the market and names with heavier-than-average short interest rising more than the market.

“The Case for the Seventh P: Progression in Nonprofit Investment Stewardship,” Allison Kaspriske, Commonfund. Given that the Investment Ecosystem is itself an advocate for continuous improvement strategies, we are in favor of getting organizations “to look beyond the present moment and ensure they are prepared to meet future challenges head-on.”

“Wall Street frenzy creates $11bn debt market for AI groups buying Nvidia chips,” Tabby Kinder, Financial Times.

Its rapid growth has raised concerns about the potential for more risky lending, circular financing and Nvidia’s chokehold on the AI market.

“Meeting the challenge of the new regime in endowment portfolios,” Edward Ng, et al., BlackRock. A new interest rate environment, growth uncertainty, and increased volatility mean that asset owners should adjust their previous approach.

“The #1 Use Case for AI,” Tim Hanson, Permanent Equity. Using a machine to do what people should be doing in the first place.

Past and future

“No amount of sophistication is going to allay the fact that all your knowledge is about the past and all your decisions are about the future.” — Ian Wilson.

Flashback: Go figure

In the October 8, 2007 issue of Barron’s, Alan Abelson’s column carried the title “Go Figure.” It referenced the “explosive stock market rally” the previous week, which was prompted by announcements from Citi and UBS that they would take multibillion write-downs related to subprime mortgages, leading investors to believe that such admissions meant that the banks “were confident that the worst of the subprime fiasco and the credit crunch were over, the formidable pile of leveraged-buyout loans gone sour was no big deal, and, from here on, it was all blue skies.”

Regarding such a belief as “essentially bonkers,” Abelson wrote:

The worst isn’t over; on the contrary we haven’t truly begun to feel the full effects of the demise of subprime mortgages, the damage visited on the global credit markets and the unchecked disaster that is housing.

The market peaked the next day before heading into the depths of what has come to be called the Global Financial Crisis. Without government intervention, the list of casualties among leading financial institutions would have been very long indeed.

Postings

All of the postings (close to two hundred now) are available in the archives. As one example, check out “Challenges and Quandaries in Manager Research,” part of a series of postings about The Bond King by Mary Childs, concerning Bill Gross and Pimco. It is anchored by a number of questions for those doing manager research, and also includes this reminder:

Many doing due diligence are too cautious with managers, and not just the famous ones. They are concerned about future access, so they don’t want to ruffle feathers. It’s not that you want to go in with both guns blazing, but you need to go where others haven’t gone.

Thank you for reading. Many happy total returns.

Published: November 11, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.