It is a bit surprising that a book titled Private Equity is not much about private equity. The memoir by Carrie Sun is centered on her time as an assistant for “Boone,” the leader of the investment firm “Carbon.”

Published reports indicate that her boss was actually Chase Coleman of Tiger Global; knowledgeable observers might have guessed that from the descriptions of the firm that Sun provides. In turn, that makes “Martin” of “Argon” — Boone’s mentor — Julian Robertson, the legendary founder of Tiger Management. (Despite those revelations, the pseudonyms used in the book are employed in this posting as well.)

Background

In contrast to what you might imagine as the background of an assistant, Sun had worked in investment roles at Fidelity for over four years before she left with conflicted feelings about the investment industry, “hoping to do a pivot.”

It seemed as if there was no real path of advancement for female analysts at Fidelity “except to marry a male PM.” But the money! Sun’s compensation rocketed with “very little effort on my part — and this felt cosmically wrong,” Not everyone was bothered by that; a coworker told her, “I basically sit on my ass and do nothing and make millions. What could be better than that?”

People said she had missed “the good old days,” which included activities such as “a $160,000 bachelor party, thrown by a few brokers for a star Fidelity trader, aboard a yacht with female escorts, ecstasy pills, and a dwarf-tossing competition.” (A settlement with the SEC followed.)

When she was interviewing at Carbon, Boone asked her what she did at Fidelity:

“Basically an in-house version of Barra,” I said. What’s Barra? he asked. It was then I realized how wide the knowledge gap was between fundamentally and quantitatively driven finance: here was an investor whom many had called a phenom, who did not know one of the industry-leading providers of optimizers and risk models.

She would soon be immersed in a much different world than the one she had known before.

Responsibilities

A member of the investor relations team told Sun during one of her interviews before being hired that “the goalposts move every day.” Her first day of work happened to be a Family Day event for the firm, and Boone emailed her a photo of his kids at the party later that evening.

As predicted, “The goalposts moved the next day.”

She hadn’t replied to the email when she first saw it. Boone told her that she needed to do so upon receiving one: “I want to know that you read everything I send.”

She had been warned by someone else in advance that “Boone cares about every detail of everything, from periods and commas in investor letters to perfect alignment of text on PowerPoints.”

And, while Sun has been described in press accounts as an assistant (and is slotted that way within the firm), the job covered a large swath of responsibilities, including some investment work and supporting another member of the team in addition to Boone. A functional list of duties, according to Sun, would be “executive assistant, personal assistant, research assistant, project manager, communications consultant.”

In sum: On call and expected to perform a wide variety of duties at a very high level.

Carbon

Unlike some other funds, Carbon didn’t limit its reach. While widely categorized as a hedge fund, it invested in venture capital and private equity as well as public securities across the capitalization spectrum.

“We’re not a hedge fund.” [Boone] paused to make sure I knew he was not kidding. “We are an investment firm.”

There was a very fast cadence, an “obsession with time,” to “speak faster, do faster, decide faster.” In all things:

What else can we do or decide on today? The rhythm of work was a constant drive to shorten the distance to decision. If you can decide on something now, do it. Don’t wait.

Carbon’s broad coverage of different kinds of equity investments, its extensive network, and its reputation gave it access to people, ideas, and data. To Sun, “Carbon felt like an international newsroom stationed inside a think tank.”

I began viewing Carbon as a decision factory, the main input of which was information — specifically, objective, and not subjective. Boone did not care about hunches, gut feelings, or intuition; he concentrated explicitly on fact-based decision-making. Your output was as good as your input, which was why Carbon paid an army of people to amass information, and why it focused on getting on the inside, on gaining access to data of all types.

Carbon also received the best corporate access, those private meetings between investors and companies. . . . Here was a feedback loop: higher quantity and quality of information allowed Carbon to make better, quicker decisions, which allowed it to generate greater, quicker profits, enabling it to spend more and more on information. Asymmetric knowledge is asymmetric power. Carbon wanted to know everything about you while you knew nothing about them.

At one point, Boone told Sun that an assistant who was leaving the firm “said she appreciated how she had a front-row seat to some of the coolest things happening in the world.” Pretty heady stuff.

The culture

As is the case at many investment organizations, there was a cultural divide at the firm. When Boone decided to have a meeting to reinforce “Carbon’s culture, values, and long-term direction,” he wanted “everyone” in attendance — “and by everyone Boone meant the investment staff.”

And that staff was predictably like that described in a previous posting, “The Homophily of Hedge Fund Culture”:

Literally meaning “love of sameness,” homophily can be more thoroughly defined as “the tendency to form strong social connections with people who share one’s defining characteristics, [such] as age, gender, ethnicity, socioeconomic status, personal beliefs, etc.”

Those supporting the investment team were seemingly a world apart from it, and relatively small in number. As such, they were surrounded by the trappings of wealth and status but not really a part of it.

For one thing, Boone was “incapable of throwing a party not to Vogue standards.” No expense was spared for firm events or meetings or anything else. Everything was fancy, even the food that routinely got tossed in the trash, uneaten. And so were the substantial gifts that Boone gave to Sun.

Boone summarized his philosophy regarding the support staff and their requests for some additional positions to relieve their workloads:

People always think the grass is greener somewhere else. They leave, they find out: it’s never greener. This is how most funds are. This is what it takes to survive. If they don’t like it, then they can leave. We know our pay is among the highest on the Street. People are paid well; some are even overpaid. Money is the only reason anyone is here anyway.

It all fit with what Boone told Sun one time, “Carrie, remember, money can solve nearly everything.” That was the organizational ethos at Carbon.

Pressure points

Even firms like Carbon and people like Boone faced times of stress when things weren’t going its way. Sun:

I was reminded that stocks are a projection of the most human aspects of us: irrational exuberance, unexplained depression, inexplicable need to achieve external validation of intrinsic value and worth. You can diversify away many kinds of risk — country, currency, industry, asset class, and factors like company size and value — but you can’t diversify away the risk of being human. And being human means that market conditions can and will affect you more than you know.

At one point, she commented on the market reaction to an earnings report by a Carbon-owned company, concluding:

A company can beat expectation and set all-time records and still be depressed.

Two pages later, in response to another earnings announcement for a portfolio holding:

A company can grow, but if it’s not in the precise directions and magnitudes other expect from it, then it can — and often does — take a beating.

If you replace “company” with “person” in those two excerpts, you can get a sense of what was starting to bug Sun. She could no longer juggle all of the balls to Boone’s expectations; she felt bedeviled by interruptions and her own mistakes — and exhausted from trying. “All I wanted was help with the work,” but Boone rebuffed her requests.

At one point, she created a “Self-Evaluation for Carrie Sun,” but it carried a subheading: “(Do Not Submit).” It was just for her, even though:

I remember staring at the document and dreaming of the freedom to share my truth.

Other things were weighing on her too:

I accepted his unreasonable requests as reasonable ones.

I had plunged headfirst into helping the rich.

I used to think that Boone was driven by a love of the game, whatever the game was, and that making money was a side effect. No. There was only money. Everything else was a side effect.

The book

Each reader will have their own interpretation of the book; it is a Rorschach test of sorts. Some reviewers see Sun’s tale as mere whining, while others think it paints an important picture of investment industry culture.

The book is a memoir, so it’s not solely a telling of Carbon and Boone, but of Sun’s thoughts and personal life, including a problematic relationship with her parents — and with her boyfriend, whose own family was worth hundreds of millions of dollars.

Michael Lewis has said he thought Liar’s Poker would be the end of something instead of the beginning of something. Many readers weren’t turned off by his depictions of life on the desk at Salomon Brothers, as he expected; they were inspired to grab for the brass ring themselves. The world Lewis painted did not fade away in subsequent years — it was supercharged.

One could imagine similar responses to this book. Aspiring Masters of the Universe wanting to be Boone — and assistants being willing to deal with the hassles in exchange for the money and the gifts and the “front-row seat to some of the coolest things happening in the world.” (And who wouldn’t want to be interviewed by the creators of Billions, as Sun was, with Boone’s knowledge, when they were thinking about adding a “right-hand-man-or-woman-type character” for the next season of the show?)

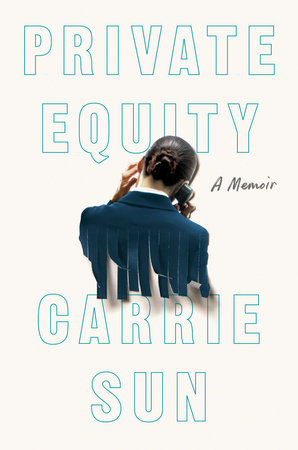

But, look closely at Private Equity‘s cover illustration. It’s an image, taken from behind, of an assistant on the phone. The lower part of the picture of her has the unmistakable parallel cuts of a shredder.

{kind=link}

In part, Sun dedicated the book to “all those who have the courage to quit.”

Due diligence considerations

Investors are presented with carefully crafted representations of asset management firms. The challenge is to find out what is real and what is not.

Books like this (and others that have been reviewed here, including a notable one about Bridgewater; see the posting) give a glimpse of the messy reality of day-to-day existence in those firms. Not that everything should be accepted as factual or accurate, but often unauthorized accounts are closer to the truth than authorized ones.

Those doing due diligence need to be able to crack the narrative and see what’s really there. It is very hard to do, but reading books like this helps to consider the range of possible dynamics at play to include in the mosaic of research.

There are always little things that surprise you, threads worth pulling on. For example, the use of AOL instant messages at Carbon:

I thought about how hard it was even for Carbon — a nimble and fast-moving crossover fund betting billions on technologies that were transforming the way people talked and shopped and worked and played — to change something as simple as its own system of communication. In AIM, at Carbon, I saw a pattern hidden in plain sight: A small decision weighed down by repetition becomes a massive habit. It becomes inertia.

And, at every firm, there are individuals going through personal struggles, who are conflicted about the business at hand, and perhaps feeling shredded themselves:

Working in an industry that trafficked in conviction, wherein ambivalence was costly and seen as a weakness — an invitation for others to take control and dominate, an effect that’s especially pronounced for women — made me feel like a fraud. Everywhere I went, decisiveness was valorized. Doubling down. Seeking closure. Being sure, settled, concluded. I sold a lot of conviction and to my surprise was not terrible at it — which made me feel like a liar.

While you can say that Sun was an outlier, an outsider, an assistant, her thoughts in that regard also plague investment professionals at times.

Realizing things like that is why you should read books like this.

The due diligence courses and other resources provided by The Investment Ecosystem help research analysts and capital allocators improve their analysis of the qualitative aspects of investment firms.

Published: August 29, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.