One specialty of The Investment Ecosystem is due diligence and manager selection. A short PDF provides a summary of some resources we offer if that’s an area of interest for you.

Active and passive (whatever they are)

CFA Institute Research Foundation released a monograph, “Beyond Active and Passive Investing: The Customization of Finance,” by Marc Reinganum and Kenneth Blay. It covers the beginnings of passive investment theory and the rise of indexation for benchmarking and, ultimately, investment. Charts and tables illustrate the trend in indexation around the world; they show that index domination at this point is mostly a one category — U.S. Large-Cap Blend — phenomenon.

In the last section, the authors look to the future and see asset managers needing to shift their emphasis:

Looking forward, asset management will continue to evolve from offering portfolio products to offering portfolio services that develop low-cost, highly customized portfolios . . . what we refer to as hyper-managed solutions.

The report relies on Morningstar data, opting to use that firm’s classification scheme for active versus indexed funds in its analysis, largely skipping over the “What is a passive fund?” question that is posed at one point.

Thankfully, that is addressed more meaningfully in another new CFA Institute publication, “Smart Beta, Direct Indexing, and Index-Based Investment Strategies: A Framework,” by Jordan Doyle and Genevieve Hayman. They argue:

Inconsistent terminology with respect to index-based products has contributed to the ambiguities surrounding their classification as active or passive investments, making it harder for investors to evaluate funds and compare products.

A conceptual framework is offered that includes four levels of indexed products, from “pure index” — those closest to the original idea of “passive” because they are weighted by capitalization, although they may be deficient in other respects — to those “indexed” products that are very much actively managed.

Among other things, the report recommends “a comprehensive regulatory framework for benchmark indexes where one does not already exist” and requirements for the managers of indexed products to provide more information “regarding indexing methodologies, including security selection and screening procedures, weighting, rebalancing strategies, and conflicts of interest.”

(A 2022 posting from The Investment Ecosystem said “we need some new terminology” to deal with the confusing descriptions in use by different parties in the investment markets.)

The market kerfuffle

The events of early August prompted banner headlines online and in print, “fear” readings off the chart, and a slew of commentary from asset managers and consultants, including from those who otherwise don’t offer much in the way of “thought leadership.”

Since these Fortnightly postings only come out every two weeks and many investments have snapped back, a large number of items that were slated to be included in this edition have found their way to the cutting room floor. In the inimitable words of Emily Litella (Google her, kids), “Never mind.”

However, here are two things that will come in handy in the future. First, from Matt Levine, a general description of market spasms:

Market crashes usually have the same mechanism. People like a thing, so they buy it, so it goes up. More people like it, so they buy more of it, so it goes up more. It goes up steadily enough that people think “ehh I should borrow some money to buy even more of this thing,” so they do. Eventually a lot of very leveraged investors own a lot of the thing. Then something goes wrong with the thing, its price goes down, the leveraged investors get margin calls, and they have to sell the thing to pay back their loans. Their losses are big enough that they have to sell other things, things that were fine, to pay back their loans on the thing that went wrong. The big leveraged investors who owned a lot of the thing that went wrong also all own the same other things, also with leverage, so there is a generalized crash in the prices of the things that big leveraged investors own.

And, a diagram of investor reactions in response to changes in the price of an investment.

Safety in numbers

Charles Skorina offered a posting called “Why take a chance?” To wit:

In theory, pensions, endowments, foundations, and the like seek active managers to obtain above-market returns. In practice, that doesn’t seem to be how it works.

A former large endowment CIO mentioned recently that his team would scour the globe for unique opportunities, but the first thing his trustees would ask when told of any rare find was “what other endowments have invested in this?”

Those tendencies are evident in hiring too. Who is willing to take a chance like Yale did forty years ago?

Let’s be honest. If the David Swensen of 1985 applied for a CIO position at Yale today, he would not survive the first round of interviews — a young untested Wall Street banker, working on something called interest rate swaps? No way.

A changed landscape

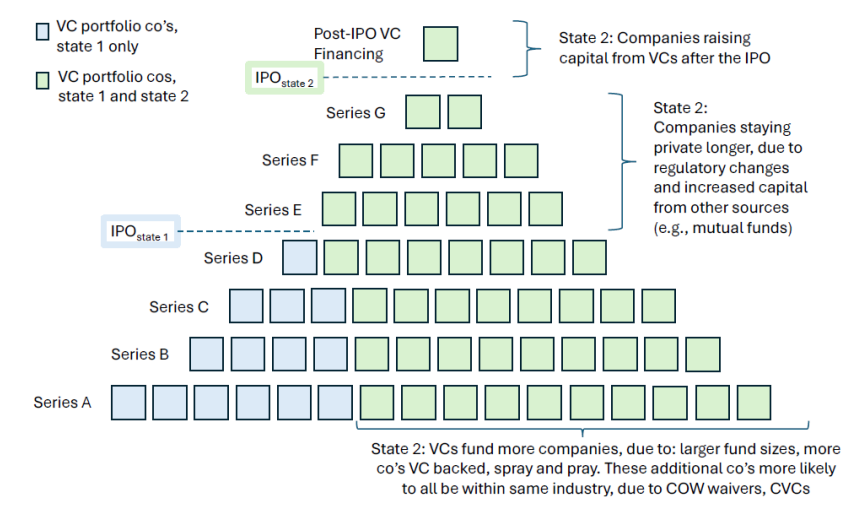

This image is from “Common Venture Capital Investors,” a paper by Jillian Grennan and Michelle Lowry. The image shows the difference between the typical venture capital funding rounds of yore versus now. Starting from the bottom, the blue boxes show how there used to be just a few rounds before an IPO. The green boxes illustrate the proliferation of additional investors and financings these days, which result in a much different cap table and a much longer wait for a public offering.

The paper looks at the changing dynamics in the venture capital industry, including increased common ownership, i.e., the investment by a VC firm in multiple startups that “operate in the same industry or product markets.” New investors, larger VC firms, more corporate VC investments, and law changes in some states have all contributed to an altered landscape for investors and startup firms.

The way of the world

For Joe Wiggins, the roller coaster of interest in ESG products is symptomatic of what happens with big ideas in investing. His recent posting boils it down into three evergreen factors:

Past performance dominates investor behaviour.

Substantial inflows erode future returns.

Asset managers will sell things that benefit them and sell them aggressively.

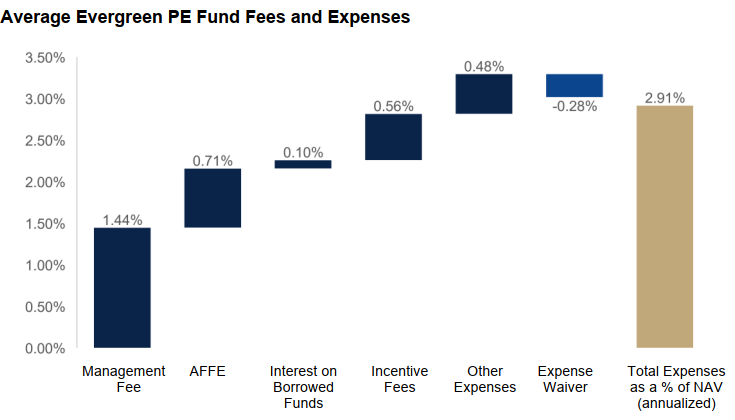

Evergreen PE fees

Phil Huber of Cliffwater wrote a summary of the fees on tender offer funds and interval funds. The average levels of fee components are shown here; each is defined in the report and a table provides the minimum and maximum values in each category. There are significant differences from one fund to another in the composition and amount of fees.

This is a relatively new but fast-growing area. The oldest of the funds has only been around for fifteen years and the average age is five.

Other reads

“Which One Is It? Equity Issuance and Retirement,” Michael Mauboussin and Dan Callahan, Morgan Stanley Investment Management.

Few investors explicitly consider the wealth transfers that a company can cause when it issues or retires stock that is mispriced.

“The Analyst’s Code,” Drew Dickson, Albert Bridge Capital. A look back at something Dickson wrote at the dawn of his career, a quarter century ago; “There is no holy grail of investing.”

“Late cycle financial innovation: Are private credit funds the new MBS CDOs?” Synthetic Assets.

Are the LPs being set up to be the bagholders in a private equity downcycle?

“If I go, you should too,” Roland Meerdter, LinkedIn. Thoughts about the related but divergent interests of institutional asset owners and asset manager salespeople — and whether the departure of the latter might provide a signal.

“The Three Types of Backtests,” Jacques Joubert, et al., SSRN.

It is evident that while backtesting is an invaluable tool, it must be utilised with care and not as the primary driver of research but rather to validate a semi-final and well-formed investment strategy.

“Texas Teachers’ growing pressure on hedge fund fees is working,” Sarah Rundell, Top1000funds. On the asset owner’s initiatives for a 1-or-30 fee structure and a cash hurdle for incentive fees. Why are many “others that are similarly inclined rooting [Texas Teachers] on anonymously”?

“The ETF industry’s shark-jumping moment,” Robin Wigglesworth, Financial Times.

Leveraged single-name ETFs incinerate investor money, make markets more volatile and are solely created to generate fees for the sponsor.

“The Impact of Misleading Corporate Communication on Stock Performance,” Lewei He, et al., SSRN. There has been an increase in misleading communication from companies; this evaluates the patterns of performance for greenwashing incidents (as well as “governance washing” and “social washing” ones too).

“The Private Funds Rule Is Dead. Now, Stakeholders Must Pick Up Where Regulators Left Off.” Thomas Deinet, Institutional Investor.

Regulators also often ignore potential tools that can create better outcomes for investors and their beneficiaries, including principles-based standards.

Being open to the new

“Living in discovery is at all times preferable to living through assumptions.” — Rick Rubin.

Flashback: Lessons from the Valley

Two people with an impact on the development of Silicon Valley passed away recently. Their stories provide lessons regarding the importance of communication.

Sandy Robertson founded Robertson Stephens, one of the “Four Horsemen” of investment banks that underwrote so many of the technology companies to come public in the last two decades of the 1900s. His obituary in the Financial Times details his career and includes a quote from Larry Sonsini, “Sandy never raised his voice, never needed to pound the table and never oversold.” A good reminder that quiet persuasion is usually more powerful than bluster.

The New York Times marked the passing of Susan Wojcicki, “who helped turn Google from a start-up in her garage into an internet juggernaut.” It included this:

Hunter Walk, a former product manager at Google who worked closely with Ms. Wojcicki, said he admired her ability to be a “translator” in navigating the many “islands, personalities and different incentives” at Google as it ballooned from a small start-up to a sprawling corporation.

“You had to convince her first, but if she believed in you and your idea, she could help translate it for Larry and Sergey,” Mr. Walk said in an email. “That was the most powerful advocacy a product leader could have on their side.”

That sort of translating is an underappreciated skill. Translators bridge the gaps between specialists and across teams and divisions of organizations, helping ideas and information flow. They also can do so with clients and prospects.

Postings

The archives include all of the previous editions of the Fortnightly, as well as original essays on important ideas from around the investment ecosystem. For example, a 2022 piece, “Looking in the Rearview Mirror,” looks at the “forced selling, margin calls, fears of insolvency, and (eventually) government intervention” related to the LDI crisis that fall. It concluded:

The leaders of organizations need to ensure that risk management gets taken to a new level, by communicating the need for change and building a culture that identifies and prepares for emerging risks before there is panic on the dance floor.

Thank you for reading. Many happy total returns.

Published: August 19, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.