Welcome to another edition of the Fortnightly, your source for interesting stories and ideas from around the investment ecosystem, (Subscribe here to receive each new Fortnightly and original essays via email.)

The most recent posting on the site, “Recognizing the Risk of Flow-Driven Performance,” looks at a new paper that analyzes the impact of inflows (and outflows) on performance for liquid strategies. That effect trips up allocators in subtle and not so subtle ways. The paper uses “bubble ETFs” to show what happens when funds have ownership stakes that are large in comparison to the daily volume of their holdings.

The investment manager playbook

A previous edition of the Fortnightly covered “The Investment Office Playbook — What Managers Don’t See,” by Ted Seides. Now he has shifted to the other side of the table, with a posting on “The Investment Manager Playbook: What Allocators Don’t See.” It is an answer to these eternal questions:

Don’t managers know size is the enemy of performance? Why are all these managers so greedy?

Which boils down to:

The investment manager’s playbook hinges on its decision to stay the same or grow. That choice carries implications for the team, investment opportunities, and risks the manager will encounter to maximize its probability of long-term outperformance.

In almost any rational assessment, the playbook favors growth. Expanding organizations can attract and retain talent and capital, which creates durability. Staying the same may benefit from focus, but it carries significant business risk.

Seides walks through two choices over time — growth or “stay the same” — to illustrate why managers choose to get bigger despite the risks to the performance of its initial strategy. The backdrop for all of it is the instability of the existing asset base because of investors who are quick to fire in response to the variability of performance (that comes with the territory of active management, although expectations in that regard are often out of whack).

While the write-up faithfully presents the mindset of managers in making the choice to expand, a couple of points of pushback:

~ The dilution of performance that (normally) accompanies larger asset sizes and the dilution of skill that (normally) results from expanding into new strategies may be acceptable trade-offs for an asset manager in order to build a more stable business, but asset owners still should be wary of those moves.

~ “Growth” need not involve just scale and complexity. Too many firms “stay the same” by not focusing on continuous improvement of their existing strategy and their communications about it.

The Baylor way

There are few asset owners who actively use social media to promote their thinking about the what, how, and why of their approach. Dave Morehead of Baylor University is one of the exceptions. His feeds on LinkedIn and “Twitter” offer ongoing perspectives on investment and organizational issues of interest to both fellow asset owners and other industry participants.

A March article by Alicia McElhaney for Institutional Investor focused on how Morehead builds his team, given that attracting talent to Waco, Texas can be a challenge. The first of three recent With Intelligence updates by Marc Hogan addresses Baylor’s manager selection process. In it Morehead describes what he says to its managers when they are hired:

In general, we are going to be taking money from you when everyone else is giving you money, and everybody hates it when you redeem. On the flip side, when they’re all redeeming from you and I’m tripling my allocation to you, you should really like that.

Years ago, Charley Ellis described the philosophy of the best institutional allocator he had seen. It was the same one as Morehead outlined. Another focus in the With Intelligence piece was Baylor’s willingness to ask more personal questions of managers than others doing due diligence. (That’s one topic in this course from the Investment Ecosystem Academy.)

Social media presence and press coverage can cut both ways, but Morehead has made a name for his school in the investment world by offering greater transparency than others. Will more take the same path?

AI corner

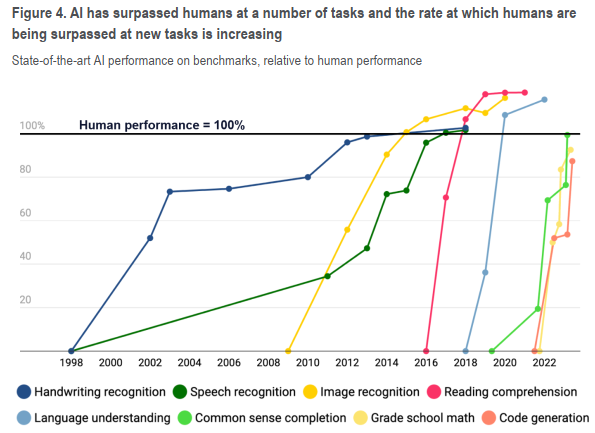

For most people, the age of AI started eighteen months ago with the public introduction of ChatGPT. This chart provides a bit more perspective on developments in the field.

It comes from Citi’s report, “What Machines Can’t Master: Human Skills to Thrive in the Age of AI.” It includes sections on competitive advantage (computers versus humans), the most valuable human skills according to a variety of experts, and the training and development of those skills.

Two other things you might not have seen. An intriguing paper by Mohammad Atari, et al., “Which Humans,” considers the implications of the narrow base for many large language models:

This systematic skew of LLMs may have far-reaching societal consequences and risks as they become more tightly integrated with our social systems, institutions, and decision-making processes over time.

And, in a posting on Marginal Revolution, Alex Tabarrok writes that “a spot-market for hiring AIs is developing.” Expertise in understanding the strengths and weaknesses of various AI capabilities will be essential (especially in the investment world).

Banks

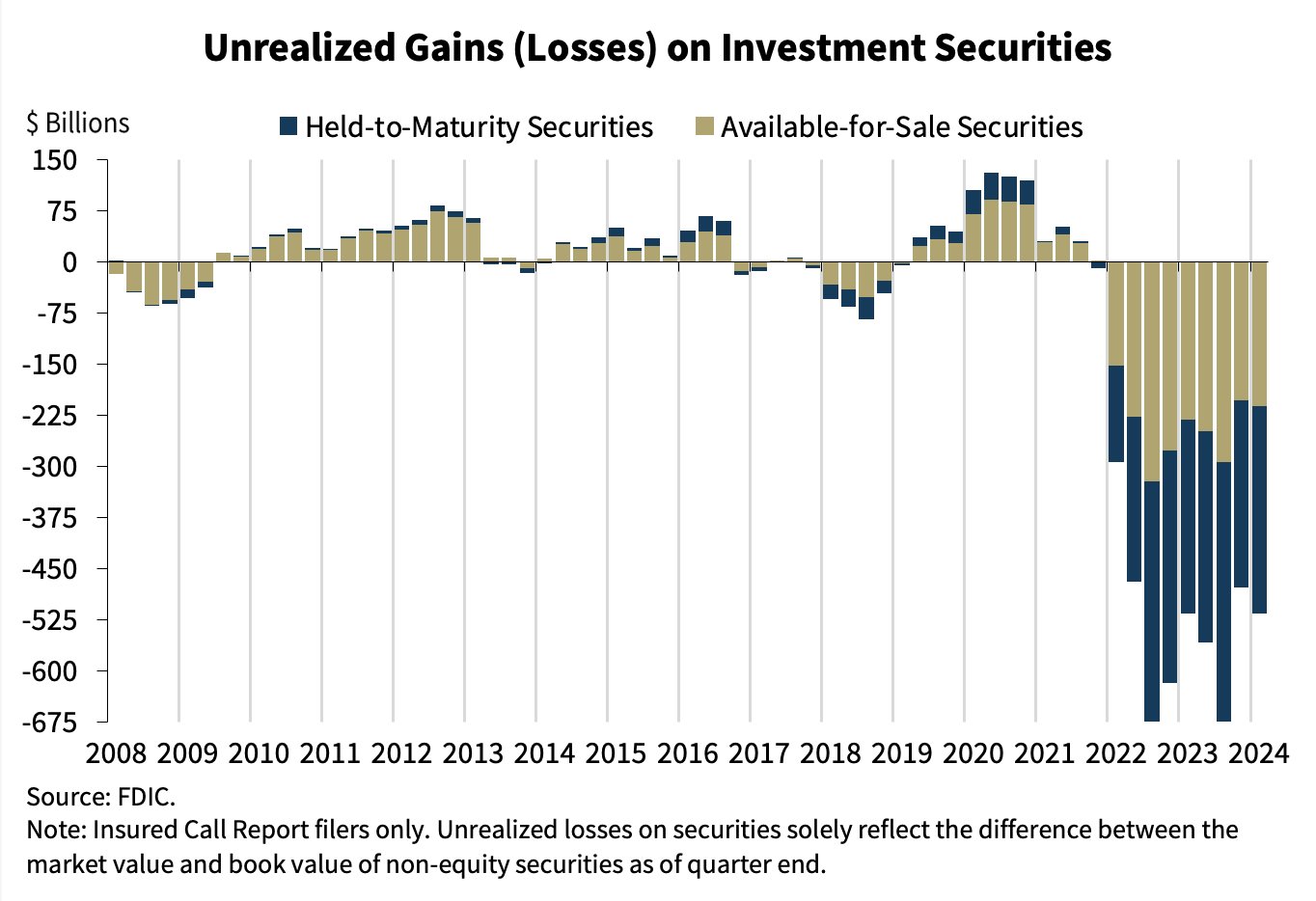

Tabarrok also posted this stunning chart of unrealized losses at U.S. banks. Ominously, that note is titled “Bailouts Forever.”

Mood

Since Ark Invest lost its mojo (by chance, its decline started within days of this early Investment Ecosystem piece), Cathie Wood has become known for her regular predictions about stocks, markets, and the economy that seem well beyond the realm of possibility. On May 23, she wrote, “In our view, the search for cash and safety in the equity markets today is as intense as that during the Great Depression in the early 1930s.”

Granted, sentiment is not always easy to divine, but since she posted that view, Nvidia is up another 25% and its CEO has gained celebrity status, including being asked to sign a woman’s chest. (After asking, “Is that a good idea?” he did it anyway.) A whiff of lower interest rates last week goosed a bunch of speculative plays. And Roaring Kitty has reanimated the meme-stock crowd.

“Is that a good idea?” would seem to be the question of the day.

Zen-like

A way to think about due diligence.

Other reads

“Stock Market Concentration,” Michael Mauboussin and Dan Callahan, Morgan Stanley.

What feels disconcerting to many investors is that the rate of increase in concentration in the last decade is the most rapid since 1950.

“Rating on a Behavioral Curve,” Utpal Bhattacharya, et al., SSRN. Analysts rate the firms that they cover relative to each other. What are the implications of that (and the opportunities presented by it) when looking across the full range of analysts?

“The Long-Run Performance of Public Pension Funds in the US,” Richard Ennis, SSRN.

We identify two distinct eras of public fund performance, separated by the Global Financial Crisis of 2008 (GFC).

“Does diversity add value to asset management?” Tommi Johnsen, Alpha Architect. A review of an academic article on diversity and hedge fund performance.

“Is ESG a Luxury Good?” David Larcker, et al., Stanford Business.

If demand for ESG follows the economic pattern of a luxury good rather than a basic necessity, boards will want to rethink how they plan, prioritize, and invest in ESG. They can expect demand for ESG will not be static but reflect whether the economic cycle is favorable or unfavorable.

“It Is (Still) Time for LP’s To Be Accountable . . .,” AIM13. “A compendium of things to look for in private equity LPAs.”

“Direct Lending Unlikely To Deliver Promised Returns,” Joseph Bohrer, LinkedIn.

Direct lending funds, desperate to invest all the money they raised, are taking more credit risk, accepting worse terms, at lower yields.

“Continuation Funds: What You Need To Know,” Greg Norman et al., Harvard Law School Forum on Corporate Governance; and “The Growing Popularity of Continuation Funds,” Hayley McCollum, Marquette Associates. Basic information about these increasingly important vehicles.

“Regarding the Usage of Cash Hurdles in Incentive Fee Arrangement,” an “open letter” from a group of large asset owners and consultants.

The long-term health of the industry is dependent on a healthy alignment of interests between GPs and LPs, and we believe incentive payments on true value-add fixes a misalignment that has been present in fee structures throughout the maturation of the hedge fund industry.

“The Investing Boom That’s Squeezing Some People Dry,” Jason Zweig, Wall Street Journal. Implications for individuals and their advisors when products that are easy to get into are hard to get out of.

Talk is cheap

“A principle is not a principle until it costs you money.” — Bill Bernbach.

Flashback: An intern at Enron

It’s intern season, which makes it a good time to read Giuseppe Paleologo’s “Memories of an Enron Summer.” The short piece recounts his time as an intern at the firm the year before it blew up.

The author captures the cultural environment there and the belief that animated Enron’s feverish rise and even more dramatic fall, but he “couldn’t understand how Enron made money.” He spreads the blame for the company’s failure more broadly than some accounts. Everyone wanted in on the game:

It was self-organizing bad behavior. What was the mechanism, though? My explanation is that Enron became very successful at something (gas trading) and as an organization it extrapolated that success could be achieved in anything it set its mind to. This enabled two classes of behaviors, each feeding on the other. First, an entrepreneurial hypertrophy, and associated excess risk taking: every new idea should be pursued, because it was new. Second, controls and processes were seen as obstacles.

Most interns are trying too hard to please those in charge to notice the incongruities around them. But, as we say around here, “all organizations are messy,” although not normally to the degree of Enron.

Postings

The archives include all of the previous editions of the Fortnightly. Among the postings are several series, including one on Bill Gross and Pimco.

Thank you for reading. Many happy total returns.

Published: June 10, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.