Coming up soon, an essay about an in-depth proposal on how AI should change the organizational design of asset management. (Subscribe so you don’t miss it.)

Speaking of missing, did you see the latest edition of Clippings? Take a quick look at a great selection of investment graphics.

The big rocket

There it is on the launchpad. The big rocket. Soon there will be a countdown, to the rapt attention of observers.

Will the big rocket blow up or soar?

That’s the question of the day; as SpaceX prepares to go public, it is dominating the investment news cycle. So many stories and so many angles. Just a few of them:

The 23 underwriters are banging the drums, which reminds Rupak Ghose of the dot-com bubble and how “some things have changed, but others are the same.” In the “same” category, analysts are crawling over each other to proclaim outrageous projections for SpaceX.

Regarding the proposed valuation, Aswath Damodaran came up with an estimate of fair value around 70% of the rumored IPO price, while Morningstar’s is about 50% of it, even though the research firm gave the company “a lot of benefit of the doubt in two of the three scenarios” that were used in its blended approach to valuation.

But does valuation even matter? Certainly it hasn’t for Tesla, no matter its sluggish results of late. Ludovic Phalippou offered a dialogue which reveals that it’s not the facts and it’s not the numbers and it’s not the valuation that matter, it’s the story. Elon Musk is a master at spinning them.

Other big firms are seeking new equity funding too. OpenAI and Anthropic are teed up to go public. Alphabet just had a big equity raise and Meta is considering following suit. The ducks are quacking, as they say on the Street, so it’s time to feed them. Whether all that supply will matter now is a good question; eventually it usually does.

One surprise was that, as other index providers were falling all over themselves to make SpaceX eligible for inclusion in their products, S&P, the most important of them of all, said it wasn’t going to change its rules to accommodate the firm. Phil Bak was among those celebrating S&P for taking a stand.

The IPO is coming at a time when we are starting to hear concerns about tokenmaxxing and whether there is an adequate return on investment from AI initiatives. Gary Marcus wonders about SpaceX’s recent deals to lease out GPUs to others and what that says about the company’s AI prospects:

Last year, people had to steal GPUs from armored trucks. This year, SpaceX’s AI division is leasing GPUs left, right, and center, because they can’t figure out what to do with them.

Finally, Rod Dubitsky provides a review of SpaceX overall, with an emphasis on its governance issues. (Among the red flags, “The S-1 is a masterclass in conflicts of interest.”) His headline calls the deal “SpaceX and Wall Street’s Middle Finger to Retail Investors.”

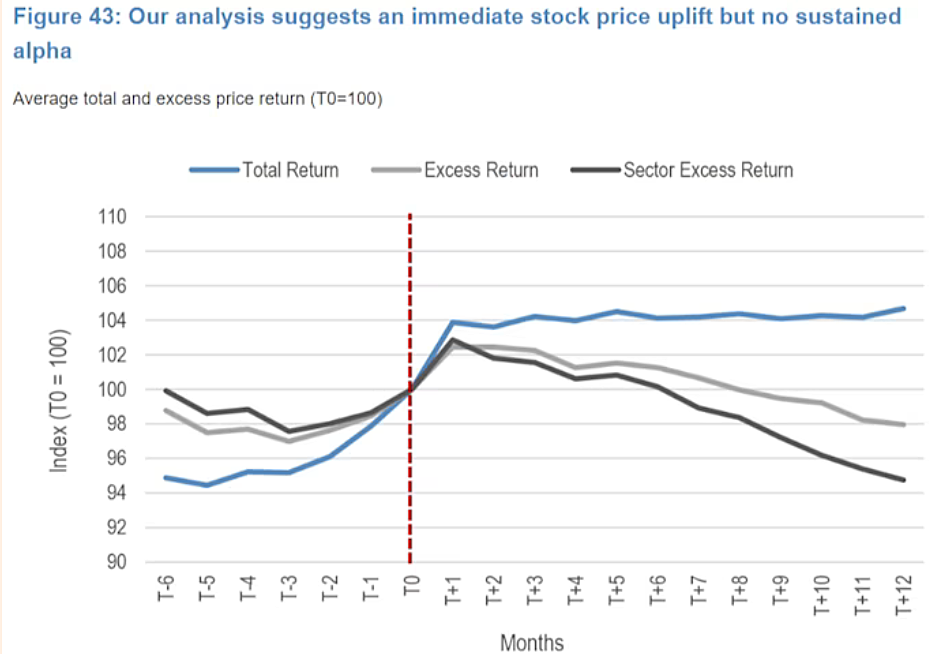

Activists

An FT Alphaville posting from Bryce Elder reviews a report on activist investors from J.P. Morgan. It’s titled “Most activist investors are not really activist investors.”

During the eight years Morgan reviewed, the vast majority of “activists” were only involved in one or two activist endeavors. However there is a small subset who truly deserve the name, led by Elliott Investment Management, which was active in more than 140 situations.

The above chart shows that overall the results from activist campaigns have been subpar. Another chart for just the “core activists” looks slightly better, but not very impressive at all.

Valuation as mindset

A short whitepaper from Divyanshu Verma, “Valuation as Mindset: Subjectivity, Dynamism, and Probabilistic Thinking in Equity Valuation,” provides an overview of some basic concepts that are too often ignored in investment practice.

The central argument is that valuation, done well, is not about computing a precise intrinsic value — it is about developing a rigorous, probabilistic understanding of a business that is continuously updated as new information arrives. In this sense, valuation is less a calculation and more a mindset: a systematic way of thinking about businesses, capital allocation, risk, and the relationship between price and worth.

Verma references Ben Graham as saying that “the goal of security analysis is not to identify the precise value of a security, but to determine whether its value is substantially higher or lower than its price.”

The questions that a rigorous valuation practitioner must ask before acting on an apparent mispricing are: (1) What specific information or analytical insight supports the view that the market is wrong? (2) What is the time horizon over which the mispricing is likely to correct? (3) What is the risk that the mispricing reflects a genuine deterioration in value that the analyst has not yet incorporated? (4) What is the cost of being early — that is, of being right on valuation but wrong on timing?

(#2 is notably mushy in both sell-side reports and buy-side recommendations.)

Other quotes:

The inputs to a DCF model — revenue growth rates, operating margin trajectories, capital expenditure assumptions, terminal growth rates, and discount rates — are all expressions of the analyst’s beliefs, information set, and, often, incentive structure.

The discipline of valuation parsimony — using only the most essential variables to construct a range of plausible outcomes –produces several practical advantages.

Decision-makers systematically overweight available information and underweight base rates and structural uncertainty.

The periods of maximum opportunity are typically periods of maximum discomfort.

Service providers

DiligenceVault published a pair of postings about the web of vendors that supports institutional investment: “The Fund Service Provider Map” and “How Fund Service Provider Diligence Has Evolved.”

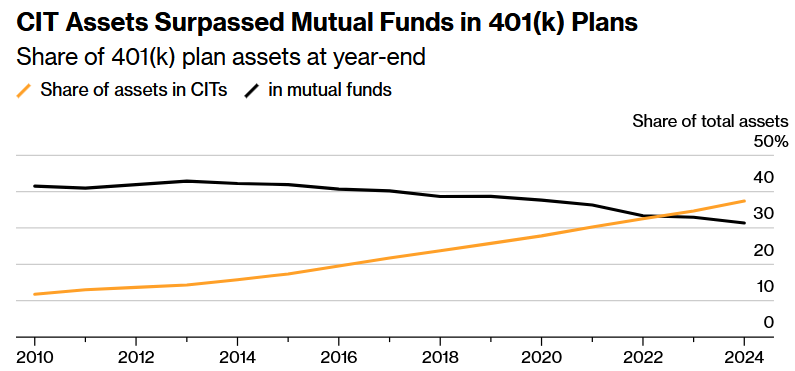

Collective funds

In the early years of defined contribution plans in the United States, collective investment trusts had a healthy market share. Then came the glory days of mutual funds when participants wanted to hold popular funds in their retirement accounts. But there has been a steady move back to collective funds, as shown in this Bloomberg chart, and they now eclipse mutual funds within DC plans.

The article from which it comes calls them “opaque trusts,” pointing out that they have different regulations and “weaker disclosure and liquidity standards,” as well as lower fees (something appealing to plan administrators, given litigation over the selection of expensive funds).

A more detailed review can be found in a paper by Natalya Shnitser, “Shadow Shareholders: The Emergence of Collective Investment Trusts as Institutional Owners.” For example:

The lack of transparency around CITs as shareholders has also obscured the relationships among — and potential conflicts of interest involving — corporate management, corporate-sponsored retirement plans, and the CIT providers that simultaneously hold corporate shares and provide services to corporate retirement plans.

The name promotes

A March issue of the Fortnightly included a section about “how a number can survive in popular discourse even as its context disappears.” Tim McGlinn of TheAltView highlighted one such (misleading) number from Blackrock that has spread widely and been used to promote the use of alternatives in defined contribution plans.

McGlinn is back with another posting on “alts propaganda,” this time how “Georgetown research” is used to support the cause.

Other reads

“The Peculiar Market for Alpha,” Byrne Hobart, Capital Gains.

Providers of capital are in a tough situation where they face constant adverse selection. For every strategy, they have to answer the question of why someone would let an outsider reap some of the profits, and, further, why they happen to be that outsider.

“Painful rules,” Shitty Situations. A terrific set of observations for credit investors (many of which apply to other kinds of investors too).

“Please, Stop Chasing Fund Performance,” Joe Wiggins, Behavioural Investment.

Even investors who sincerely try to avoid performance chasing find it extraordinarily difficult when it is such a powerful industry norm. Everyone is happy when you sell a struggling fund or buy into one topping the performance charts, despite the evidence suggesting that this is unlikely to be a good idea.

“Go big or go home,” Charles Skorina. The pieces of the puzzle at the WashU endowment.

“Cluster Strength as a Moderator of Porter’s Five Forces,” Hema Raju Barri, SSRN.

The central argument is that regional cluster strength does not merely provide background context; it alters the intensity of the competitive forces themselves.

“Am I Ready to Launch?” John-Austin Saviano, ThreeStone. Thinking about hanging out your shingle as an asset manager? Here’s a “readiness assessment” for you.

“Marked to Faith,” TSCS.

The retail vehicles, all of them, agree with each other to within roughly half a point. They disagree with the market by twenty-four.

“Built to Disagree: How Institutional Investment Management Is Designing AI That Challenges Itself,” Rafael Febres-Cordero, LinkedIn. How AI is being used at three asset managers.

“After the Professionals: A Founder’s View of AI and the Restructuring of Work,” Lukas Swid, SSRN.

Artificial intelligence is not replacing skill levels. It is collapsing the value of structured work, defined as work in which the structure itself is what the buyer was paying for, regardless of whether that work was historically performed by a high-school graduate or a doctoral specialist.

Keep improving

“If it works, it’s obsolete” — Marshall McLuhan.

Flashback: Go-go years

Investors are always looking for past market environments to compare to today’s. According to “Palmy Days and Low Rumblings,” a posting from Lewis Enterprises which reviews The Go-Go Years by John Brooks, “the 1960s remain largely unexamined” in that regard, which is unfortunate.

For example, “Ross Perot was a stock promoter’s dream.” When he brought EDS public, the market was trading at 16 times earnings and the firm had $1.7 million in profits. But Ken Langone shepherded an IPO priced at 120 times earnings, with a very small float, arguing that the price would be supported “by the investment banks that would bring the shares to market.” (Sounds familiar.)

And then there was Jimmy Ling, “a Muskian character . . . with a knack for complex deal-making that created the hydra conglomerate Ling-Temco-Vought.” At LTV:

The smashing together of disparate business lines had a poor track record of success but with enough managerial promotion the strategy could still entice investors.

The go-go years led to that famous concentration of one-decision stocks, the Nifty Fifty. Then came a horrible period for financial assets, as inflation spun out of control during the 1970s.

A pension plan soap opera

A 2022 piece on this site, “Lessons From a Pension Plan Soap Opera,” reviews the travails at the Kentucky Retirement System.

State pension plans are some of the largest investors on the planet, and are among the most visible, in that many of them are required to publish details of their portfolios and operations online. They are also in the crosshairs during some political battles, most recently regarding ESG, and often have governance structures that are less than ideal.

Elements of the Kentucky story are recounted in the posting, as are communication, due diligence, and governance lessons from it.

Thanks for reading. Many happy total returns.

Published: June 8, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.