Welcome to another edition of the Fortnightly. If you subscribe you’ll get these compilations in your inbox every two weeks, providing you with links to interesting investment readings, along with a little commentary.

You will also see original work, the most recent piece being a posting about the “professional strangers” of due diligence.

In a few days, the first installment of Investment Ecosystem Clippings will be issued on Substack. You can sign up for it now.

The theme of this edition comes from the first section and applies broadly throughout.

Fairy tales and marvels

In his latest posting, Aswath Damodaran explores the logic of trillion dollar market capitalizations. Regarding our fascination with certain levels:

From a rational perspective, you could argue that these thresholds (billion, half a billion, trillion, etc.) are arbitrary and that there is nothing gained by focusing on them. [In a previous post] I argued that crossing these arbitrary thresholds can draw attention to the numbers, with the effects cutting both ways, drawing in investors who regret missing out on the rising market cap in the periods before (a positive) and causing existing investors to take a closer look at what they are getting in return (perhaps a negative).

Rather than giving answers, Damodaran offers the concept of “breakeven revenue” as one way to think about the reasonableness of a current valuation. In turn, that leads to the 3Ps he uses to consider likelihood — is it possible, plausible, or probable? — a construct that can guide all sorts of investment discussions about fairy tales and marvels and all those routine ideas in between.

He closes with some general conclusions, including that a highly priced stock does not necessarily equal an overpriced stock. And that “investors at many tech companies, including most on the large cap list, have given up their corporate governance rights, often voluntarily (through the acceptance of shares with different voting rights), to founders and top management in these companies” — a couple of whom are cited as “more emperors than CEOs.”

Risk management

The Thinking Ahead Institute issued a report called “Fresh snow | risk management for investment systems.” The thesis is that traditional risk management — what the report calls risk 1.0, which started seven decades ago with Harry Markowitz — is no longer fit for purpose:

The main difference between risk 1.0 and risk 2.0 is the underlying model of reality. Newtonian physics for 1.0, and complexity science for 2.0.

While it is almost never highlighted by strategists, chief investment officers, and product providers, the quantitative work that underlies typical risk management is merely “simplifying a small subset of reality,” which is unlikely to be repeated.

That point is brought home by short summaries of five market spasms — exactly the kind that are used in risk management exercises for “what would happen if” examples. But they hadn’t happened before they did real damage and the next big surprise will be a brand-new one too.

Each of the five past events includes a summary of the risk 1.0 assumption that was violated, the results that were unexplained by it, the model blindness involved, the inadequacy of VaR to manage it, and neglect of the systemic risk that resulted from it.

For working within a complex adaptive system, the risk management tools that are deemed to be state of the art aren’t good enough.

More bubble talk

The last edition of the Fortnightly had a section on bubbles. Not to overdo it so soon, but Howard Marks issued a new memo on the topic shortly thereafter. He did his normal good job of thinking about the possibilities, including by asking an important question: “Who can identify the boundary of rationality?” (Speaking of fairy tales.)

Among the important ideas discussed are the differences between “mean-reverting bubbles” and “inflection bubbles;” the specific areas under bubble watch today; the “circular deals” that are becoming increasingly prevalent; and the recent surge in debt financing — and special purpose vehicles — for data centers:

Is it prudent to accept 30 years of technological uncertainty to make a fixed-income investment that yields little more than riskless debt?

The tone of the postscript to the memo is notably different than found in other investment writings — and it has received a lot of attention as a result. Marks called the outlook for employment as a result of AI “terrifying.” And:

Finally, I’m concerned that a small number of highly educated multi-billionaires will be viewed as having created technology that puts millions out of work. This promises even more social and political division than we have now, making the world rip for populist demagoguery.

Active mutual funds

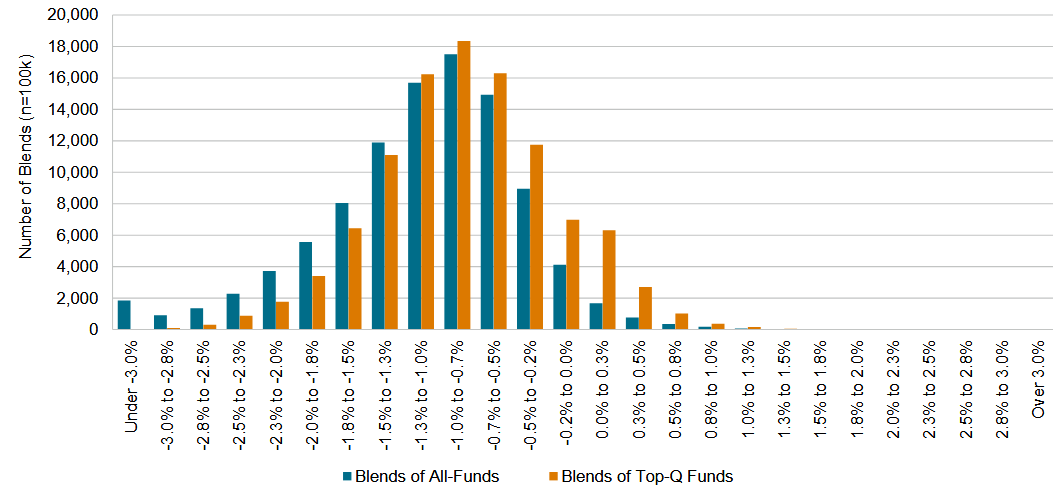

A new report from S&P Dow Jones Indices addresses the question “How do portfolios of active funds compare to similarly weighted blends of indices?”

The report offers a number of different ways of looking at the possibilities. The chart above shows the relative returns for random mixes of funds versus an indexed portfolio (using the same category allocations between the two to keep them comparable) for the decade ending in 2024.

As would be expected based on the underperformance of individual funds versus their categories, the histogram is heavily skewed to the left of zero, indicating that the active fund portfolios lag the indexed ones a high percentage of the time.

The blue bars show the results when drawing from all available funds. The orange ones illustrate blends that only choose top-quartile funds for the five years ending before the measurement period started (mimicking the approach of many allocators of capital).

The latter strategy is better than drawing from the whole universe, but the results are still overwhelmingly subpar. As has been shown in other studies, that improved outcome “had more to do with screening out the worst performers than it did with more frequently choosing alpha-producers.”

Also, if you’re wondering where due diligence might pay off, “the identification of outperformers among International Funds offered the highest positive impact at the portfolio level.”

Independent asset managers

Dave Finstad wrote an article about the due diligence of asset managers and the challenge of identifying those that will be good partners:

One thing that I can say that did help explain future performance was employee ownership. In my experience, I found that employee-owned firms had a stronger culture and were able to attract and retain superior investment professionals compared to those firms with little to no employee ownership.

They also tend to be more focused on generating performance than on gathering assets.

His views are backed up by empirical studies. In addition, surveys (including ones at Investment Ecosystem presentations, workshops, and via the online course) have shown that employee-owned firms are favored overwhelmingly by due diligence analysts. But they have a hard time building out portfolios dominated by those kinds of organizations because they are becoming scarce, which makes Finstad “a little sad.”

Mystery versus mastery

Earnest Sweat of Groundwork published a posting called “The Jason Kapono Problem.” In it, he used the basketball player in the title to illustrate a problem that he sees in venture capital. Namely, that investors often prize mystery over mastery, lottery tickets over deals with real results and better odds of success. The latter “often get scrutinized more heavily than the buzzy phenoms”:

We are in a moment where the hottest AI companies look like high school phenoms. They show up to demo day with vibes, velocity and a spreadsheet full of inbound from hyperscalers. The market squints and sees a projected future All-Star. Maybe Hall of Famer.

The unknown becomes the valuation.

Timing is everything

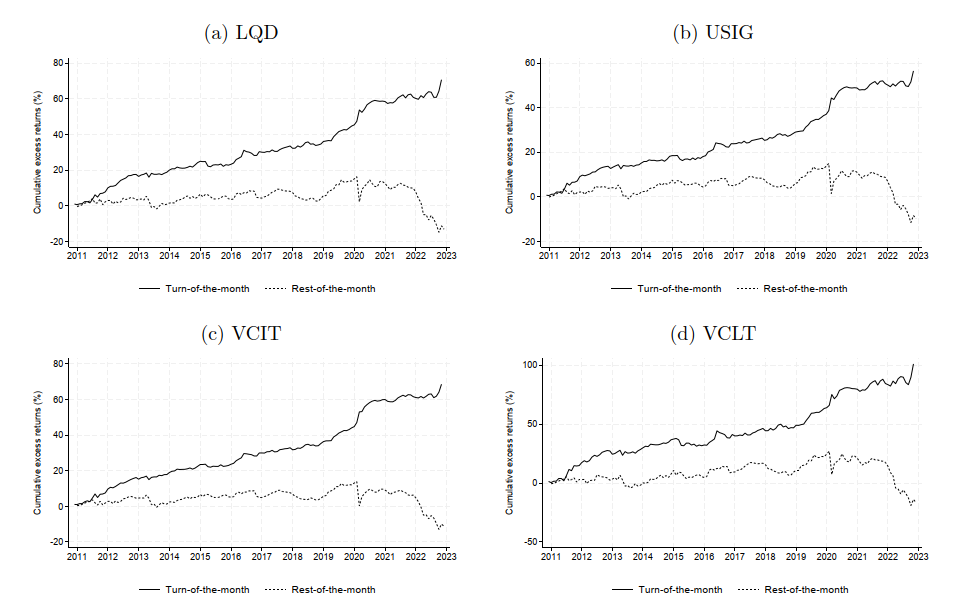

A paper by Clemens Sialm, et al., “Recurring Demand for Corporate Bonds,” states that “nearly all of the credit premium of investment-grade corporate bonds is earned during a narrow window around the turn of the month.” Why?

This pattern can be explained by the monthly bond mutual fund reinvestment cycle, which is driven by the rebalancing methodology of the main bond index benchmarks.

Shown above are the returns for four investment grade bond ETFs. The solid line in each graph shows the return from investing during that window.

Given the propensity of market participants to close windows of opportunity once they have been broadcast, it will be intriguing to find out what happens to this anomaly in the years to come.

Other reads

“The rise of proprietary capital,” Rupak Ghose, Rupak’s Substack.

If internal capital grows to be a majority of AUM, is it still worth running external money? How do you balance returns and the increased focus on Sharpe ratios benchmarked against the pod shops?

“Venture’s Media 2.0 Moment,” Rohit Yadav, All Things VC. Branding has become a big thing, since “the story is the strategy.”

“Everyone’s at the Party — Fortunately and Unfortunately,” Georgina Tzanetos, CAIA Association.

In short, the music is still going, but success in 2026 and beyond will hinge on discipline, transparency, and knowing when to step back from the noise. Dystopian author Kurt Vonnegut once said, “Dance first, think later,” but in private markets, that mindset has run its course.

“Investors Must Scrutinize ‘Performance Detractors’ in Semi-liquid Private Markets,” Henry Cotton and Bradley Budd, bfinance. Dividing potential detractors into “performance drags” and “performance risks.”

“How liquidity killed diversification,” Phil Bak, BakStack.

Only one trade remains, and all of your fancy models and static correlation matrix data can be tossed in the trash. One trade remains, and it’s the only one you need to focus on. Risk-on, or risk-off. That’s it. That’s all that matters. And that’s all that remains of Modern Portfolio Theory.

“The Psychological Burden of Concentration,” Adam Wilk, MicroCapClub. With a concentrated portfolio, can you “sit with discomfort long enough to let real compounding work”?

“Canada Pension Giant Balks at Paying Fees to Co-Invest With Private Equity,” Swetha Gopinath, Bloomberg.

Large pensions and sophisticated investors like CPPIB have for decades jointly invested with buyout firms in marquee transactions on a no-fee, no-carry basis. An influx of capital from wealth channels now threatens to change that dynamic.

“How Banks Exploit Your Psychology,” Larry Swedroe, Larry’s Substack. The “anatomy of financial exploitation” in yield enhancement products.

“A Century of Cycles: Five Lessons from Jim Grant,” Excess Returns.

“Do not stand in line to make an investment.”

In market tragedies too

“What destroys the characters of tragedy is their refusal to let it be, their stubborn insistence on their own ideas, their own wills.” — Alexander Leggatt.

Flashback: ESG forecasts

In November 2021, the Wall Street Journal published “Where Will ESG Investing Be in Five Years?” The subtitle:

We asked 10 experts to look into their crystal balls and predict the fate of socially responsible investing. They had some very different views.

Yes they did. You can see the optimism of the time, as well as the emerging concerns. What isn’t there? Forecasts of the political backlash that disrupted the trends that were in place.

Regime change

Early in the history of The Investment Ecosystem there were postings that appeared under the heading “Charts.” One from April 2022 featured some images related to the apparent end of the “one-way move in bonds for four decades.” It included looks at the correlation between bank stocks and interest rates, the performance of growth versus value, and this one, showing the trajectory of inflation and interest rates:

We know now that those levels of inflation pulled rates higher. Despite some contrary indications, it seems like the weight of the evidence is that we have moved to a new market regime after a very long time.

Thanks for reading. Many happy total returns.

Published: December 15, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.