Sometime soon, there will be a new Investment Ecosystem outpost on Substack. But nothing will change in the existing setup. You will still see the regular IE fare (sets of curated links like this one and essays about the changing investment world) in the same places (online or via email) as you do now.

The Substack will be an add-on offering. Called Investment Ecosystem Clippings, it will be just that — snippets of text and images found elsewhere that are worth sharing. Quick to review but likely to get you thinking.

Clippings will be free and if you’re interested, you can sign up now so that you’ll get the first issue when it is published.

Now, on to the readings.

Questioning the convergence

The convergence of public and private investing is a major theme across asset classes. Institutions are managing portfolios differently and structuring their organizations differently in response to the decreasing separation between the two categories of assets.

The so-called democratization of alternatives is a big factor in the convergence, as the investment industry pushes hard to get private investments into retail channels of distribution, including defined contribution plans.

But that’s where things get messy.

For example, see “Evergreens: The Tree That Never Sheds,” a report from EDHEC by Evan Clark which focuses on the perpetual funds that are attracting assets:

These vehicles promise access, convenience, and periodic liquidity — but closer analysis reveals structural features that pose material risks for investors.

The concerns are summed up in the details behind five bullet points, each of which is addressed with helpful exhibits:

Performance driven by unrealised gains

Fee misalignment

Illusory risk-adjusted performance

Liquidity mismatch

Governance conflicts

A new paper is drawing attention to another potential hurdle for “the convergence,” as indicated by its title, “Private Equity, Public Capital, and Litigation Risk.” The authors, Ludovic Phalippou and William Magnuson, begin their conclusion in this way:

Private equity has long operated with limited transparency, minimal regulation, and contractual insulation. That equilibrium is now shifting.

Said another way:

As retail exposure to private equity has grown, the line between stylized financial storytelling and actionable fraud has narrowed.

The customs and legal agreements of the institutional world, shaped in no small part by the desires of limited partners not to get shut out by the most attractive general partners, will come under increased scrutiny:

Practices normalized in institutional settings — misleading performance metrics, manipulable valuations, opaque fees, limited liquidity, and fiduciary duty waivers — become significant litigation risks when ordinary investors enter the picture.

Foremost among the many issues is the fact that “private equity formation documents frequently limit or entirely eliminate the fiduciary duties that managers owe to their investors.”

For one example of the disconnect, the law firm Carlton Fields recently released “Alternative Retirement Plan Investment: The Checklist,” in response to a change in guidance for pension plans from the Department of Labor. Note the emphasis on fiduciary duties found there.

A posting from Tim McGlinn of TheAltView reveals how BlackRock appears to be dealing with this issue in target date funds that include alternatives — by trying to offload its fiduciary duties to others. It does not do that in its alternatives-free target date funds.

All of the wondering about whether this convergence will be a good thing is not concentrated on the retail side of the fence. A commentary by Chris Cumming in the Wall Street Journal (“Private Equity’s Embrace of the Mass Market Alarms Longtime Investors”) starts simply: “Private equity’s old money is not happy about the new.”

Institutional investors fear getting crowded out of deals, as well as the possibility that the money chasing private equity will erode returns available to them — and say they are willing to alter allocation decisions as a result:

Eighty-three percent of these private-equity heads told ILPA they would be less likely to invest with a manager that took in large amounts of capital from individuals.

Bubble watch

Another popular topic these days: bubbles. Here are a number of readings along those lines.

GMO has warned of bubbles off and on for quite some time. A quarterly letter (“It’s Probably a Bubble, but There is Plenty Else to Invest In”) by Ben Inker offers a “taxonomy of bubbles,” which includes illustrations of the risk-reward trade-offs (as seen by the firm) in four recent bubble environments. They term them the internet bubble (2000), the “everything” bubble (2007-8), the duration bubble (2021), and the AI bubble (now). Regarding today’s version:

Plenty of other risk assets are trading at fair or even compelling valuations, and even if today’s financial markets turn out to be rationally priced, there is no long-run expected return give-up for tilting your portfolio away from the AI darlings and into those other assets.

Rajiv Jain of GQG is known for his willingness to go against the crowd at times. In September, the firm published a posting, “Dotcom on Steroids,” that argued that the technology sector “stands at a significant inflection point,” featuring “the trifecta of rich valuations, increasing macro risk, and — perhaps most importantly — deteriorating company fundamentals.” Comparisons are made to address what it feels are misperceptions about the quality of today’s tech companies versus the dotcom era. A second part with the same title was recently released; it focuses on OpenAI and the exuberance for the company that “seems to overlook the fundamental fragility of the current business model.”

On the other side of the argument is Owen Lamont of Acadian. “Firms are the smart money,” he wrote, observing that we aren’t seeing the stock issuance that marked the dotcom era:

Let’s conclude by considering the claim that the U.S. is currently experiencing an AI bubble similar to the tech-stock bubble. I’m skeptical, because today I don’t see a lot of equity issuance by AI-related firms. In contrast, as of 1999, technology firms were issuing equity hand over fist.

Lamont expanded on that argument in a follow-on posting, in which he acknowledged that the situation can change relatively quickly, as it did from March 1999 to March 2000, when issuance increased dramatically over that year.

For research into bubbles, check out the links from The Capital Spectator and the “short field guide to bubbles” from Alpha in Academia. The latter also includes examples featuring technical analysis, which some think can help in evaluating bubbles.

Following the evidence

In a posting on his blog Behavioural Investment, Joe Wiggins asks an important question: “How Can Investors ‘Follow the Evidence’?”

“Evidence-based investing” became a popular phrase over the last two decades, making it all sound so easy. But Wiggins puts the desired goal into proper perspective:

A robust piece of evidence may directly contradict another equally strong argument. Investment decision making is about understanding what we are trying to achieve, assessing the available evidence and drawing a necessarily uncertain conclusion.

He provides a number of good examples, including that of using a static asset allocation or varying exposures based on valuation. Good arguments can be made for either; “If we are following the evidence, what should we do?”

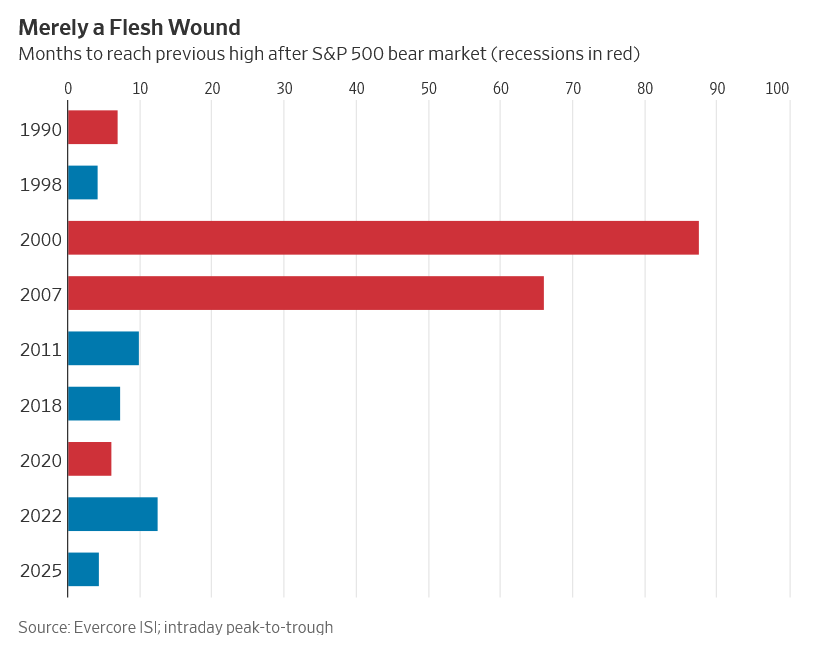

Barely bears

It is common in the financial media to call a drop of 20% a “bear market” — a level of precision that doesn’t really tell you much. But that “unofficial definition” is handy to gauge the length of those drawdowns, like the chart above, which appeared in a Spencer Jakab column in the Wall Street Journal. (Periods that included a recession — also an imprecise definition — are shown in red.)

The piece was titled “Why We Could Use a Good, Long Bear Market.” We’ve had two of those this century, neither recently. Jakab wrote that they can be “both awful and therapeutic”:

Long bear markets accompanied by a recession discredit the last boom’s wildest themes and its cheerleaders. They also remind us of what capital markets are for: matching mostly good businesses with patient savers’ nest eggs.

The optimism premium

Are you concerned about lists of equity valuation statistics showing that a great many of them are higher than at other times in modern market history? Head on over to Hudson Bay Capital for a dose of wishful thinking.

“No, Stocks Aren’t in a Valuation Bubble — Not Even Close,” screams the title of a piece by Jason Cuttler, the firm’s senior markets and derivatives strategist (although the disclaimer says that it “does not necessarily reflect the view of Hudson Bay Capital”). He sees the fair value for the S&P 500 at $9,000 in an “optimism regime,” writing that “such outcomes are consistent with President Trump’s ‘MAGA’ policy goals,” and that:

Investors who myopically focus instead on the recent history of P/E multiples risk missing out on such generational upside.

Nouriel Roubini of the firm offered an optimistic economic outlook with many of the same themes but in a more muted fashion. He thinks that “US exceptionalism is intact” and that “deep pessimism about medium term US growth and returns is unwarranted,” although he cites more caveats to the potential growth surge he sees coming. Chief among them is that “some policy proposals — if fully implemented — would justify a more stagflationary outlook.” Not to worry, though:

Four guardrails have become increasingly binding against stagflationary policies: market discipline, Fed independence, strong and market-savvy economic advisors, and a limited Republican majority in Congress.

Judgments about those “guardrails” animate today’s market debate.

(A tip of the hat to Toby Nangle of FT Alphaville, who wrote a longer summary of Cuttler’s piece.)

Junk chart

A Bloomberg article about the strong weekly finish to November included this image, which deserves a place in the junk chart of the year contest. Adding the returns of five assets together is certainly a novel concept, but a meaningless one. Hopefully we won’t see it again.

A Bloomberg article about the strong weekly finish to November included this image, which deserves a place in the junk chart of the year contest. Adding the returns of five assets together is certainly a novel concept, but a meaningless one. Hopefully we won’t see it again.

Other reads

“Hedge Funds Call This Psychologist When Their Traders Start Losing,” Gregory Zuckerman, Wall Street Journal. Dave Popple:

[Top hedge-fund traders] are the rare overlap of leaky attention, which allows them to pick up signals others miss, and strong discipline and willpower.

“Why Smart Investors Choose Not to Play, The Case Against Active Management,” Larry Swedroe, Larry’s Substack. A case study in institutional advantage leading to unfavorable outcomes — wrapped in an analogy regarding the benefits of carding a par on every golf hole without really trying.

“Ethical firms are more likely to merge,” Joachim Klement, Klement on Investing.

Indeed, there is a kind of self-sorting among firms where some firms disproportionately attract employees with many ethics violations. Over time, the industry thus splits into companies with high integrity and companies with a lack of integrity.

“How Journalists Are Becoming the New Power Hire in Private Funds,” Jake Conley and Shahrukh Khan, Cash and Carried. Searching for talent “to extract information that hides behind numbers, or that numbers don’t pick up to begin with.”

“Multistrategy hedge funds are hiring armies of insufferable clones,” pseudonymous author, eFinancialCareers.

Difference was what once made the hedge fund industry great. Now there’s just an army of clones.

“Blue Owl’s Failed Merger and Cracks in Non-Traded BDCs,” Covenant Lite. On the firm’s reversal of its plan to merge a public business development company and a private one, and what it means for the sector.

“A Risk Professional’s Guide to Physical Risk Assessments,” GARP Risk Institute (for the Climate Financial Risk Forum).

Physical risk assessments are likely to become an increasing influence on day-to-day risk management, and it’s important for all financial institutions to grow their understanding and insight into how their portfolios are likely to be impacted.

“Behavioral Finance,” Simon Hallett and Tim Kubarych, Harding Loevner. Short videos about “the common cognitive biases that affect all investors” and how one firm aims to mitigate them.

The illusion of knowledge (including about quotes)

“The greatest obstacle to discovery is not ignorance — it is the illusion of knowledge.” — Daniel Boorstin (although it is most commonly attributed to Stephen Hawking, who may have repeated it later).

Flashback: Motif Investing

Motif was an online brokerage, in operation from 2012 to 2020. It was chiefly known for the ability to buy “motifs,” thematic baskets of stocks that could be bought or sold via a single trade, as well as other innovations.

But it couldn’t survive against the established players in the industry, especially after the move to low- and then zero-commission trading. Its intellectual property and technology assets were sold to Schwab after it closed down.

The proliferation of ETFs has meant that there’s usually one that fits the bill for any thematic idea you might have. If not, improved technology and fractional trading at most brokers means that it’s possible for you to execute on motifs you dream up.

(Studies of thematic fund performance have shown that they rarely outperform standard indexes, since they usually become available after optimism around a theme is already priced in. And, the funds have a high closure rate, since assets flee after the flame is gone.)

Oddly, the Motif Investing home page still appears as it did five years ago, although none of the links work.

Quality shareholders

The topic of “quality shareholders” was the subject of an early Investment Ecosystem essay. It featured ideas from Lawrence Cunningham and Philip Ordway, a link to a discussion between them, and a series of questions for those who work at asset management firms. Those investors face challenges to acting as quality shareholders and, similarly, attracting quality investors themselves.

Thanks for reading. Many happy total returns.

Published: December 1, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.