Since the last issue, we’ve publish a new essay, “Private Equity at the Crossroads,” and the latest edition of “Clippings,” which features the usual eclectic selection of charts and other graphics of interest.

As always, your comments, pushbacks, and ideas about any of the content are welcome.

The pull of consensus

Earnest Sweat, writing for his Groundwork newsletter, begins by reflecting on his early years in equity research — specifically on the need to understand Wall Street consensus before publishing research on a company, which confused him:

Was the goal to be right, or was it to be close enough to everyone else that we wouldn’t stand out?

Now he sees that pull of consensus in the realm of venture capital:

Instead of conviction first and validation later, validation is driving conviction. Investors are circling deals because other investors are circling. Founders signaling who else is in as a primary input into the decision. Rounds that start to take shape only after a certain kind of social proof appears.

A strange version of game theory has taken hold. Not the kind where independent actors make decisions, and the market converges over time, but an inverted version where everyone is trying to anticipate everyone else and move together. The goal is not to be right, but to not be wrong alone.

This is an issue in many parts of the investment ecosystem; as Sweat says, “It is worth asking what kind of outcomes we are quietly optimizing for.”

The repocalypse

“Hedge Funds, Leveraged Finance and Safe Assets: A Look Through the Lenses of the Repocalypse,” a paper by Stefano Sgambati, “examines the deep entanglements between hedge funds, leveraged finance, and the U.S. Treasury market.”

Sgambati recounts examples of “a recurrent pattern of instability in the U.S. Treasury market: one that has become increasingly visible over the past three decades.” He disputes the belief that hedge funds are “opportunistic traders whose failures may harm their investors but pose little systemic risk”:

This view is deeply misleading. Assets under management are a poor proxy for financial power (the ability to shape market outcomes). Hedge funds derive their influence not from the size of their balance sheets in net asset value (NAV) terms, but from their capacity to generate gross notional exposure (GNE) through leverage. By combining repo financing, derivatives, securities lending, and off-balance-sheet synthetic instruments, top hedge funds routinely operate with gross exposures that dwarf their equity capital many times over. It is gross exposure — not net leverage worth or AUM — that determines market impact and, literally, leverage over financial markets.

This means that “treasury market instability is not a narrow technical issue, stemming from exogenous shocks, but a structural feature of the market itself, now entangled with the balance sheets of hedge funds.” And the hedge fund industry’s profitability “has become more and more dependent on the systematic (and automated) exploitation of minuscule spreads across markets through extreme leverage.”

The author provides historical context to frame the issue, including from the “repocalypse” of 2019 and the monetary response it triggered:

This scale and persistence of intervention demand explanation. Markets do not require months of emergency liquidity to recover from minor technical glitches.

The problems that have repeatedly arisen are part of a bigger picture:

The growing instability of the Treasury market, the expansion of hedge fund leverage, and the money market ruptures revealed by the Repocalypse — cannot be understood in isolation. They are embedded in a broader transformation of credit markets: the emergence of what can be described as the leveraged finance complex.

For an entirely different view of the risks that hedge funds present, you can read “Hedge Funds and Financial Stability: A Review of the Evidence” by Ron Alquist (of the Managed Funds Association) and Craig Lewis. Other than the collapse of Long-Term Capital Management (LTCM) in 1998, which they view as “an isolated case,” they find that “hedge funds’ impact on broader financial stability is minimal or absent,” and that the reforms instituted in the wake of LTCM help “market participants accurately price the risks associated with hedge funds” and mitigate potential systematic issues.

Place your bets.

Competitive advantage

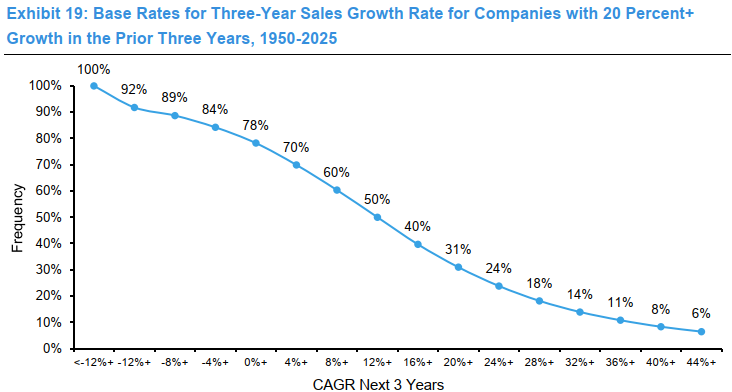

Michael Mauboussin and Dan Callahan have released a report about “the neglected value driver,” that is, the length of the competitive advantage period (CAP) for a firm. They write that “the tools used to quantify CAP are wanting”:

Specifically, market participants generally assess value using multiples of earnings or cash flow that obfuscate the contributions of growth, return on invested capital, opportunity cost, and CAP. A smaller number of practitioners use discounted cash flow models, but they limit the model’s utility by making ungrounded assumptions for the terminal value that often makes up the vast majority of the worth.

Their analysis covers a wide swath of the valuation endeavor, including the seminal developments in company analysis and valuation practice. Toward the end there is a summary of the steps in the valuation process, the exposition of each step having been provided earlier.

Above is one of the charts from the report, demonstrating the importance of knowing the base rates for important variables, in this case regarding sales growth. (If you were able to plot analyst expectations for the same cohort of companies, you would likely see a much different look, demonstrating the need to include base rates in the valuation framework.)

Cogs in an investment machine

Organizational design is a fascination here at The Investment Ecosystem, so a Bloomberg article from David Ramli about FengHe Fund Management caught our eye. It details founding partner Matt Hu’s “unusual approach” to running a hedge fund, especially its decision-making process. Hu makes the decisions; analysts stay mostly within their “monastic cells,” communicating by and large via Slack:

FengHe’s solution is to look for analysts who see this arrangement as a feature, not a bug. Compared with other funds, there’s less need to be an engaging speaker, have an aggressive ‘alpha’ personality or be politically savvy enough to rally internal support. Ultimately, it’s the ideas that count.

There are a few common arrangements of the “cogs in an investment machine;” we hear about the uncommon ones when things have gone well. The question is always whether a given design will work across time in different environments.

Private credit losses

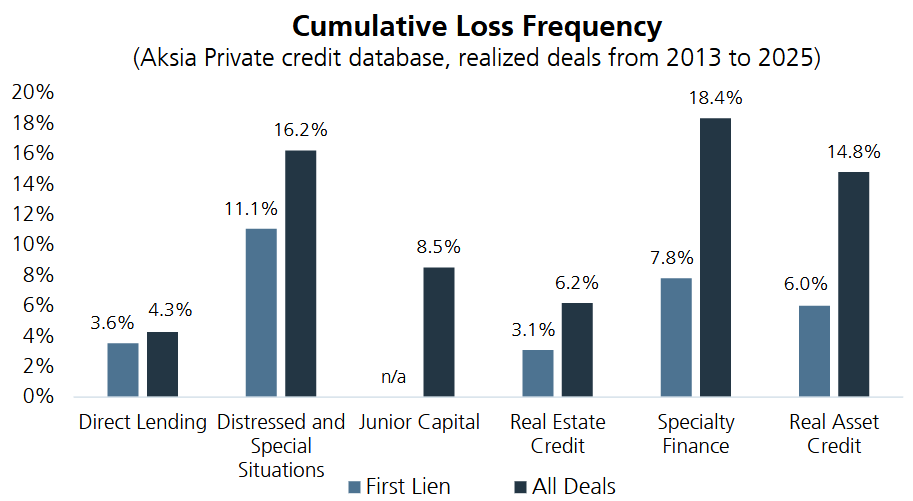

Chris Schelling and Jim Vos of AC Private Markets wrote a report, “Perspectives on Private Credit Risk,” in which they state that “the forward-looking credit loss assumptions being casually tossed around in the financial media appear to have little grounding in fact.” They have included a number of charts and scenario analyses to support their case. Note that the image above shows cumulative losses across thirteen years, not annualized rates of loss.

Other reads

“The Distribution Fallacy — Moats, Mechanisms, and Misreads,” The Terminalist.

What AI provides is the capability to move at speed against moats built in an earlier era, under different competitive conditions, with tooling that has since been superseded.

“BDC and Interval Fund Managers Can Stem Redemption Waves with Transparency, Not Reassurance,” Jeffrey Diehl, Adams Street. This includes a list of metrics that managers should provide to investors.

“Private-Equity Holdings Look Overvalued. Who’s Going to Fix It?” Chris Cumming, Wall Street Journal.

Investors are increasingly worried that private-equity assets are overvalued, and are questioning whether regulators and auditors will hold firms accountable.

“The Impact of AI on SaaS: A Risk Framework for Investors,” Jim Masturzo, Research Affiliates. A view of the “cyclical (within 12 months), secular (one to five years), and super secular (beyond five years)” risks.

“Investor Advocates Ask FASB to Reconsider Guidance on Secondaries,” Michelle Celarier, Institutional Investor.

Because secondaries can be revalued immediately under current rules, the accounting treatment can lift reported performance early — making them attractive tools for evergreen funds that need steady inflows and investor confidence to manage redemptions.

“New kind of boom for US oil patch: Wall Street securitisation,” Stephanie Findlay, Financial Times. A strategy to slice up the cash flows of oil and gas wells “has really exploded;” what are the risks?

“Liquidity as a Product Feature, Not a Market Reality,” Nirasha Senanayake, Enterprising Investor.

The issue is that liquidity is increasingly engineered at the product level, often creating expectations that may not hold under stress.

This is a subtle but important shift — from an asset characteristic to what a product promises.

“The Vanishing Footnote,” Nick Nemeth, Mispriced Assets. Following the trail of private credit exposure to the software firm Medallia, which Thoma Bravo is handing over to creditors (and taking a five billion dollar loss).

“Endowment Radar Study 2025: A Widening Divide,” Tracy Filosa, Cambridge Associates.

The [study] underscores the increasingly strategic role of the endowment as colleges and universities face persistent financial, political, and operational challenges.

“What to do when you’re underperforming,” The Intellectual Edge. Helpful ideas from Anthony Bolton.

Grounds for an opinion

“He who knows only his own side of the case, knows little of that.” — John Stuart Mill.

Flashback: Apple

With Apple turning fifty this month there have been a number of retrospective articles about it. The announcement that Tim Cook will be stepping down as CEO has prompted further reviews, including a New York Times chronicle of the firm’s CEOs since its inception. (There have been several more than the two that most people remember.)

One fascinating item was shared by Sequoia Capital — Don Valentine’s 1977 memo recommending an investment in the company, although “memo” is overstating it a bit. Per word, one of the greatest payoffs of all time.

Mass customization

A very early posting on this site, “Mass Customization and Tactical Asset Allocation,” reviewed a paper from BNP Paribas that proposed an automated approach for investment advisory firms to use a single set of investment views to drive customized allocations across a large number of clients.

While the firm’s view — that “Creating a viable industrial TAA process is thus part of the asset manager’s fiduciary duty towards all its clients” — is debatable, since the old-fashioned way still works:

The paper is a good example of the dance between theory and practice, as well as the push and pull in the industry between customization and industrialization.

Thanks for reading. Many happy total returns.

Published: April 27, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.