Private equity investing has flourished over the last few decades, dramatically changing the institutional investment landscape.

Buyout, venture, growth equity, and distressed all fall under that general umbrella. While each subcategory has it own attributes, historically they have been structurally similar, designed as closed-end funds with a limited life that aren’t offered to the general public.

Over time, other vehicles like secondaries and continuation funds have broadened the opportunity set even further. And there are an increasing number of perpetual or “evergreen” funds that lock up capital for longer periods — to capture greater value in portfolio companies than happens when they ride the typical closed-end fund carousel from manager to manager to manager.

(Recent events have highlighted that investors in those longer-duration funds that have been marketed as “semi-liquid” may have different expectations of liquidity than the structure accommodates.)

The “crossroads” of this posting’s title is applicable to the broad universe of private equity investments, but is specifically aimed at buyout funds, what most people think of as traditional private equity.

The environment

Here are some of the important attributes of the private equity environment today:

~ The latest memo from Howard Marks is titled “What’s Going on in Private Credit?” Among the topics is the relationship between direct investing and private equity, regarding which he writes:

Bottom line: private equity was born and existed through 2021 in an interest rate climate that was supportive of it in the extreme.

Unsurprisingly, things went great.

Marks provides a series of bullet points on the effects of the increase in rates on private equity, including the decline in returns, distributions, and new commitments.

~ There are plenty of books and articles about the downside of the standard private equity fund model and the negative effects on companies and communities from high levels of leverage (often in service of goosing early distributions) and extractive practices.

A 2023 essay on this site asked the question, “As an asset owner, does it matter to you how the money is made, or just that the money is made?” While not all private equity investments should be painted with the same brush, there are clearly negative externalities that result from industry practices. Many asset owners have turned a blind eye to the problems — often in contravention of their stated missions.

To that point, an anonymous author (“a senior partner at a leading international law firm”) wrote a short paper on “The Dark Side of Private Equity.” While stating that “the PE investment model can and should continue to be a substantial vehicle for productive investment,” the author proposes reforms that “would realign PE fund incentives toward resilience and quality without freezing capital formation or growth.”

The private equity industry has thrived in spite of these concerns, but there is an undercurrent of distrust that will likely intensify if inflation persists (keeping interest rates where they are or even higher) and/or if there is a prolonged period of economic weakness. Failed deals expose the weakness of the standard model.

~ To date, the commitment to private equity has remained strong throughout the investment industry. Surveys of asset owners show little inclination to reduce exposure and those with smaller holdings are still ramping up. They are encouraged in that quest not only by the narratives of the providers but by the institutionalization (or industrialization) of private equity — and private capital overall — as the key to investment success.

It is rare to hear a consultant or OCIO or credentialing organization question the orthodoxy of the day. In part that is because working on private capital, with its greater complexity and restricted access, feels like a higher calling. And it feeds much higher fees into the coffers of the organizations and the wallets of the individuals involved.

Inertia is a powerful force. It would take more years of disappointment for the current conformity to reverse, but that should not be dismissed as an impossibility. What would happen if asset owners started stepping back, especially those who have led the parade?

~ The business being what it is, opinions will most likely change only if the current weakness in returns continues for a time.

“Returns” remain a slippery concept for private equity. Internal rates of return (IRRs) don’t fit neatly with the time-weighted returns that are calculated for traditional investments — and IRRs can be manipulated and communicated in ways that are misleading.

Ludovic Phalippou has been especially good at identifying the shortcomings of IRR and its misuse. For example, see a LinkedIn posting from him that pointed out the inanity of the return claims of Apollo. But it’s not just managers who play fast and loose; if you look at the footnotes found in materials from advisors who should be objective about such things, you’ll see that the comparisons made are sometimes apples to oranges — without appropriate context being provided. (Also, there are still those who pass off smoothed volatility as an acceptable measure of “risk.”)

“Democratization”

Retail investors have been clamoring for private equity for some time, wanting to get in on the high returns and low volatility that they have heard institutional asset owners enjoy.

They now are getting their wish, as private equity is marketing standalone vehicles to individuals and has laid the groundwork for a big push in the defined contribution market.

That makes an article by William Clayton and Elisabeth de Fontenay, “Private Equity for All: The Paradoxical Push to Democratize Private Markets,” essential reading. They see “a glaring paradox”:

The democratization narrative has it backwards: retailization erodes private equity’s famed advantages in investor performance and corporate efficiency, while subjecting retail investors to new risks and imposing burdensome new constraints on the private markets.

For individuals, the grass appears greener elsewhere, but:

The suggestion that retail investors have suffered from being limited to publicly-traded securities is not merely misleading, but fanciful. Few investments worldwide have performed better over the last half-century than index funds tracking U.S. public equities — an investment strategy available to all retail investors at near-zero cost.

The authors note that private equity returns have diminished over time as the amount of institutional investment in the industry has swelled; it “delivered its strongest performance when it was still a small, exclusive corner of the market.” And “democratization” will continue that trend and impose other kinds of costs:

Injecting retail investors into private equity directly threatens the very features that make private equity special. Where retail investors tread, regulation, litigation, and public scrutiny inevitably follow.

Yet, the current state of private equity has hastened the move by fund managers to expand the pool of buyers. The authors point out that the new push represents a dramatic shift in the industry’s stated philosophy. As recently as 2023, the American Investment Council (the industry’s lobbying group) “vehemently opposed” changes to private fund regulations that would provide more protection for investors akin to those for registered investment companies:

In pushing back against the proposed regulation, AIC made one thing abundantly clear: the superiority of the private equity ecosystem depends on the sophistication of the investors in the industry.

The authors outline the historical advantages of private equity — selection, governance, freedom from regulation and litigation, and (theoretically at least) the ability to capture an illiquidity premium — and then, one by one, argue how each of those advantages will be eroded in the new era of retail participation.

How will institutional investors deal with the changes?

A poll conducted by the authors (of “69 senior in-house attorneys” for asset owners) gives some indications. First, that the current paucity of distributions has caused a “relative lack of satisfaction with the present-day state of the private funds industry.” The respondents also think that, as a result of the new distribution initiatives, performance will decline and that “retail investors will suffer most.”

While those polled didn’t anticipate a big drop in exposure by asset owners, their responses did reveal “a fascinating possibility”:

The private equity investor universe could become splintered among institutional investors, on one hand, and retail investors, on the other. One mechanism for this would simply be for certain investors to avoid managers that accept any retail capital, which would lead to a divide in the market between two types of managers.

The split

To that point, Dan O’Donnell of Laird Norton Wetherby thinks that private equity investors should avoid those private equity firms that are in the asset gathering business. His report, “Private Equity at 50: Hold Everything,” puts forth an important thesis:

PE’s prolonged success transformed a specialist craft into a $10 trillion dollar industry. Scale doesn’t just make complex systems bigger. It reorganizes them around new priorities. In PE, scale shifts emphasis away from performance-driven carried interest and toward AUM-driven enterprise value.

O’Donnell draws a contrast between managers in “segments within PE where the model is still working the way it was designed” and the firms that dominate the industry and media attention. Yes, “rates went up,” triggering challenges, but that’s “an incomplete explanation” of what is happening:

The deeper cause — the one that headlines don’t address — operates more slowly, more quietly, but unrelentingly: scale.

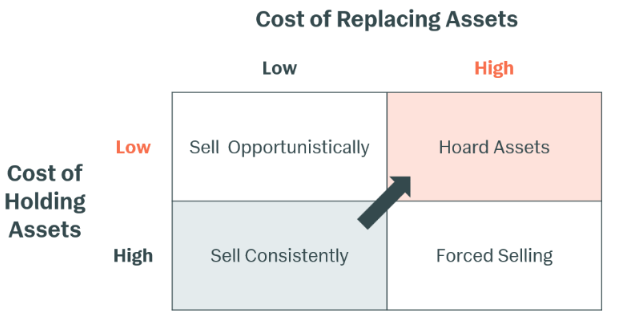

Scale has broken “the iron law of PE,” that “to raise a bigger fund, you had to return capital from prior funds.” Everything stemmed from that; then “scale reorganized the system.” Now we have GP stakes and continuation vehicles and NAV loans — facilities that aid in the hoarding of assets:

The more firms that hoard, the more expensive it becomes for everyone else to replace, which pushes more firms toward hoarding.

The PE flywheel is now spinning in reverse.

How the game has changed:

In the second half of his piece, O’Donnell urges limited partners to find the “specific cohort of firms for whom the original model — buy companies, improve them, sell them, return the proceeds — still holds.” He puts them in three categories: lower middle market, specialists, and emerging managers. His rationale for each is provided, including supportive performance comparisons.

In the second half of his piece, O’Donnell urges limited partners to find the “specific cohort of firms for whom the original model — buy companies, improve them, sell them, return the proceeds — still holds.” He puts them in three categories: lower middle market, specialists, and emerging managers. His rationale for each is provided, including supportive performance comparisons.

What managers will be fit for purpose going forward? Do you want to invest with asset gatherers or investors (or doesn’t it matter)? Where are the incentives aligned? Isn’t it better to have the people in charge close to the investments, with their prospective fortunes relying upon their creative actions rather than by earning fees on assets under management?

In Asset Gatherers, the senior team has a big enterprise to run and competing demands on their time — global fundraising, GP stake negotiations, resource allocation to different vertical or platform teams, sitting on multiple investment committees, managing a 100+ person organization. But at Investor firms, the senior team is spending most of their time investing — originating deals, leading diligence, crafting value creation plans, sitting onboards, and being directly plugged into what’s happening on the ground. Because the investment strategy is the business strategy and vice versa. There’s precious little else to manage.

The crossroads

Private equity is many things. Different strategies, different structures. While this posting mostly deals with classic buyout funds, the ripple effects of these changes will alter the entire private equity ecosystem.

Asset owners and their advisors need to reexamine their beliefs and behaviors to see whether they are based on the private equity that was or the private equity that will be.

It’s common to hear due diligence analysts talk about re-underwriting exposure to a current manager, even though such reviews are often perfunctory when historical returns have been good (especially given the fear of being shut out of future vintages if you skip one).

Now, a re-underwriting of the whole asset class and its subcomponents is in order. Not a casual look rooted in orthodoxy and potentially outdated return expectations, but a deep examination of where the industry is headed and what that means for the size and composition of private equity investments.

Published: April 25, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.