The latest Clippings posting featured the usual mix of great charts, including a most unusual day in the oil market, crashing free cash flows at the hyperscalers, booming secondaries, and many more.

And now, here are some great reads for you.

Endowment model principles

John-Austin Saviano of High Country Advisors wrote a piece called “Swensen Was Right All Along.” Saviano uses his own history and evolution as an investment professional to illuminate the effects that David Swensen had on industry practices.

In the early years, he admitted:

My less-experienced self focused on the Endowment Model as a recipe to be followed. Keep the bar high in your search for PE, venture, hedge funds, etc. and you would create a portfolio which would outperform.

Later, he came to see:

How small the universes were which comprised our understanding of private “asset classes.” So much of what we knew for sure was grounded in relatively limited (in some strategies, incredibly limited) data sets and dominated by a single 10-15 year period.

Getting hung up on the returns that Swensen produced at Yale led industry participants far and wide to see the recipe as a set of asset class ingredients. Instead, it was a different kind of recipe that made the cake (much like the adoption of Moneyball in baseball). Swensen was “playing the game in a fundamentally different way while the rest of the league was still moving on intuition and tradition.”

Now we are in a “massively different environment,” one in which “generating differentiated results today won’t come from artless allocations to private equity, venture, or hedge funds.” Nevertheless, the real endowment model principles are still valid: searching for equity or better uncorrelated returns; using asset managers truly aligned with you (and that offer genuine differentiation); and concentrating on non-consensus undercapitalized ideas.

The endowment model has spread far and wide, but only in the sense of that asset class recipe. Alternatives have become conventional, when the real endowment model means being unconventional and willing to go where the crowds haven’t gathered.

Desirable characteristics

At the end of Saviano’s piece he wrote:

Behaviorally, we need humility, a willingness to accept risk, and curiosity which drives renewal.

In his latest memo, “AI Hurtles Ahead,” Howard Marks opened with a section on understanding AI and recent developments in that area — and ended by revisiting topics from previous writings, namely the possibility of an AI bubble and the potential for negative impacts on society.

In between, he explored the implications for investing from the use of AI, identifying the ways in which the technology could emulate good investor behavior:

It shouldn’t feel fear or greed. It’s hopefully less likely to have an optimistic or pessimistic bias, anchor to preexisting beliefs, or overemphasize the most recent information — unless it picks up those things from the material it’s trained on. It isn’t swayed by the fads that are exciting everyone else, and it isn’t afraid of missing out on the trend others are chasing. In other words, AI possesses a lot of the qualities one needs to be a good investor.

That said, Marks pointed out areas where AI would fall short, including struggling with novel developments for which there aren’t past patterns to draw from and lacking a sense of risk from not having skin in the game. Also, will AI be able to “make subjective decisions regarding qualitative factors and exercise taste and discernment”?

Rayna Lesser Hannaway believes that self-awareness is the key to success in the investment world. A LinkedIn posting from her explains that and includes a visual titled “What the best investors practice consistently.”

Those three perspectives provide pieces of the puzzle. How would you define the most desirable characteristics of an investment professional?

AI Scenarios

In “The AI Disruption: From Doomsday Destruction to Do-Nothing Bots!” Aswath Damodaran considers the AI scenarios that have proliferated of late:

The problem with all of these AI scenarios is that they are rooted in the weakest of responses to uncertainty, which is to either pick a scenario and to describe it in detail, without establishing, at least in qualitative terms, how likely that scenario is, in the first place, or to list out a whole host of scenarios, without making judgments on likelihood of any of them.

That fits with the overwhelming tendency in the investment realm to use point estimates rather than probabilistic distributions when forecasting:

Financial analysts and economics have been slow in adopting and using probabilistic approaches, where point estimates are replaced by distributions, and a single judgment on outcome by a distribution of outcomes.

Damodaran uses his possible/plausible/probable framework to evaluate the potential disruption from AI, focusing on the magnitude and speed of disruption as the key variables.

In closing, he makes an analogy to Pascal’s wager, concluding that you should assume that an AI imitator or bot is coming for your job “even if you don’t believe that it is imminent” — providing a two-by-two matrix of what you believe versus what actually happens (alongside one summarizing Pascal).

Trinary, not binary

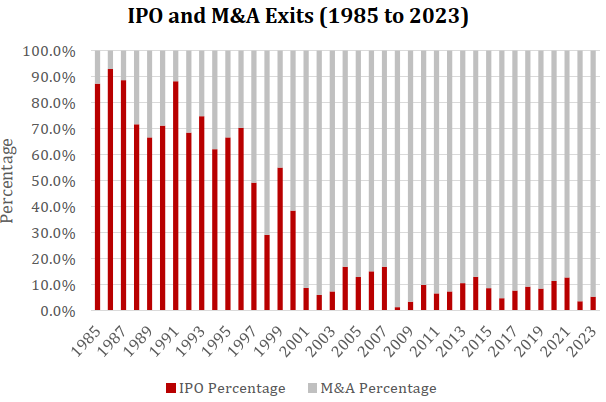

“Public, Private, Acquired,” an article from Alex Platt and Matt Wansley, has a simple premise: that common beliefs about companies choosing to stay private rather than going public are incomplete:

Startups don’t face a binary choice between going public and staying private. They face a trinary choice between going public, staying private, and being acquired. And in the last several decades, startups have increasingly chosen the third option. The decline of public companies is in large part a story of startups choosing acquisitions over listings.

The graphic shows the stark change over time. Many of the companies that might have gone public instead got gobbled up by others.

The Berkshire letter

For the first time since Warren Buffett took over Berkshire Hathaway, some one else wrote the 2025 annual letter — his successor as CEO, Greg Abel.

The first eight pages serve as Abel’s restatement of the firm’s culture, structure, and operational approach. A reader is struck by how unique the total package is among public U.S. corporations. That doesn’t mean that the firm can generate outstanding performance from here — it is a behemoth after all — but you have to admire the elements that Buffett (and Charlie Munger) put together over time.

A Wall Street Journal article by Krystal Hur says that “CEOs Want to Be Like Warren Buffett, Right Down to His Shareholder Letter.” It focuses on the difficulty of writing simply and clearly about business topics — something Buffett was known for — but there’s nothing about the broader being-like-Buffett in it.

If you’re pining for quotes from Buffett, Phil Mohun pulled some passages from annual reports over the last fifty years.

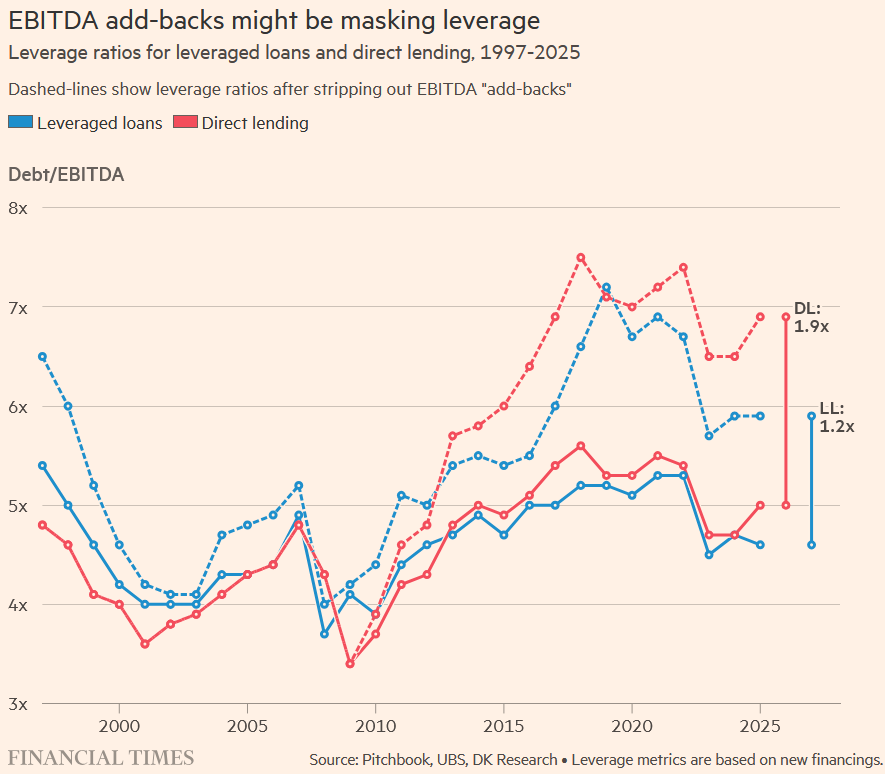

More leverage than advertised

FT Alphaville published a piece by Suzanne Gibbons of Davidson Kempner Capital Management, “Adjusted EBITDA and the masking of leverage.” As shown in the chart:

Over the past decade, these adjustments [to EBITDA] have expanded materially. As credit documentation has weakened, the definition of EBITDA in loan agreements has become looser. Market participants have watched the list of adjustments grow steadily over time, but the data now confirms how far the metric has drifted — so much so that an investment analyst from a decade ago might struggle to recognise it.

In leveraged loans, EBITDA add-backs now reduce reported leverage at issuance by roughly 1.2 turns of leverage. In direct lending, the impact is even larger — about 1.9 turns. In both cases the gap is roughly double what it was in 2015.

Other reads

“World (Soft)War II,” Arctos.

AI creates substitution threats for validation and certainty, while simultaneously raising the marginal costs of computing. This is Software Deflation + Compute Inflation that threatens gross margins.

“Insurance Weapons of Mass Deception,” Rod Dubitsky. Is reinsurance “a massive and opaque means of credit risk laundering” that “warrants immediate attention by market participants and regulators”?

“The SPEC Test,” Milos Maricic.

The problem is not that quantitative managers are dishonest. Most are not. The problem is that the standard framework for evaluating them creates systematic blind spots.

“The Created Value Attribution Handbook,” Paul Viscio and George Pushner, Kroll. A guide to the firm’s CVA Framework, which was created to correct the “fatal flaws” of the traditional value bridge.

“The Gap Between Wanting AI and Being Ready for It Is Wider Than You Think,” Angelo Calvello, Institutional Investor.

The gap is more consequential than most are willing to admit. The real obstacle is not the technology. It is the institutional structure of asset owners themselves.

“Nasdaq’s Shame,” Keubiko’s Musings. Subtitle: “How to rig an index to appease a billionaire.”

“How to Actually Align Investments with Your Foundation’s Mission (Without Breaking the Budget),” Kris Shergold, LinkedIn.

Most foundations struggle to translate their specific charitable purpose into an operational mission-aligned investment framework.

“The tyranny of targets,” Tim Harford. Which metrics are “scaffolding for productivity” and which are “a cage for us poor players”?

“Superstar CEOs and Super Acquisitions,” Weisu Yu and Craig Wilson, SSRN.

These results reveal that the social status a CEO gains from winning a best CEO award plays an important role in explaining their firm’s merger and acquisition decisions. Our findings provide a potential channel to explain why firms with award-winning CEOs tend to decline in value in the years following the award.

Some investing talk too

“Three-fourths of philosophy and literature is the talk of people trying to convince themselves that they really like the cage they were tricked into entering.” — Gary Snyder.

Flashback: Bell Labs

According to Wikipedia:

Bell Labs and its researchers have been credited with the development of radio astronomy, the transistor, the laser, the photovoltaic cell, the charge-coupled device (CCD), information theory, the Unix operating system, and the programming languages B, C, C++, S, SNOBOL, AWK, AMPL, and others, throughout the 20th century. Eleven Nobel Prizes and five Turing Awards have been awarded for work completed at Bell Laboratories.

The New York Times recently highlighted some of those developments, which have shaped our modern world. For more on Bell Labs, check out a book by Jon Gertner, The Idea Factory: Bell Labs and the Great Age of American Innovation.

Understanding your organization

A 2022 posting, “Network Analytics in Investment Organizations,” explored the structure of organizations and how information moves within them. This is how it ended:

What you would most like to know is how ideas flow through the organization — who originates the best ones, who propagates them, who uses them to great effect, and who kills them off. And you’d want to understand what functional needs are not being met and where there are skill shortfalls that should be addressed through hiring or training or the restructuring of roles. Insights like those are mostly the province of observation and intuition now; network analytics may provide more concrete evidence to support design decisions that will produce the investment performance of the future. Organizations should be examining the possibilities as part of their research and development efforts.

Thanks for reading. Many happy total returns.

Published: March 16, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.