This month, AI has turned into the boogeyman.

Almost every day, equity investors are taking the axe to an industry because of fears of competition from AI. It started with software, then insurance brokers, then wealth advisors, then real estate services, then trucking/logistics.

The latest “clippings” posting included a chart on the software effects, plus a Tesla triptych and a bunch of other cool visuals. (Subscribe here if you don’t want to miss these quick, informative, and fun dispatches.)

Meanwhile, there are important questions afoot.

Evergreen funds

In January, Hilary Wiek of PitchBook published a report, “Evergreen Funds: We Have Questions.” She used the common structure of words beginning with “P” to outline an approach to evaluating funds, in her case seven Ps in all: people, philosophy, process, portfolio construction, performance, pricing, and potpourri. (The last, unusual one consisting of investor concentration and suitability.) As advertised, each section offers important questions for prospective investors.

On the other side of the table, managers — eager to cash in on the retail demand for private assets — are actively promoting evergreens. Two examples: KKR offered “5 Questions to Ask Managers about Evergreen Private Equity” and Ares published “Evaluating Evergreens: Navigating the Subtleties of Private Markets Fund Structures,” much of which compares evergreen to drawdown structures.

To Wiek’s seven Ps, Tim McGlinn of TheAltView adds another uncommon one: “ponzicity.” He uses the Ares Private Markets Fund to show how “NAV-Squeezing” — buying secondaries at a discount and immediately marking them at net asset value — can juice the returns of evergreen funds.

While being careful not to call “any evergreen secondary fund an actual Ponzi scheme,” McGlinn thinks it will feel like that to some investors when the virtuous markup cycle runs out of gas.

Private credit

In response to what it sees as a “misguided narrative” about private credit (conflating issues in the broadly syndicated loan market with other forms of lending), Cliffwater issued a report called “Back to Basics: The Five Ws of Private Debt.” The five questions to ask: “Who is borrowing? What supports repayment? When does capital return? Where does the lender sit in the capital structure? Why does the borrower need the capital?”

The Five Ws describe the shape of risk. The final question is how that risk is managed.

In response, Rachel Volynsky wrote a posting for Leyla Kunimoto’s Accredited Investor Insights, “Five Q(uestion)s for Cliffwater’s Five Ws.” While generally complimentary about Cliffwater’s work, Volynsky has qualms, best summed up in this paragraph:

The Five Ws framework explains how private debt is supposed to work. What it does not ask is how it behaves when it stops working as advertised.

What will happen “when correlations rise, exits stall, amendments proliferate, and liquidity becomes scarce?” As is always the case regarding newer strategies, “we have heard plenty of reassurance, but most of it comes from within the asset management ecosystem itself.” Will the early evidence stand up in less benign market environments?

AI

Will the promise of investments in AI pay off? More specifically, will the forecasts of companies at the heart of AI development come to fruition?

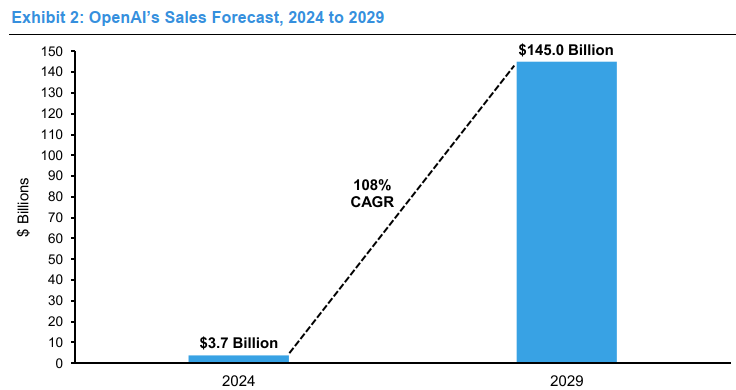

That’s the question behind “Bayes and Base Rates,” a short article from Michael Mauboussin and Dan Callahan. It first looks at OpenAI’s 2029 revenue forecast, as shown here, that calls for a compound growth rate of 108%. In looking for comparables, the authors find that “no public company [with similar revenues] has grown this fast for five years in the last three-quarters of a century.” (Also of interest, the rate of stock-based compensation at OpenAI is seven times higher than any large technology companies prior to going public.)

The second example provided is in regards to Oracle’s cloud infrastructure business, where the conclusion is the same — there’s no precedent for the kind of revenue growth expected.

Unfortunately: “The math of Bayes’ Theorem does not work if the initial belief is based on an outcome with a probability of zero,” which is what the base rates for these expectations are. Plus, the success rates of large projects (being on time and on budget, with benefits as expected) are close to zero too. A highly speculative set of assumptions out there.

For more on AI investment possibilities, see the Sparkline investor letter from Kai Wu. It’s full of interesting charts and perspectives, including:

Lofty AI infrastructure stock valuations price in rapid growth in near-term AI demand. Unfortunately, precisely forecasting the speed of adoption is nearly impossible. That said, we believe risk skews to the downside, as these stocks could see significant losses from multiple compression if demand does not materialize as quickly as investors expect.

Princeton

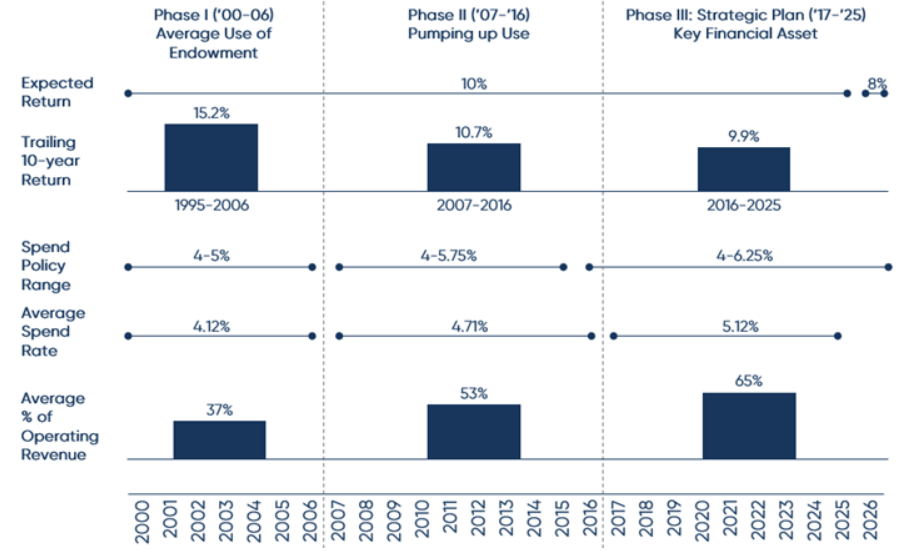

In a surprise move, Princeton slashed the expected return on its endowment from 10.2% to 8%. Anne Duggan of TIFF covers the “highs” of the endowment relative to its peers: high endowment dependency, high sensitivity to changes in endowment value, a high spend rate, and a high expected return. Given sloppy returns on private assets lately and other pressures on universities, observers have been wondering how investment policies might change. Princeton realized that lofty investment expectations had led to unsustainable practices and is downshifting its projections, as spending is being cut across the university.

The hidden organization

When doing due diligence, accepting the narrative as it is doesn’t lead to discovery or understanding. One point in the structure model of the Advanced Due Diligence and Manager Selection course is that an organization chart doesn’t tell you as much as you think it does. There is always a hidden organization based on who really matters without regard to where (or whether) they appear in an organization chart. (And, yes, the investment process in the pitch book may not be that great of a representation either.)

That all came to mind upon reading this wonderful paragraph on a much different topic (the “SaaSpocalypse”) in a piece by Chris Walker:

You learn that the org chart is a polite fiction. The real map of influence and trust is invisible, legible only through presence, and it determines which initiatives actually ship and which ones die in committee. You learn which tools people rely on versus which ones they dutifully log into for compliance. You observe the workarounds, the informal protocols, the tribal knowledge passed between colleagues. None of this is written down. Very little of it can be written down.

Family offices

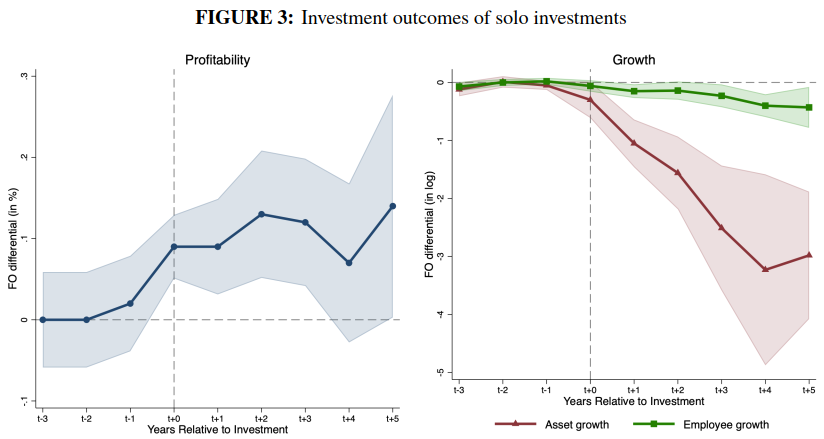

In the paper “The Family Office Effect: How Ownership Style Shapes Firm Strategy,” Jeroen Verbouw, et al. examine how the ownership preferences of family offices differ from those of typical institutional buyers:

Our findings demonstrate that FOs, driven by their unique ownership style, pursue more distinct investment strategies, hold investments for longer, and foster a strategic orientation that emphasizes sustainable profitability over aggressive growth.

R&D alpha

A paper by Abhishek Sehgal includes the conclusion that a measure of R&D intensity “offers a complementary return source for factor-based investors” (while choosing not to ascribe causality to the “mispricing of intangible assets” or “risk compensation for innovation exposure”).

In addition to the research itself, the paper is notable for its clarity in comparison to most academic research. Explanatory sidebars throughout describe key terminology, “what we do vs. what we do not claim,” limitations, how to interpret the results of tests, etc. A model to follow (for investment communications as well as research papers).

Other reads

“Beyond the Hype: How AI Is Changing Equity Investing ,” Weichen Ding, bfinance.

The right question for investors is no longer “Are you using AI?” but “How is AI changing your process — and can you prove it?”

“The Pain of Starting Work on Another GP,” Anthony Hagan, Freedomization. Regarding “the psychological anguish many investment analysts experience before they begin deep work on a manager they have never analyzed before.”

“NBIM quantifies the portfolio threat of economic fragmentation,” Darcy Song, Top1000Funds.

A risk assessment of Norges Bank Investment Management’s portfolio reveals global economic fragmentation as the most threatening risk scenario analysed, with the fund’s latest stress test highlighting that alienated trade blocs, aggressive tariffs and restrictions on foreign investments could erase more than a third of the fund’s value.

“How the Merrill Lynch deal made Bloomberg,” Rupak Ghose. The history of that “David and Goliath partnership” of yore might provide lessons for potential hookups between financial firms and upstart data vendors today.

“Super Bowl Ads as a Bubble Warning,” Owen Lamont, Acadian.

If the wave of AI ads at the Super Bowl is followed by a wave of AI IPOs later this year, watch out.

“The Second Coming,” Rajiv Sethi, Imperfect Information. Now available: A prediction market contract on whether Jesus will return this year — and a derivative bet for the real players out there.

“The Data Delusion in Venture,” Rohit Yadav, All Things VC.

Stop underwriting stories about data. Underwrite systems.

“Here’s Fidelity Contrafund’s Will Danoff’s Secret Sauce,” Robby Greengold, Morningstar. Insights on Danoff’s long and successful tenure.

“Come Clean,” Jeffrey Ptak, Basis Pointing.

Absent some better explanation, it sure seems like the manager misrepresented the economic substance of XOVR’s participation in SpaceX equity.

It can go on and on

“It’s amazing how many times you can take 20% out of these things.” (Overheard at a common-area Quotron during a 1980s pullback in small technology stocks.)

Flashback: The Blodget report

A December newsletter from Spencer Jakab of the Wall Street Journal marked the day 27 years earlier when Henry Blodget, “a young analyst at second-tier brokerage firm CIBC Oppenheimer,” raised his target on Amazon from $150 to $400.

In response, Amazon soared and then crashed hard, ultimately providing an opportunity for anyone brave enough or foresighted enough to take a shot at the beaten-down stock.

Those were the star analyst years, as recounted in a 2022 posting on this site. These days, the hype often comes from CEOs rather than analysts — or from influencers leading a mob of individual investors. In any case, if we do get a collapse in today’s highfliers, there will be a few choice long-term bargains on offer.

Cliques and claques

Another 2022 posting offered thoughts on this theme:

Cliques and claques are foundational elements of the practice, if not the theory, of investing, which is dominated by social proof and pressure. The investment textbooks don’t get into that, but the sociology and anthropology ones do.

Thanks for reading. Many happy total returns.

Published: February 16, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.