If you are a new reader of this publication: The goal of the Fortnightly is to provide a curated set of reads from across the investment world that are moving (or will move) institutional investment activity. In addition, occasional original essays provide in-depth ideas for the kind of continuous improvement that’s necessary for long-term success. To receive each posting in your email, subscribe here.

Asset owner governance

Redouane Elkamhi and Jacky Lee published a paper about “The Benchmarking Prisoner’s Dilemma.” They argue that the common approach of having a board (or investment committee) approve a top-down benchmark for an asset pool and the benchmarks for individual parts of it, results in a “double-agency problem” in which:

The organization settles into a “safe but constrained” equilibrium — careers are protected and optics are preserved, but genuine value creation is limited.

Instead, the authors favor a situation where the responsibility for benchmarking of asset categories is delegated to the CIO and CEO, thinking that it leads to improved total-portfolio efficiency; the decoupling of benchmarks from investment decisions; higher-quality alpha; better talent alignment; more honest reporting; and higher risk-adjusted returns.

While all of that sounds great, it’s not clear that the game theory involved would actually translate in practice. Especially questionable are the assumptions about the incentives for and behaviors of those involved and the cultural norms embedded in individual organizations and the asset owner community in general.

Howard Marks also addressed asset owner governance in his latest memo, “A Look Under the Hood,” which offers his impressions of a meeting with a state pension fund’s board, senior staff, and investment consultant. His overview covers a wide range of concerns for asset owner fiduciaries, reflected in the results of a survey of the fund’s decision makers, and gives his opinions on the relevant topics. The memo could be useful as the basis for a discussion by an investment committee as part of a periodic review of beliefs to identify areas of agreement and contention.

One set of important governance practices involves the reporting of decisions, positions, and results to fiduciaries, beneficiaries, and other stakeholders. Government pension plans often make much of that information public, while many other asset owners don’t.

A lawsuit filed in July by Rich Wiggins against the Iowa Public Employees’ Retirement System (IPERS) has brought some of those issues to the fore. Tim McGlinn at TheAltView has dug through the IPERS information and published three postings questioning its reporting of 1) investment costs and benchmarking analyses (as prepared by an outsourced provider); 2) benchmarking practices for individual asset classes; and 3) the calculation of (and the striking visual presentation of) tracking error as “risk.”

Regardless of the future path taken by that litigation, asset owners ought to consider their own reporting standards carefully. There is a long chain of (internal and external) investment agents in the investment world and many opportunities to present information in favorable ways.

Sell-side analysts

Because elements of their work can be tracked, the performance of sell-side equity analysts has been extensively studied over time. Here are three pieces of research from the last few months that address different angles of interest:

“Empty Vessels Make the Most Noise: Analyst Self-Promotion Behavior and Market Outcomes,” Chun Liu and Shunzhi Pang. In our age of social promotion, judgments about analysts are shaped by “both standardized professional metrics and carefully constructed personal narratives.” Career opportunities are shaped in different ways than they used to be.

“Clinging to Beliefs in Financial Markets: Solving the Post-Earnings Announcement Drift Puzzle,” Odhrain McCarthy. That “drift,” the playing of which is a feature of many investment strategies, “is not an unconditional anomaly but largely a conditional one — it mostly occurs when quarterly earnings contradict the prevailing analyst recommendation.”

“Sell-Side Analysts’ Rating Systems,” Leonardo Madureira, et al. The ratings systems used by brokerage firms and how they are mapped to consensus ratings featured on data platforms and websites “have implications for the determination of whether analysts tend to herd or be bold and on the reactions of investors to the issuance of stock recommendations.” A fascinating example of an overlooked set of practices that affects investor behavior and the academic analysis of analyst beliefs.

The AI capex boom

Several previous editions of the Fortnightly have included links to material about what seems like the biggest financial story of the day (but one which really only shot to the top of investors’ minds in the last few months). Here’s another chapter.

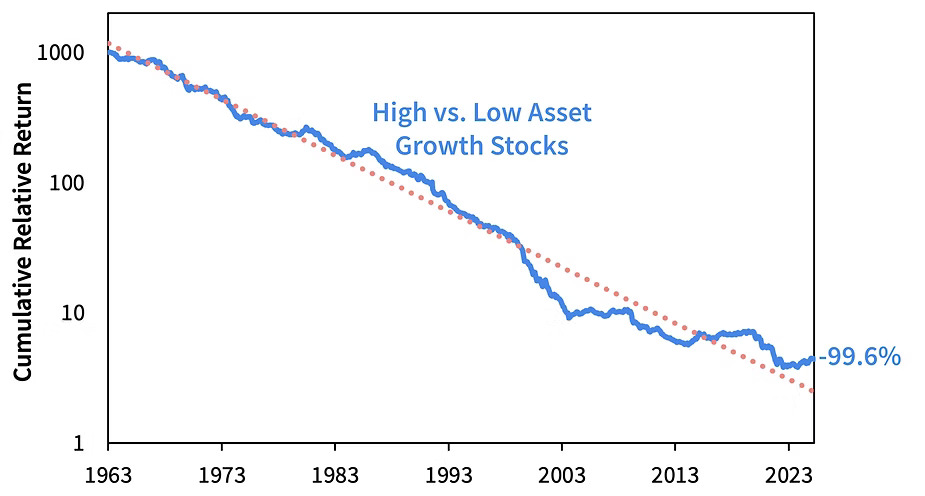

Kai Wu of Sparkline Capital published “Surviving the AI Capex Boom,” a report in which (as is typical of the firm’s output) the topic is examined via a large number of helpful charts and comments.

Setting up the main theme in dramatic fashion is the above image, the title of which is “Asset-Heavy Firms Underperform.” According to the footnote, it shows “the relative return of top vs. bottom quintile stocks based on trailing 1-year capex to revenue. Equally-weighted and rebalanced monthly.”

Today’s market leaders are morphing from asset-light plays to capital-intensive ones, with a sudden and significant rise in capital expenditures:

![]()

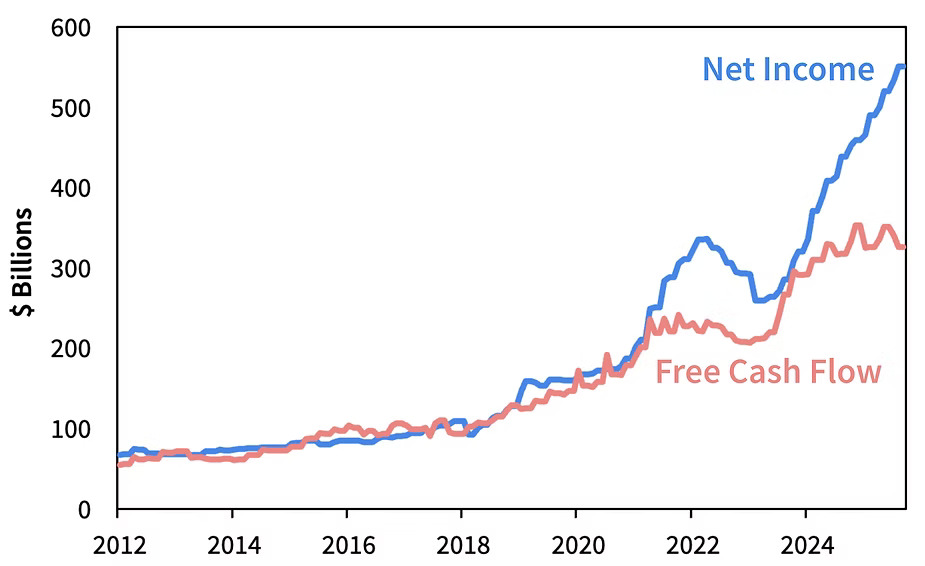

Leading to a divergence in net income and free cash flow:

There is much more covered in the report, including “hidden AI winners,” comparisons to previous hype cycles, the “AI prisoner’s dilemma,” and:

There is much more covered in the report, including “hidden AI winners,” comparisons to previous hype cycles, the “AI prisoner’s dilemma,” and:

Although the Magnificent 7 still have sterling balance sheets, they are increasingly entangled with less financially-sound firms like OpenAI, CoreWeave, and Oracle. In addition, with free cash flows dwindling, they are starting to turn to debt financing.

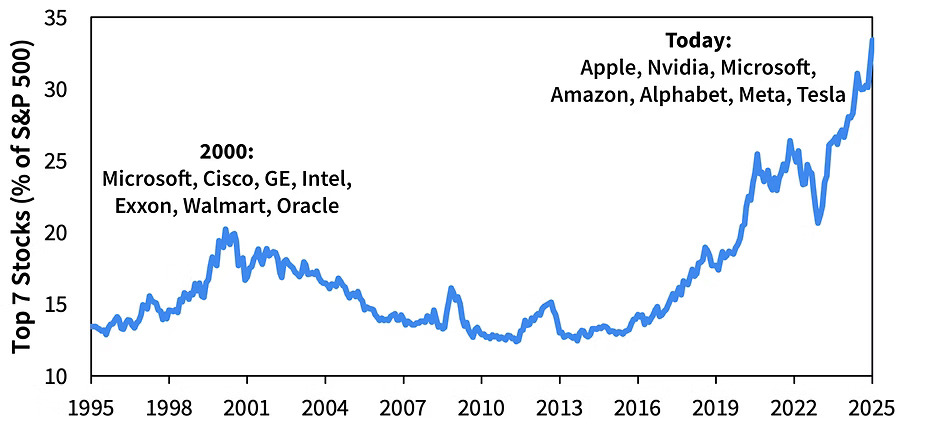

The stakes for the market are high, since it “is increasingly driven by a single theme”:

General partner positioning

Anthony Hagan of Freedomization writes regularly and well about the relationships between general partners and limited partners, mostly from the latter’s point of view. However, three recent pieces have focused on choices made by GPs regarding how to position themselves in those relationships.

~ Which will it be, putting forth an aura of transparency or mystique?

~ Six topics about which GPs might take advantage of strategic ambiguity.

~ Doing reverse due diligence (to identify LPs you’re better off doing without).

Margin math

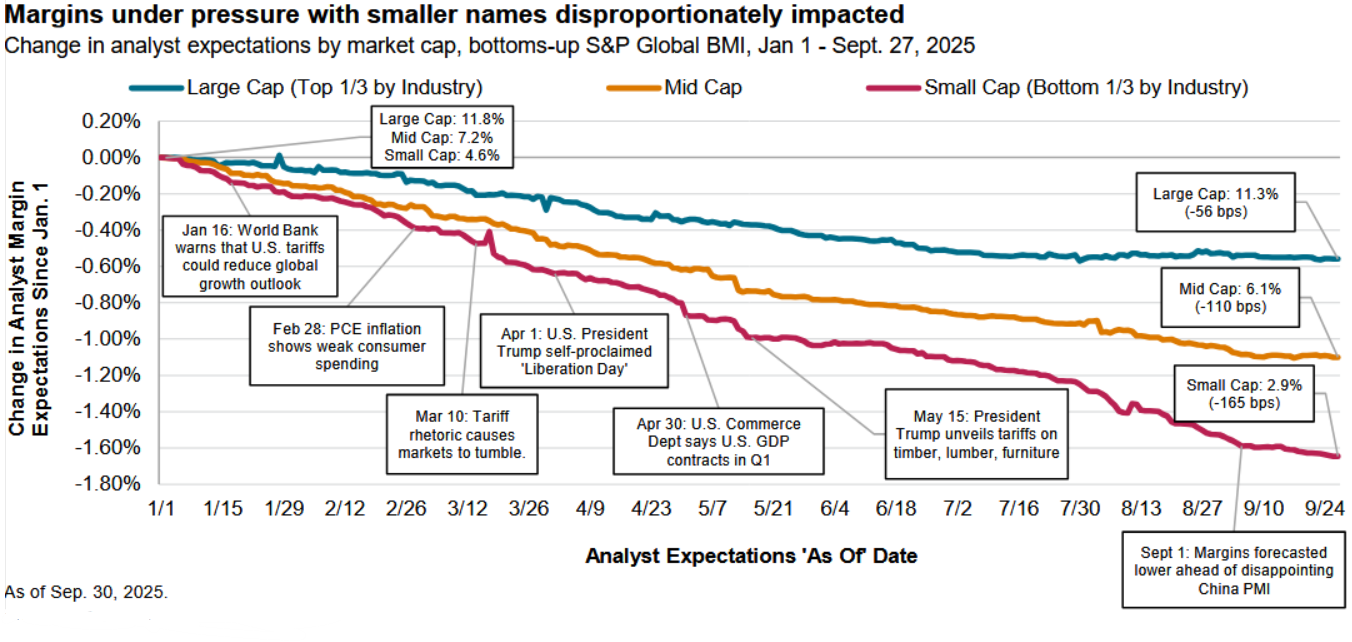

According to an S&P report, the forecasted sales growth for global companies is outpacing that for earnings because of pressure on margins due to “supply chain contagion,” related to increased tariffs and other issues. As you might expect — and this graphic shows — the effects are more pronounced for smaller companies.

Other reads

“How to Use the Sharpe Ratio,” Marcos Lopez de Prado, et al., SSRN.

The Sharpe ratio remains the most widely used measure of investment efficiency, yet its naive application leads to misleading inference and financial losses.

“What’s up with private credit ratings?” Toby Nangle, Financial Times. Insurance industry regulations provide a window into credit ratings issued on direct loans, prompting questions.

“The Cockroaches in Private Credit,” Covenant Lite.

BDCs and other private credit lenders exposed to healthcare roll-ups are already feeling the pressure. While healthcare platforms make up a small share of assets, they make up a disproportionate share of problem loans.

“The Trading Floor – Cathedrals of Capitalism,” Rupak Ghose. A brief history of and differences among trading floors at different kinds of firms. (See also a previous Investment Ecosystem posting on the dynamics of an investment bank trading floor.)

“The Challenge of Diversification,” Chris Satterthwaite, Verdad.

Asset class diversification works well in theory, but for the return-maximizing investor the reality has been that benefitting from diversification has not been easy. The sources of diversifying returns have been too fickle.

“Breathe Through Your Mouth,” Jeffrey Ptak, Basis Pointing. Estimating the underlying expenses of a popular leveraged ETF.

“The New Face of Private Markets in Your 401(k),” Hilary Wiek, PitchBook.

Income-producing private assets are the best fit for offerings that allow frequent contributions and periodic withdrawals, which may disappoint those expecting this movement to provide access to more high-octane PE or VC.

“Strategy shares will go up if bitcoin goes up and won’t if it doesn’t: Citi,” Bryce Elder, Financial Times. Parsing a research report on the preeminent bitcoin treasury company.

Cognitive diversity

“Surround yourself with people who are thoughtful in ways you are not, because they see what you can’t.” — Shane Parrish.

Flashback: Venture capital valuations

Released as a working paper in 2017 and subsequently published in the Journal of Financial Economics, “Squaring Venture Capital Valuations with Reality” by Will Gornall and Ilya Strebulaev laid bare a common industry practice that doesn’t stand up to scrutiny. Namely, using the stated valuation of the most recent round of venture capital as the measure of its real value:

Many finance professionals, both inside and outside of the VC industry, think of the post–money valuation as a fair valuation of the company. Both mutual funds and VC funds typically mark up the value of their investments to the price of the most recent funding round.

Written during a time when it became popular to name and count “unicorns” — those venture firms having a valuation above a billion dollars — the authors poked holes in the game:

Equating post–money valuation with fair valuation overlooks the option-like nature of convertible preferred shares and overstates the value of common equity, previously issued preferred shares, and the entire company.

Subsequent work by the authors and others have supported the conclusion that the stated value of venture companies is too high; most analyses have put the overvaluation in the neighborhood of fifty percent. Yet we still see inaccurate values of firms cited in the press and in investment reports — and (most importantly) in the accounts of investors and employees — at levels much higher than they should be.

More on sell-side analysts

A 2023 posting, “Social Forces and Sell-Side Analysts,” was published on this site as a part of an extensive series, “Anthropology and Investment Organizations,” which looked at cultural patterns in different parts of the investment ecosystem.

Social forces play a meaningful part in investment decision making despite protestations to the contrary, and the role of the sell-side analyst is particularly exposed to those pressures:

“Webs of relationships” characterize the environments within which analysts operate, including those with the companies that they analyze, the buy-side investors who tap them for information (and “concierge services”), others in the firms at which they work, and their analyst counterparts at other firms, with whom they compete.

Thanks for reading. Many happy total returns.

Published: November 3, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.