If you don’t already receive these postings via email, you may sign up here. (And don’t forget to share with your co-workers and friends.)

On to the readings.

Bitcoin treasury

Michael Saylor of Strategy (née MicroStrategy) is the godfather of the corporate bitcoin treasury movement. He has bet his company on the digital currency (if “currency” is an appropriate description of bitcoin).

In the Financial Times, Craig Coben writes that, since the premium afforded by investors to Strategy for its bitcoin holdings has been shrinking, “it feels like the magic is fading.” But other companies are rushing to adopt Strategy’s strategy.

As chronicled in a series of Be Water postings, we’ve seen similar developments before, especially during the 1920s bubble in investment trusts and the crash in their values that followed. And you can hear an echo of the CDO-squareds of the financial crisis, with a new “Strategy-squared” plan to use a “digital-asset treasury company to invest in other digital-asset treasury companies.”

Proponents are thinking big. For example, Zac Townsend of Meanwhile, “a BTC-denominated life insurer and asset manager building long-term financial infrastructure,” wrote an opinion piece for Institutional Investor, which began:

The conventional wisdom on Bitcoin treasury companies that make holding BTC their primary business is that they’re just clever public-market arbitrages. They’re levered bets on digital gold wrapped in corporate paper. But to believe that take is to miss the forest for the trees. These firms aren’t short-term trades. They’re the seed stage of the world’s next generation of endowments.

The institutional world has been inching toward the inclusion of crypto investments in the standard toolkit. Banks and advisory firms that swore they wouldn’t offer crypto-related products are now doing so. And investment credentialling organizations have responded too — see one 2023 example, “Valuation of Cryptoassets: A Guide for Investment Professionals,” from CFA Institute.

Every supposed new era in investing promises a bright future of expanded possibilities. Sometimes it comes true, sometimes not. Making choices as to what to believe when in the midst of the excitement is the hardest part.

The value of creativity

In “The Value of a Creative Hire in Finance,” Stacy Havener offers a scenario:

Your new creative hire walks into a meeting. They’re the only one in the room without a CFA designation. They can’t rattle off the Sharpe ratio from memory. If you asked them to explain a basis point, they might pause.

At this point, you might say, “Why would you hire someone that unprepared?” Except they aren’t really unprepared, you just think they are because they don’t know what you know or do what you do.

They bring different skills to the table — ones in short supply at many organizations. Havener does a good job of describing what it takes to connect with (and stay connected with) prospects and clients in ways that are outside of the typical playbook for many investment professionals.

But the need for creative types is not limited to the marketing function. Having everyone of one type on an investment team impedes good decision making and results in a lack of continuous improvement in methods. You won’t end up with needed creativity in the investment process if you don’t have some at-least-marginally-creative people involved.

Chenmark invests in small businesses, but the topic of its most recent weekly piece fits here and is applicable to all of us, no matter where we are in the investment ecosystem. We all should want to “read the air,” yet the ability to do so is generally undervalued in our industry.

Paying up for safety

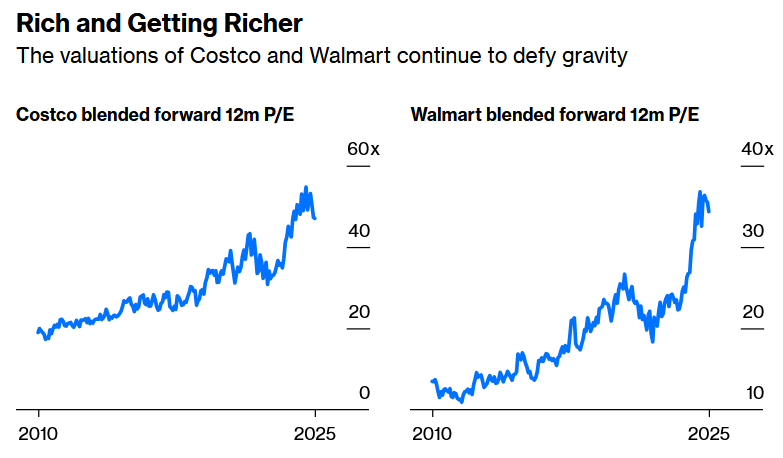

Recollections of the late-nineties stock market are usually focused on technology companies, especially the dot-coms which crashed thereafter. But all manner of stocks reached multiples substantially above their norms, including some “big and safe” ones. Coca-Cola traded around fifty times earnings before that ratio fell steadily over the ensuing years, finally bottoming in the low teens during the financial crisis.

A Bloomberg column by Jonathan Levin points out a similar circumstance today: “Forget Nvidia. Costco and Walmart Look Scarier”:

As the story goes, Costco and Walmart are all-weather stocks. Their reputation for good value means they profit in good times and snap up market share when the economy goes south.

And, as you can see from the charts (and from history), how those profits are priced by investors can vary significantly over time. “Reasonable” is a movable standard.

AI pitching and AI washing

Angelo Calvello, a veteran of marketing AI investment capabilities, offers recommendations on “how to pitch an AI strategy.” His four lessons provide a good framework for investment managers trying to figure out how to position themselves in this new world. The last of the lessons — “Explainability Is Non-Negotiable” — deals directly with one of the core questions that managers have:

Allocators won’t invest in AI strategies where the model developer is unable to explain the model decisions (despite the irony that human decision-making is equally opaque).

For those on the other side of the table, Joseph Simonian published a report for CFA Institute, “AI Washing: Signs, Symptoms, and Suggested Solutions for Investment Stakeholders.” He covers the motivations behind AI washing for managers and the dilemmas they face promoting changes in their process related to AI. The report ends with a list of “the most pertinent questions for asset owners and prospective clients.”

Active and passive

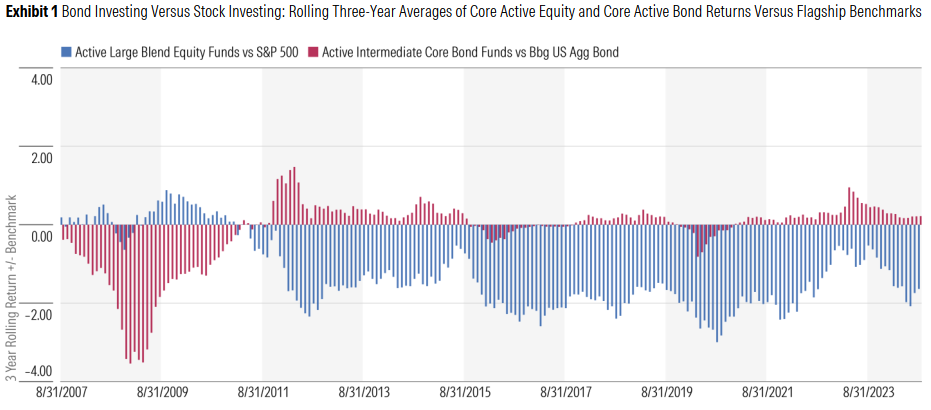

Eric Jacobson of Morningstar wrote a report entitled “The Bond Market as Fertile Ground for Active Management.” It “argues that the bond market’s structure and complexity create substantial inefficiencies so fundamental and inherent that eliminating them anytime soon would be a mammoth and improbable task.”

This chart, one of many in the report, shows the pervasive underperformance of equity funds over the last fifteen years and the frequent, if modest, outperformance by bond funds.

Elsewhere, writing for the Alpha Architect website, Larry Swedroe examines the “classification paradox” for equity vehicles, which he believes “creates more confusion than clarity”:

Rather than getting caught up in arbitrary active/passive labels, investors should focus on more meaningful distinctions.

Down on the farm

A Wall Street Journal article begins:

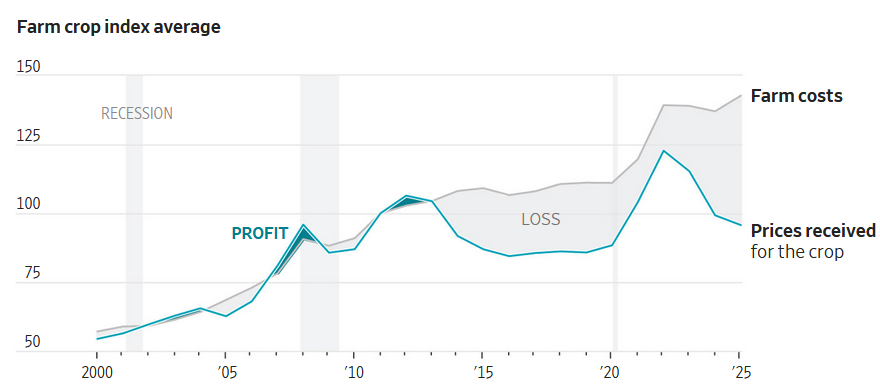

American farmers are good at producing two crops: corn and soybeans. Too good, actually.

Advancements in seeds, pesticides, and equipment have led to bumper crops. Plus, farmers have gone from planting “fencepost to fencepost” in the old days to increasing the acres planted: fenceposts are rare now (allowing for a bit more land to plant), tiling has drained most of the wet spots, and irrigation is used in dry areas. Plus, a warming climate has made it possible to plant in northern regions where it wasn’t practical before.

The cost of inputs has increased significantly — and demand and market prices have lagged, resulting in the decade-long loss profile shown in the chart. Tariffs have made the demand situation even more dicey.

Surprisingly, land prices have increased steadily over the years, although a little softness is starting to show up. As the article indicates, the Trump administration is considering a bailout for farmers; given the way large producers now dominate the business, that may not provide the help to those who need it the most.

Other reads

“An Old-School Hedge Fund Strategy Reboots Outside Big Pod Shops,” Liza Tetley and Nishant Kumar, Bloomberg.

Making money out of event-driven strategies requires conviction and a lot of patience. It’s at odds with the rules hard-coded into the DNA of most pod shops that typically set tight loss limits to achieve the steady returns their investors demand.

“Bull Markets,” Ian Cassel, MicroCapClub. Polar opposite challenges and behaviors in bull and bear markets.

“Private Markets for the People? Or Just More People for Private Markets?” Ludovic Phalippou, SSRN.

Giving individual investors exposure to a high-fee, opaque, conflict-ridden asset class — marketed using gameable metrics and de facto fictional track records — is not governance for the people. It’s governance at their expense.

“Democratizing Private Markets: Private Equity Performance of Individual Investors,” Cynthia Balloch, et al., SSRN.

We document that individual investors [in private equity] achieve performance comparable to institutional benchmarks and outperform public markets on aggregate. However, this overall success masks important heterogeneity, with a significant wealth gradient where the most affluent investors substantially outperform the least affluent.

“Spotting Accounting Shenanigans with AI,” Matt Robinson, AI Street. Can machines do a better job of spotting problems than analysts, who are anchored by management guidance?

”Carpet Guys,” Phil Bak, BakStack.

There is only so much we can learn from our computer desk. There is only so much we can understand about the world through screens.

Confidence

“Too little confidence, and you’re unable to act; too much confidence, and you’re unable to hear.” — John Maeda (via Jim O’Shaughnessy).

Academic research

Most Fortnightly editions, including this one, reference academic research sources. A 2022 posting, “How to Use Academic Research,” covers some basics and then provides three examples of papers and questions that could be asked in response to them. The topics considered are pairs trading, fund size, and selecting managers.

Thanks for reading. Many happy total returns.

Published: September 8, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.