The first Investment Ecosystem essay since March is “Cultural Inflections and Disruptions at Asset Management Firms.” The posting looks at the hard-to-discern-but-ultimately-critical element of success:

A deterioration in culture is often overlooked by leaders and clients as long as performance holds up. When things turn the other way, as they inevitably do, what looked like small tears in the cultural fabric become big rips that are obvious to all. Mending them is hard and unfamiliar work for leaders. The clients often choose to walk away.

Speaking of how organizations work, here’s a short summary of CUDOS, an interesting model of the best kinds of knowledge communities. Does it describe yours?

If you aren’t getting these updates via email but would like to, subscribe here. Now, on to the readings.

Cognitive diversity

Alex Edmans has produced a comprehensive report on an important topic: “Cognitive Diversity in Asset Management.” (Don’t let the title fool you; the content is of value to those in other parts of the investment ecosystem who don’t consider themselves asset managers per se.)

Talking about diversity in organizations has always been tricky and it has gotten trickier of late as the topic has become increasingly politicized. But beliefs about diversity — both social and cognitive — shape how organizations are built and affect how decisions are made.

When asked about diversity, some leaders are quick to say that what is important is cognitive diversity, but they struggle to articulate anything meaningful about the concept and fail to demonstrate how that belief is reflected in the team that has been assembled.

Edmans’ report is long and includes overviews of a wide range of research on the topic as well as insights gleaned from interviews with investment practitioners. The executive summary illustrates the balanced and nuanced view that Edmans provides throughout, and the short “What is Cognitive Diversity?” section that follows it includes this:

This report argues that cognitive diversity, properly implemented, can have a significantly positive effect on investment performance . . . [and] its objectives are twofold.

The first is to identify the specific benefits and costs of cognitive diversity, the types of cognitive diversity for which the benefits might outweigh the costs, and the settings in which cognitive diversity is overall beneficial or detrimental, rather than to make broad statements about cognitive diversity in general. The second is to discuss what asset management firms can do to fully harness the advantages of cognitive diversity while mitigating its risks.

The due diligence dilemma

A paper by Yifat Aran and Nizan Packin looks at venture capital firms and the “core tension between the imperative to invest rapidly and the widespread, yet often unfulfilled, expectation that VC firms serve as effective gatekeepers through independent diligence.”

Its ultimate purpose is to explore the legal ramifications of due diligence choices, but don’t let that deter you from reading the first two sections, which effectively demonstrate how “due diligence practices evolve with market dynamics.” That general industry problem is easiest to see in venture capital, because of “the discrepancies between the thorough scrutiny often portrayed in VC literature and the realities of investment decision-making, particularly during market peaks.”

The result is “a diligence culture skewed toward optimism” that “has created a collective action problem.” Namely, many investors engage in “proxy due diligence,” relying on the reputations of the big-name investors who are involved as proof that proper diligence has been conducted. That is a questionable assumption. Euphoric times beget little scrutiny and fast, superficial decisions.

The salient case of venture capital is part of a broader issue. Reliance on the due diligence efforts of others is built into most every part of the investment industry. Too often the quality of work is not as advertised.

Mimetic organizations

FT Alphaville kicked off “an informal series of simple Q&A interviews” with a conversation with Gappy Paleologo of Balyasny Asset Management. In comparing managers Paleologo said:

The key to understanding differences in hedge funds is the difference in personality of the founders, because hedge funds are incredibly mimetic organisations. There’s an absolute leader, and the people who report to them tend to mimic the leader. Over time they acquire the same tics and personality traits.

Among those he references are Citadel, Millennium, Hudson River, and Balyasny. (You might also be interested in Paleologo’s Odd Lots interview with Tracy Alloway and Joe Weisenthal.)

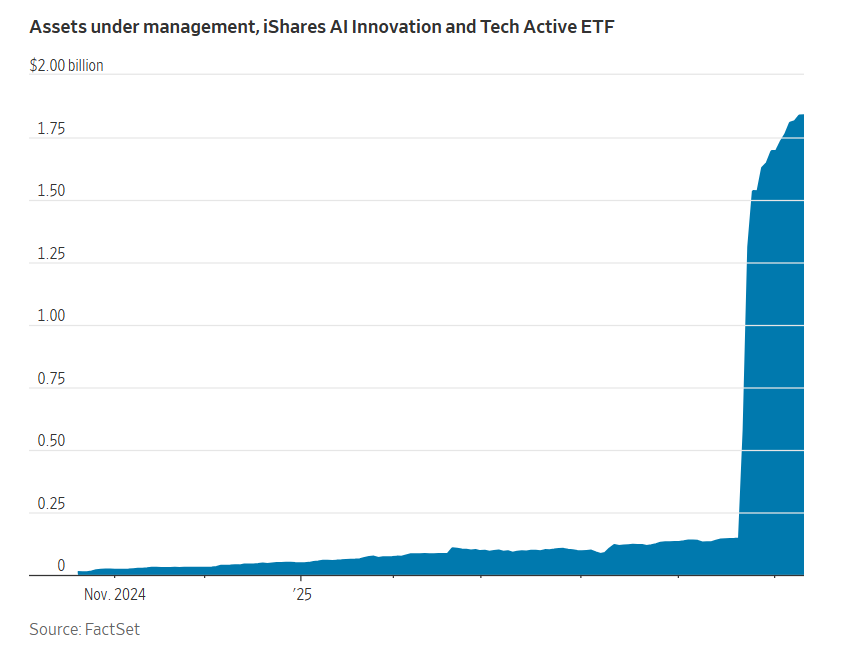

Model flows

Phil Bak included this chart in a posting about model portfolios. It shows how quickly assets can flow into a new strategy when the creator of the product, in this case BlackRock, includes it in one of its models. (Bak added an ironic “organic flows” description underneath the chart.)

His broader point is how the move to model portfolios is changing the industry script:

Inertia is destiny. For fund managers, if you’re not in the default, you’re not in the game. If you’re not embedded now, every quarter that passes compounds your irrelevance.

The industrialization of the advice industry proceeds apace.

Love of the game

Devyani Aggarwal wrote a paper about the movement of private equity into new areas:

In recent years, private funds seem to be expanding their interest beyond these traditional sectors and targeting high-profile, culturally significant industries such as sports, fashion, music, etc. Interestingly, these industries share little in common with the traditionally favored sectors that attract PE: they are arguably unpredictable, more risky, less reliable, and engaged in the production of relatively “non-essential” services and commodities. So where is the appeal?

She looks at the “unique legal, regulatory, financial, and governance challenges” involved, using investments in the business of sports to illustrate those challenges. (For investors, there is also a question of how the personal excitement of investing in those areas intersects with the need to make objective judgments about the appropriate valuation of them.)

Other reads

“Thesis Drift,” Philo, MD&A.

Thesis drift is entirely psychological in nature. It is natural to want to avoid admitting to yourself that you were wrong or that you didn’t know what you were doing, as it conflicts with your self-image as someone who is smart or has good instincts. If you have made public pronouncements about your position, changing your mind threatens your external image as well.

“Why Do Some Assets Become More Attractive As they Become More Expensive?” Joe Wiggins, Behavioural Investment. Strong, weak, and nonexistent valuation anchors — and “belief assets.”

“The (Uncertain) Payoff from Alternative Investments: Many a slip between the cup and the lip?” Aswath Damodaran, Musings on Markets.

If there is one takeaway from this post, I hope that it is that historical correlations, especially when you have non-traded investments at play, are untrustworthy and that alphas fade over time, and more so when the vehicles that delivered them are sold relentlessly.

“A Pioneer in Private Credit Warns the Industry Is Ruining Its Golden Era,” Miriam Gottfried, Wall Street Journal. Have private credit shops “become factories, churning out deals with little consideration of their long-term prospects”?

“False Precision and Framing Houses,” Christopher Schelling, LinkedIn.

Math in finance is just an approximation because we are measuring results that are all based upon the behavior of market participants. Fewer things in our industry have fixed effects like they do in the physical sciences. We need to view results with a healthy dose of skepticism and humility.

“When looking at private investments, the past is prologue,” Joachim Klement, Klement on Investing. Regarding a paper that shows “how interim valuations change and how stale they are provides valuable information about the future performance of assets in a private equity portfolio.”

“The Growing Index Effect in the Corporate Bond Market,” Sean Shin, et al., SSRN.

While liquidity during other periods of the trading day has declined, liquidity at index closing time has improved, resulting in a net positive effect. However, during periods of market stress, when trading becomes one-sided, this concentration of activity diminishes the benefits of indexing and leads to higher liquidity costs.

“Outperformed by AI: Time to Replace Your Analyst?” Michael Schopf, Enterprising Investor. The title of the conclusion: “Master the Tools — or Be Outpaced by Them.”

“What UnitedHealth Can Do to Revive Its Battered Stock,” David Wainer and Jonathan Weil, Wall Street Journal. Analytical standards are permeable:

The opacity wasn’t a problem for Wall Street as long as the company kept delivering. With a steady record of beating earnings estimates and a soaring stock, investors were content to let details slide.

New or new to you?

“Everything feels unprecedented when you haven’t engaged with history.” — Kelly Hayes.

Flashback: Statues

Today’s housing market is perplexing in many ways. Economists, investors, homeowners, and prospective home buyers are all looking for a sign of what’s to come.

Which is a reminder of a comment made during the Federal Open Market Committee meeting on September 20, 2006 by Sandra Pianalto, president of the Cleveland Fed. From the minutes:

I heard a report yesterday morning that sales at religious stores for statues of St. Joseph have been soaring. [Laughter] It seems as though people who are trying to sell their homes are buying statues of St. Joseph because he’s the patron saint of real estate, and they’re burying him next to the “For Sale” sign. Unfortunately, there is no patron saint for central bankers. [Laughter]

It turned out to be one of the greatest indicators of all time (and no laughing matter).

Postings

You can search the archives for original essays in the categories of interest to you. For example, a 2021 posting looks at a paper by Fidelity about the “investment innovators curve”:

The various positions along the innovators curve have their pros and cons, their (apparent) risks and returns. Where is your organization and where do you think it should be (and why)?

Thanks for reading. Many happy total returns.

Published: June 30, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.