Here is a full slate of ideas for you to digest!

Second-order effects

Counterpoint Global produced a report, “AI Beneficiaries: Investing in Second-Order Effects.” The title plays on the firm’s findings that “the best investments were often not the obvious, first-order ones but rather the second-order ones.” In this case, they are looking at the hot topic of the moment and asking whether the big economic winners will ultimately be the users of AI.

In its initial “Culture Quant” research a few years ago, tapping an alternative dataset covering more than 300 million employees, the firm “found a strong positive correlation between high employee retention and stock price outperformance.” The new report involves a more complicated analysis that tries to assess the net effect of changes related to the implementation of AI on corporate profitability.

Industry and company examples are included, as well as a section on company life cycles and capital allocation. (See this earlier Investment Ecosystem posting on that topic.) The report says that despite the sense that a life cycle only proceeds one way, firms “can revert to earlier stages when new opportunities arise.” AI is nothing if not a new opportunity.

The report is interesting and worthwhile. A blunt take is that head count will go down and profits will go up. But consider the point from the firm’s earlier research about retention. The envisioned changes from AI also will have an unprecedented effect on corporate culture, leading to unanticipated outcomes. In other words, while Culture Quant is important, Culture Qual is unpredictable when making changes of this magnitude.

Thinking ahead

Thinking Ahead Institute (affiliated with WTW) has produced “What Asset Owners Did Next,” follow-up to a 2017 study of leading asset owners from around the world.

The “nutshell” summary says that asset owners are “buckling under peak busy conditions in which business as usual (BAU) is more complex than ever and business beyond usual (BBU) is not getting enough bandwidth.” Thematically, competitive edge “can be maintained through focus on three key areas: it takes a system to manage a system, the soft stuff is the hard stuff, and what gets measured gets managed.”

An incredible number of topics are covered, each using a format of “the story so far” and “what happens next.” The sheer heft of it all indicates that these asset owners all have large organizations, but smaller entities (who can’t cover all of the bases at once) might find some ideas to put into practice.

The FT on PE

While concerns about private equity have been percolating for a while, there has been a noticeable change in tone of late, as can be seen in the stories from any financial publication. To pick one, here are some representative stories from the Financial Times.

“Big investors look to sell out of private equity after market rout.” This was published in early April after the downdraft in public markets following Trump’s tariff announcements. While equities have snapped back, the underlying portfolio realities remain: high exposure to PE and low distributions have changed the perceptions about that asset class. In the meantime, the looming effects of changes in taxation on endowments and foundations — plus the announcements about high-profile investors reducing exposure — have reinforced the worries.

“Private equity founder warns retail investors risk being saddled with worst assets.” The industry has been aggressive in trying to move to the private wealth channel to stay on the growth path. Many observers have also seen that push as a way for the industry to offload companies to unsuspecting retail clients anxious to get in on the gold rush they have heard about. It’s unusual for someone at a PE firm to state that case.

“The delusion of private equity IRRs.” A guest column by Ludovic Phalippou runs through the problems with internal rates of return and how they are misused by providers and buyers alike throughout the industry, leading to “capital allocation distortions”:

The industry insists that institutional investors are smart and sophisticated enough to see the limits of IRR and run their own numbers. Maybe. But it seems more doubtful that ordinary investors will see through the theatre.

“Is private equity becoming a money trap?” Another opinion piece comes from Daniel Rasmussen of Verdad Advisers. In his view, over the last several years “allocations started to outpace the size of the market.” Plus, “private equity-backed companies” — the holdings in PE funds — “are under strain.” His conclusion is that the belief in private equity, a one-way train for decades, is changing:

The consensus on private equity is being quietly, but decisively, rewritten. The question now is not whether the model is being broken. It is whether the exit is wide enough for everyone trying to leave.

Target-date funds

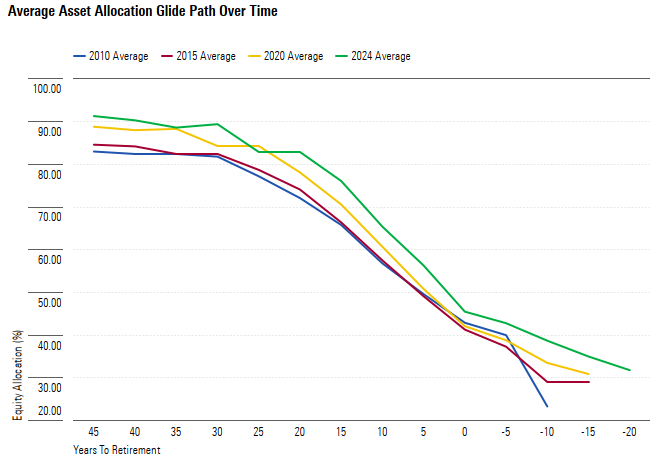

Morningstar includes a number of charts in its “2025 Target-Date Fund Landscape” report, including the one above. It shows that (on average) the percentage allocation to equity has risen over time. The firm chalks that up to low interest rates during much of the last fifteen years. Now that rates have increased, will lower allocations to equity follow?

Target-date funds have been a hit in the marketplace, growing at a 30% clip since 2009, when they totaled $272 billion, to today’s $4 trillion. The report includes looks at the largest providers (Vanguard leads by a lot), the shares of active and passive, the conversions from mutual funds to collective investment trusts, and the ongoing decline in fees.

Digging for nuggets

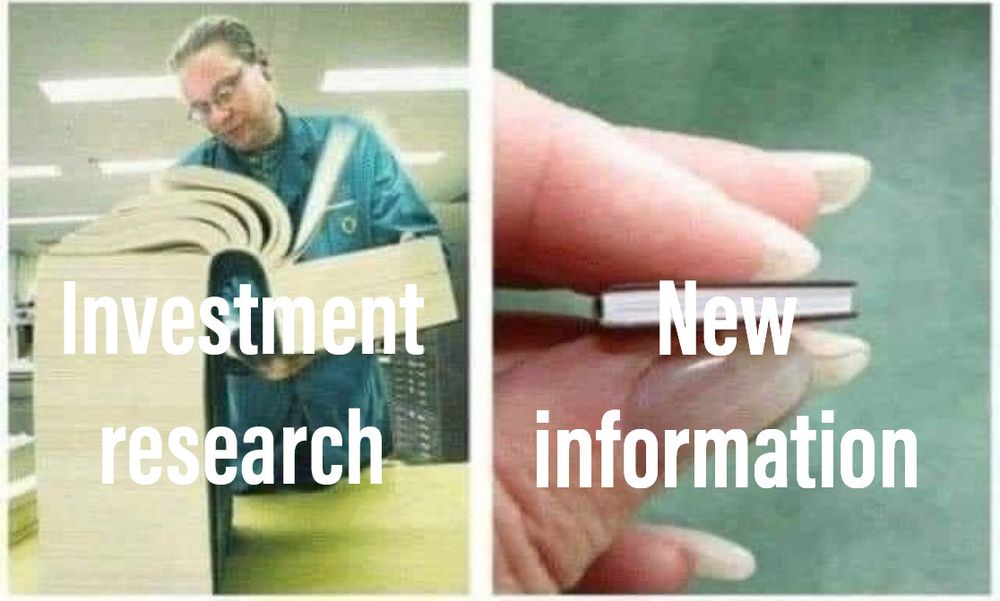

Rupak Ghose posted this diptych on Bluesky without commentary.

In its simplicity it represents one of the main challenges of the investment endeavor. On a macro level there is an excess of published ideas; sorting through it can seem like an impossible task. But large chunks of that constant stream are perfunctory and unnecessary — just think of the time spent creating and digesting predictions of one kind or another, usually to little benefit, although a realization of their ineffectiveness never seem to impede the demand or supply.

The images also fit when it comes to the documentation of an individual investment recommendation. Leave something out and you could be accused of not doing your due diligence (either at the time of the recommendation or after the fact if it doesn’t come through as advertised). So it’s easy for the new information, the valuable information, to get lost in a blizzard of paper or pixels. That puts a premium on good report design, something sorely lacking in many parts of the business.

(Commercial break: We help organizations improve their recommendation and documentation practices. Also, you also can find The Investment Ecosystem on the Bluesky platform.)

Other reads

“Stepstone’s NAV Juicer,” Tim McGlinn, LinkedIn.

Oh, to be a Secondary PE manager in 2025, 😊 generating immediate and high-quality investment returns by buying things . . . then rinse and repeat with fresh inflows of capital . . .

“Adversarial Attacks in Statistical Arbitrage,” Richard Dewey, The Diff. A look at the 2007 quant crisis when “there were two different systems with varying degrees of sophistication interacting with each other” — and the implications of those dynamics for the agentic AI to come.

“Leadership in Boutique Asset Management,” Sebastian Stewart, Independent Investment Management Initiative.

Little research has been conducted on leadership within the asset management industry, and even less so on the segment of the industry classified as “boutique asset management.”

The survey results suggest that around half of those in a management position in the UK’s boutique asset management sector are there by default rather than design.

“Same As It Ever Was,” Jon Petersen, Novel Investor. Will “buy the dip” ever quit working?

“Private Funds Are Turning to Complex Bonds to Tackle Cash Crunch,” Kat Hidalgo and Scott Carpenter, Bloomberg.

But as CFOs [collateralized fund obligations] get more popular, some are concerned about the bundling of unrated private funds into instruments with top ratings.

“The Walking Wounded,” Anthony Hagan, Freedomization. A limited partner’s “armor gets thicker and thicker” every time he or she “gets burned by a GP.”

“The Evergreen Evolution,” Zane Carmean, et al., PitchBook.

While not new, a growing share of private market investment is being allocated to evergreen and open-ended fund structures. These help GPs avoid the lumpiness of sporadic fund launches and inopportune end-of-life liquidations in the traditional drawdown/finite-life structure. For LPs, these funds provide a simpler way to manage private market allocations and, by gaining full allocation from the subscription date to redemption, more exposure to the benefits of compounding returns.

“The Whisper Before the Shout: Market Consequences of Implied versus Actual Recommendations Revisions,” Mark Bradshaw, et al., SSRN. Do analysts signal changes in sentiment before they actually adjust their recommendations?

“How Teamwork Makes The Dream Work,” Brett Steenbarger, TraderFeed.

The best teams work as hard on their teamwork as on their markets. They constantly look to improve what each person looks at, how they look at it, and how they communicate. They work as hard on team goals as individual goals. They review team performance every bit as much as they review their own individual performance.

Metamorphosis

“Once a majority of players adopts a heretofore contrarian position, the minority view becomes the widely held perspective.” — David Swensen (from a set of financial history quotes put together by Mark Higgins and Rachel Kloepfer).

Flashback: Big money in Boston

The last Fortnightly featured a flashback to a piece from 1970 about mutual fund complexes. In it, Jack Bogle, then at Wellington and also chairman of the Investment Company Institute, an industry advocacy group, was quoted as talking optimistically about the cozy relationship between mutual funds and their advisors. A few years later he would found Vanguard and become a critic of that model.

In 2013, Bogle penned a Journal of Portfolio Management article, “‘Big Money in Boston’: The Commercialization of the Mutual Fund Industry.” More than sixty years earlier he had read a story titled “Big Money in Boston,” then “the center of the fund universe.” He wanted in — but over time:

The fund industry that I read about in Fortune was a profession with elements of a business. It would soon begin its journey to becoming a business with elements of a profession and, I would argue, not enough of those elements.

Bogle traces the evolution of the industry (and his own evolution in thinking), including a couple of dates “that will live in infamy” and the disparate fee paths of most mutual funds (higher and higher) and Vanguard (lower and lower) that eventually led to an unsustainable gap between the two — and increased pressure on the business models of traditional funds.

Postings

All of the postings since inception may be found in the archives.

For example, a 2022 perspective, “We Need Some New Terminology (Part 2),” deals with the fuzzy and varied uses for the term “passive investing” including:

Look around. Some firms promote “passive” approaches — taking advantage of the salience of that term — when the strategies they offer involve layers of active choices. Others try to hew to an ideal like Sharpe’s — and a few off them tie themselves in knots over some of the sticky implementation questions that arise when trying to reach that goal.

(FYI, Part 1 dealt with the also-fuzzy-and-varied uses of “advisor.”)

Thank you for reading. Many happy total returns.

Published: June 2, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.