During chaotic times like these, the tendency is toward myopia, as near-term happenings demand attention. But letting needed improvements slide increases organizational debt that needs to be tackled when things settle down. (If ever.)

Don’t let that happen. Reach out if you need a hand or a sounding board.

On to the readings.

Trend following

How would you describe the current trend in equities? In other markets? It’s been a crazy time, with abrupt shifts, the kind of action that’s not made to order for trend-following funds.

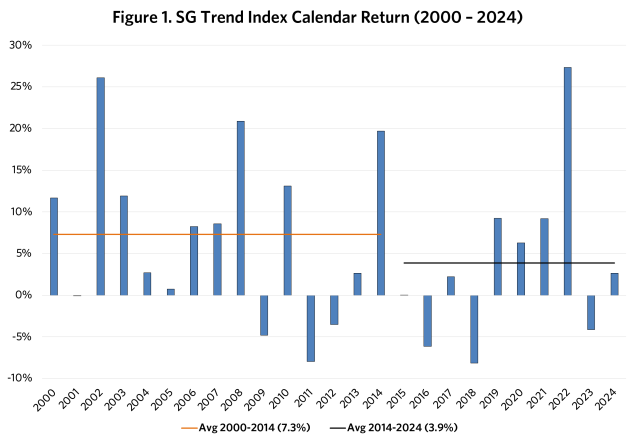

We’ve arguably already had two instances of “initial shock and position misalignment,” one of three recurring patterns that mark the strategy, as identified in a Man Group report. The other two are “adaptive recalibration” (hard to do in back-and-forth markets) and “delivering crisis alpha.” Three charts plot that alpha, showing the performance of large trend followers (using the SG Trend Index) versus the S&P 500 during the dot-com bust, the financial crisis, and the “inflation episode” of 2022.

Another account, from Jim Masturzo of Research Affiliates, totals the excess returns using the same index for the three worst calendar years this century as 49.5%, 59.4%, and 46.8%! That said, the absolute returns have downshifted during the last decade:

Masturzo writes:

At its core, the construction of trend-following strategies is a trade-off between Sharpe ratio (i.e., higher average risk-adjusted returns over time) and positive skewness. The tail protection comes from the skew, but the Sharpe ratio should not be overlooked because it is often what allows investors to remain in a strategy during extended bull markets.

And he offers trade-offs for portfolio construction to achieve the desired balance between the two.

Additional perspectives on trend following come from AlphaSimplex, Methods to the Madness, and Rupak Ghose (who offers a short history of trend-following funds).

Playing a bigger game

In “The Portfolio Problem,” a Behavioural Investment posting, Joe Wiggins writes:

What has seemingly been forgotten is that there is a yawning gulf between these two statements:

“I am investing to meet my clients’ long-term outcomes, hopefully my approach will mean I can do it better than others over time.”

and

“I am investing to beat the returns of people doing similar things to me, hopefully I might also deliver good long-term outcomes.”

That serves as a good lead-in to “Playing a Bigger Game,” a white paper by Carol Geremia of MFS. It challenges those individuals and organizations “in the middle of the investment chain, between the end investor and the public companies in which they invest” to reconsider what they say they do versus what they actually do.

A lot of ground is covered, including the collapse in time horizons, benchmarking misalignments, the effect of passive investment, and the disconnect between investment objectives and performance measurement.

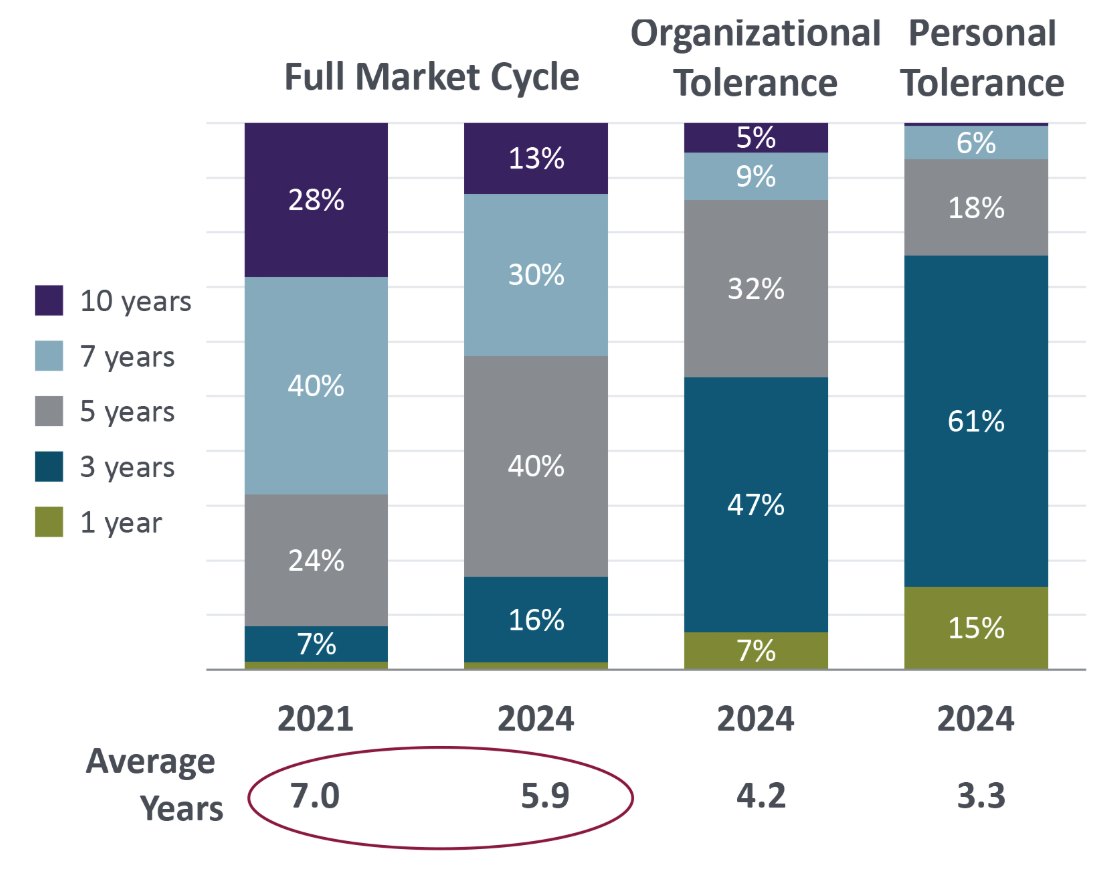

Here’s one of the exhibits, which summarizes the results of a survey of global investors:

The first two columns show that on average the assessment of those investors as to what constitutes a “full market cycle” has shrunk recently, despite the fact that those cycles have lengthened over the last few decades from what they had been historically.

But look at the last two columns. They chart responses to the question, “How long are you willing to tolerate underperformance of active managers?” The industry has institutionalized performance chasing rather than long-term investment, leading to the dichotomy that Wiggins summarized.

White smoke

Rajiv Sethi analyzed the betting on prediction markets in advance of the naming of the new pope. In his posting, he wrote about the surge in the price of the contract on Pietro Parolin after the white smoke appeared (while the probability of Pope Leo being selected remained essentially at zero until the actual announcement):

Although it’s clear in hindsight that there was no leakage of inside information, this was not known to traders in real time. They saw the price rising, and tried to interpret this.

That is, while no trader knew the identity of the new pope, they suspected that some other traders knew. And by treating the price movements themselves as informative, traders acted in ways that amplified these movements.

Which led Sethi to this conclusion:

This episode reveals something quite general about financial markets. It shows that momentum trading can be profitable under certain conditions, but also that too much of it can destabilize markets.

Consolidation

A Morningstar report, “Consolidation in the European Asset-Management Industry,” is subtitled “The elusive benefits of scale.” As asset management firms — especially “traditional” ones — search for a winning formula, mergers are one option, but:

The benefits of consolidation touted by dealmakers are often hard to realize in practice . . . as consolidation presents five critical integration challenges: cultural misalignment, leadership complexity, talent exodus, product rationalization risks, and scale disadvantages that may compromise performance.

The report compares three types of firms, which it classifies as organic growers, consolidators, and opportunistic acquirers — and looks at the outcomes of three major mergers: Amundi, Janus Henderson, and Aberdeen.

PMs as entrepreneurs

In an usual take on the active-passive debate, Lotta Moberg and Brian Singer published “Financial Entrepreneurship,” a brief from the CFA Institute Research Foundation.

The thesis is that “active investors are the entrepreneurs of finance,” who “either create new opportunities or exploit existing ones in new ways.” Furthermore, the entrepreneurs are those with “ultimate decision-making authority,” principally portfolio managers. While the piece contains a variety of interesting points worth dissecting, it bathes those investors in a heroic light. To wit: “Wisdom is the purview of the portfolio managers.”

Other reads

“30 ‘pearls’ of wisdom from our last 30 years,” Paul Zummo, J.P. Morgan Asset Management. A terrific list (and accompanying commentary).

“Deferred Conviction: The Illusion of Skin in the Game,” Anthony Hagan and Shahrukh Khan, Cash and Carried.

GP commitments once signaled belief. Today, they’re often financed, waived, or deferred by fund managers raising ever-bigger funds.

“The Endowment Model Reimagined,” Jeff Blazek and Rebekah McMillan, Neuberger Berman. An argument that what the model needs in order to be refreshed is an increased focus on the science of portfolio construction.

“A Few Questions,” Morgan Housel, Collaborative Fund. Reflective examinations of beliefs and behavior.

“Productive versus Parasitic Finance,” Christopher Schelling, LinkedIn. When is investment activity productive for society and the economy, and when is it just “finance for finance’s sake”?

“Even with AI, junior bankers still need the grind,” Craig Coben, Financial Times.

This is the paradox juniors face: the work they resent is often the scaffolding for the judgment they’ll need. AI may spare them some tedium, but it can’t simulate the slow, accretive development of instinct — the bit of intuition that only comes from having made mistakes or having seen them made.

“The Rule of 3,” Jim Ware, Focus Consulting Group. Within an organization, can communication be improved be means of this simple idea?

“The Politics of Venture Capital Investment,” Jeffery Wang, SSRN.

VC partners are more likely to invest in startups managed by co-partisan CEOs [but] co-partisan investments underperform relative to non-co-partisan deals made by the same VC partners.

“Why can’t more financial heavyweights write letters like Warren Buffett?” Pilita Clark, Financial Times. Principally because they don’t like to admit their blunders.

Don’t do this

“When most people give presentations, they try to squeeze two megabytes of data into a pipe that carries 128 kilobytes.” — Steve Jobs.

Flashback: Mutual funds

“A Study of Mutual Fund Complexes” was written in 1970. What could possibly be relevant today in a piece from that period? More than you’d think.

Even though the industry was tiny by current standards, structurally it resembles what we see today. And the article speaks to an issue that still exists:

The emergence of the “complex” as the dominant form of organization within the mutual fund industry has added a new dimension to the problems raised by the external management relationship between most funds and their investment advisers.

The odd “community of interest” between the funds in a complex and the management company — and many of the inherent conflicts involved — remain in place, including that “the adviser sometimes has a greater self-interest in some funds than in others.” In practice, that can drive decision making within the management company in ways unexpected by the owners of some funds.

While the emphasis is on structural and legal matters, the footnotes are full of references to people and firms that were instrumental in the development of the industry, as well as evergreen challenges, including this one, quoted from a letter to the shareholders of the T. Rowe Price New Horizons Fund:

With most of the stocks in the Fund’s portfolio and new candidates for investment selling at prices far above our buy limits, it was simply impossible to invest the large flow of new money to advantage; consequently, management restricted sale of new shares.

Postings

All of the postings can be found in the archives. For example, from “Challenges and Quandaries in Manager Research,” based on events at Pimco, but full of questions that apply universally, including:

Are asset management organizations different from other kinds of organizations when it comes to the methods for creating a culture that leads to sustainable success?

If so, why, and in what way?

Thank for reading. Many happy total returns.

Published: May 19, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.