If your organization is looking for ways to foster or further your continuous improvement efforts, the Investment Ecosystem can help. Change is a constant — you can either be proactive in dealing with the possibilities or reactive in picking up the pieces. Reach out today to explore your options.

On to the readings.

Credit

Over the years, Howard Marks of Oaktree has developed a ready audience for his “memos” about the craft of investing. His latest, “Gimme Credit,” delves into the two questions most asked by clients.

The first concerns spreads and whether they compensate for the risk inherent in high yield bonds. In general,

The spread is a good barometer of investor psychology, or a “fear gauge.” It’s worth noting the obvious: the spread doesn’t tell you what the actual default rate will be, as some mistakenly say. It tells you what investors think the default rate will be. The thoughtful investor has to evaluate that expression of opinion against what the reality is likely to be and assess whether investors are being too optimistic or too pessimistic.

With “one of the narrowest spreads on record,” are investors being properly compensated today? Marks thinks that concerns about spreads are “very much overblown.” (He would probably feel even more that way now, since high yield spreads have increased by fifty basis points since his memo was published just eleven days ago.)

His rational:

~ The historical average default rate overstates the typical experience, because of a couple of rough patches along the way. (That points to the fact that recessions are the curse for those predicting default rates, just as they are for equity analysts forecasting earnings. Serious consequences in each case if those recessions are unforeseen.)

~ “It can be argued that the macro environment is safer.” (There are plenty who have changed their minds about that of late.)

~ The overall credit quality of the high yield market has improved over time.

~ Spread widening (akin to volatility in stocks) can lead to better reinvestment rates and opportunistic positioning by astute active managers.

The other area of interest from Oaktree clients is private credit. On the positive side, there are higher yields available there and managers can lever the portfolios (albeit, that’s a double-edged sword). But there’s no ready market for many of the loans and fees are higher.

As with private equity, the stated level of volatility on private credit is “obviously unrealistic,” but not marking the portfolios to market “may be welcome.” (Hopefully we’ll get past that charade one of these days.) The big unknown is that “the tide has never gone out on private credit,” so “we don’t know what’ll happen if and when a difficult environment does arrive.” On a macro basis, Marks doesn’t think that private credit poses a systemic risk.

Speaking of which, the Bank for International Settlements released a report on the “global drivers of private credit,” concluding:

From a financial stability perspective, developments in funds’ investor base, including the growing role of insurance companies and retail investors, as well as funds’ leverage and degree of portfolio concentration warrant monitoring. This is especially relevant in light of growing interlinkages between banks and private credit.

The report covers concentration risks, specialization versus diversification within funds, the demand and supply drivers during the strong growth in the category, and the cost of capital for private credit funds as compared to banks.

Other pieces on private credit:

~ “Is the Shine Coming Off of Private Credit’s ‘Golden Age’?” Bailey McCann, Chief Investment Officer.

~ “Has Private Credit Broken the High-Yield Spread Signal?” Greg Obenshain, Verdad.

Whither alternatives?

The abstract for “The Demise of Alternative Investments,” by Richard Ennis, forthcoming in the Journal of Portfolio Management, states his premise:

Alternative investments, or alts, cost too much to be a fixture of institutional investing.

The article drives home the point:

The assets that you get when you index are pretty much like the assets that you’re invested in with all these fancy fee schemes. So, it’s just basic arithmetic. It’s not complicated.

Except that quote isn’t from Ennis. It’s from David Swensen (in 2009), who most would regard as the godfather of alternative investing.

In addition to analyses of the “extraordinary cost and ordinary returns” of alts, Ennis looks at the behavioral reasons that they have taken over the landscape. Among them are the high expected returns used for actuarial calculations (based upon suspect internal rate of return calculations), and “agency problems and governance weakness”:

The funds’ CIOs and consultant-advisors, who are responsible for formulating and implementing investment strategy, have an incentive to favor complex strategies. They can earn much greater salaries and consulting fees advocating complex investments. Plus, it helps burnish their reputations as shrewd investors. And they get to do it with large amounts of other people’s money.

Ennis thinks that the endowment model will fade away over the next two decades. That would represent a revolution in investment activity even more surprising than the one that brought us to this point.

Three innovators pass on

Worth your time are stories of the passing of three innovators — a businessman, a pioneering investment researcher, and a renowned academic:

~ Bob Kierlin founded Fastenal in his hometown of Winona, Minnesota. His obituary in the Wall Street Journal highlighted “the Kierlin creed of extreme cost control and decentralized management,” his personal thrift, and his ten rules of leadership. (In a video interview, Kierlin discussed his philosophy.) An article in the Minnesota Star Tribune gave more examples of his frugality, as well as his public service, charitable contributions, and humility. It was a formula for success: since its 1987 IPO, Fastenal stock has returned almost 191,000%, over 22% per year.

~ The Financial Times offered a retrospective on the career of “quant-father” Barr Rosenberg.

In May 1978, the magazine Institutional Investor put Rosenberg on the cover, depicting him as a cerebral, pink-robed giant with flowers in his hair and posing in the lotus position. Around him tiny men in suits prostrated themselves in admiration.

Through Barra, the consultancy he founded (which eventually became part of MSCI), Rosenberg led a revolution in the application of quantitative techniques to institutional investment management. He later created a successful asset management firm, but a delay in fixing a problem with a risk management model led to the end of his career.

~ It has been a year since Daniel Kahneman passed away, but a new Jason Zweig article explores the Nobel Prize winner’s decision to end his life by assisted suicide at age ninety. An important if unsettled reflection from someone who knew Kahneman well.

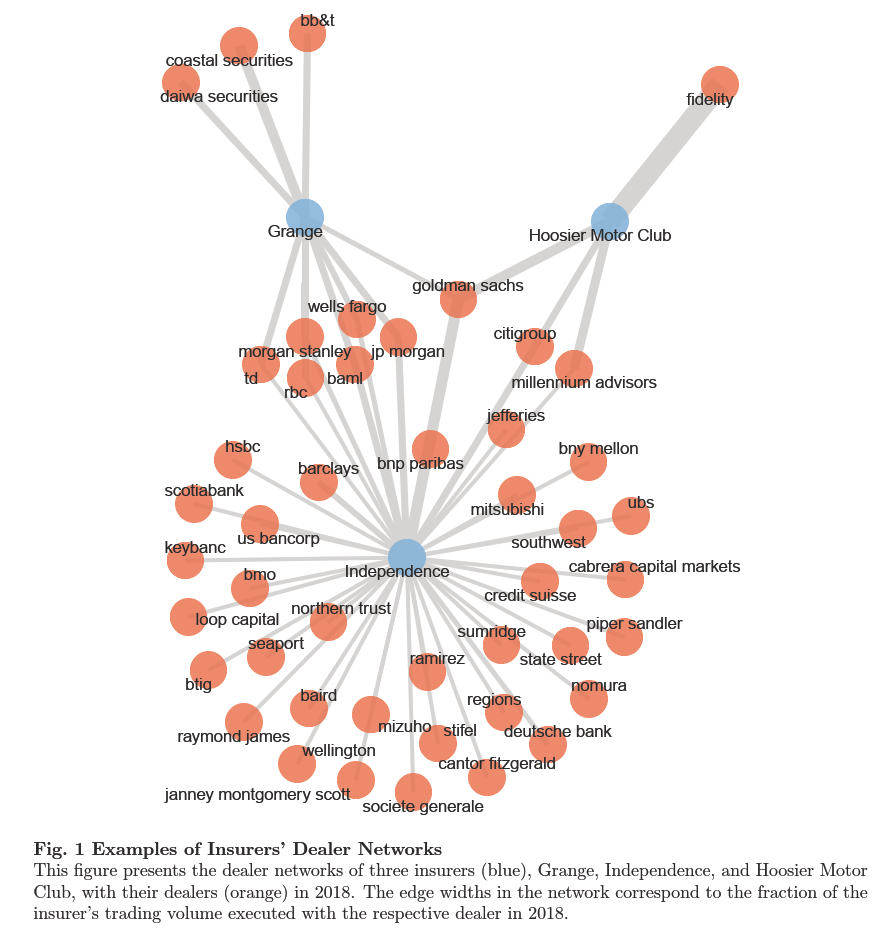

Mapping the network

It’s unusual to be able to map the information networks of a firm (a topic dealt with in a 2022 posting), but Stefan Huber, et al. were able to do something akin to that by accessing an unusual database to study “Information Flows in Trading Networks.” From the transaction-level data that they studied from insurance companies, they come to a number of conclusions, including that “investors with larger dealer trading networks make superior trading decisions before changes in credit fundamentals and yield better risk-adjusted performance.”

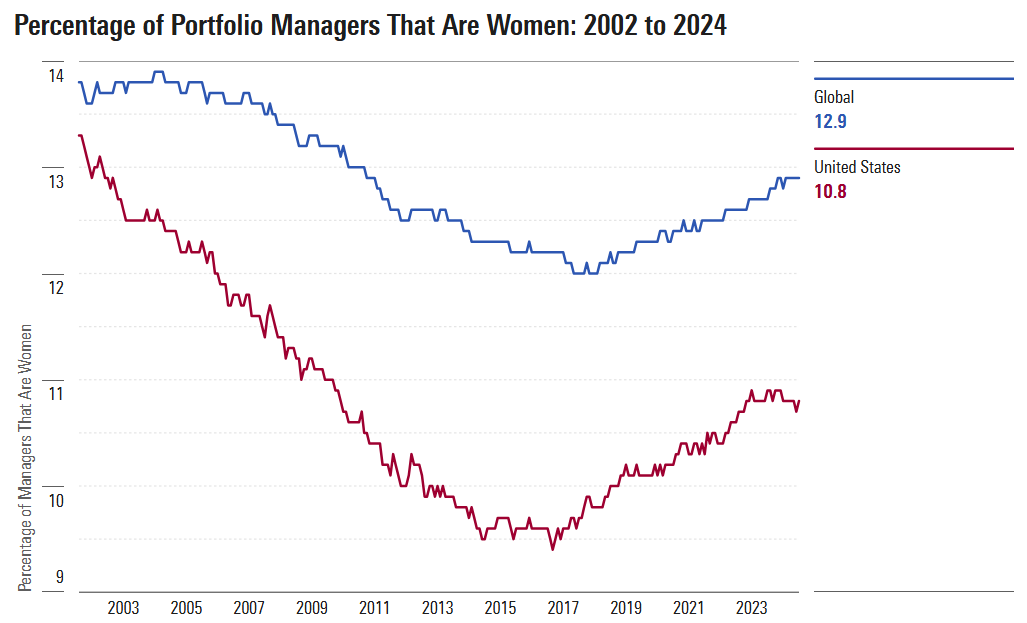

Still a man’s world

Alyssa Stankiewicz of Morningstar ran the numbers on gender representation in the ranks of portfolio managers and there are fewer women today in percentage terms than in 2002.

At the same time, the percentage of funds with at least one woman manager has gone up over that time — in the U.S. and globally — because portfolio teams are larger than they used to be. Women also have a much higher representation among passive funds than active ones.

The staffs of asset managers have always had areas where it was more common for women to be given a chance. Marketing, for one, and certain equity research industries. It looks like you can add “PM team member,” especially “passive PM team member” to the list.

Wannabes

At the Bloomberg Invest conference, a couple of CEOs offered comparisons of their (already successful) firms to a legendary one. At Brookfield, “with the insurance business owning our asset management and our investment operations,” it’s “really what Berkshire Hathaway is.” At KKR, it is trying to build what “is in some ways a mini Berkshire Hathaway.”

Other reads

“The Collaborative Model – Can’t We All Just Get Along?” Aaron Filbeck, CAIA Association.

Unlike its Norwegian, Endowment, or Maple contemporaries, TPA is not technically a “model” but instead more of an evolution in philosophy, mindset, and implementation. Perhaps the Collaborative Model is an evolution, while TPA is a revolution.

“Specter of Stagflation Threatens RIAs,” Matthew Crow, Mercer Capital. Will the business that has been rolling along unfazed for years be facing its toughest test? What about those aggressive rollups?

“His Hedge Fund Imploded in Spectacular Fashion. His New One Has $12 Billion.” Gregory Zuckerman, Wall Street Journal.

Nicholas Maounis oversaw one of the biggest hedge-fund fiascoes in history. Nearly two decades later, he is leading one of the fastest-growing funds.

“Investing Politics: Globalization Backlash and Government Disruption!” Aswath Damodaran, Musings on Markets. Macro and micro analyses of recent developments, including the impact on Tesla (see Damodaran’s framework for analysis of it in a posting that reviewed his life cycle book).

“Rushing to Judgment and the Banking Crisis of 2023,” Steven Kelly and Jonathan Rose, Federal Reserve Bank of Chicago.

We highlight seven facts that depart from the standard account of the crisis that has developed. We describe the crisis as a reaction to bank business models that focused on providing banking services to certain economic sectors, crypto-asset firms and venture capital, that had come under economic pressure during the preceding year.

“The ‘Why’ Question: Rebuilding Investment Theses from the Ground Up,” Polymath Investor. Steps and questions to apply first principles to investment analysis.

“What’s Behind the Capping Changes to the Russell Indices?” Nicole Wubbena, Callan.

At minimum, there is a lot to digest (at least educationally) with this development, but also a lot that only time and the markets will reveal as the implementation date of this methodology nears and crosses.

“Why Bother? ESG and Its Discontents,” Lewis Ireland, Dasseti. Despite the backlash — which seems to have turned into a full-scale retreat — “ESG is more relevant than ever.”

“Accounting considerations when studying private equity buyout portfolio companies,” Paul Lavery, SSRN.

During the PE holding period, portfolio company accounts are usually consolidated through one of these [acquisition] vehicles, as opposed to at the operating company level. This can make it difficult to accurately study portfolio company performance from pre- to post-buyout.

The way

“Obstacles do not block the path, they are the path.” — Zen proverb.

Flashback: Megatrends

According to his New York Times obituary, John Naisbitt was “a struggling business consultant and trend watcher who in 1982 hit it big with Megatrends, a book that galvanized a country just emerging from a gut-wrenching recession with its prediction of a bountiful high-tech economy right around the corner.”

The book was a sensation and the term stuck, to the point that a 2024 academic paper reviewed 267 studies of megatrends publications and offered “consensus characteristics” and a “standardized approach for developing and validating megatrends.” Consulting and investment firms continue to offer megatrends-themed predictions, including PGIM, Nuveen, and PWC.

You can judge the accuracy of Naisbitt’s megatrends by reviewing a short summary of them. The Wikipedia entry for him includes this quote from the book: “The political left and right are dead; all the action is being generated by a radical center.” That one turned out to be a clunker.

Postings

All of the previous issues of the Fortnightly are in the archives, as are essays on a wide variety of investment ecosystem topics. As an example, “Forbearance (Regarding Performance) is in the Eye of the Beholder” considers some research into how much leeway is given to an asset manager before the business is pulled from it. From the posting:

It is fine that the goal of the research was to describe current practice rather than assert an optimal time horizon after which the concept of forbearance is applied. But the counterproductive three-to-five year industry time frame which drives the tone of the article is not the standard by which impatience or trigger-happiness or tolerance should be judged.

Thank you for reading. Many happy total returns.

Published: March 17, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.