The most recent piece on the site is “Common Practices, Best Practices, and Next Practices,” which explores the dynamics of established practices and innovative ones:

So the question then is whether best practices are those that have stood the test of time and are widely implemented or those that are superior to others. In other words, what is the meaning of “best”?

To get every new posting via email when it is published, subscribe here.

Since the previous Fortnightly, the last two short items on concepts for evaluating investment organizations appeared on LinkedIn. They are social pressure and explanatory depth.

On to the readings.

Using LLMs

Alex Spyrou and Brian Pisaneschi wrote a report for CFA Institute, “Practical Guide for LLMs in the Financial Industry.” A “critical step”:

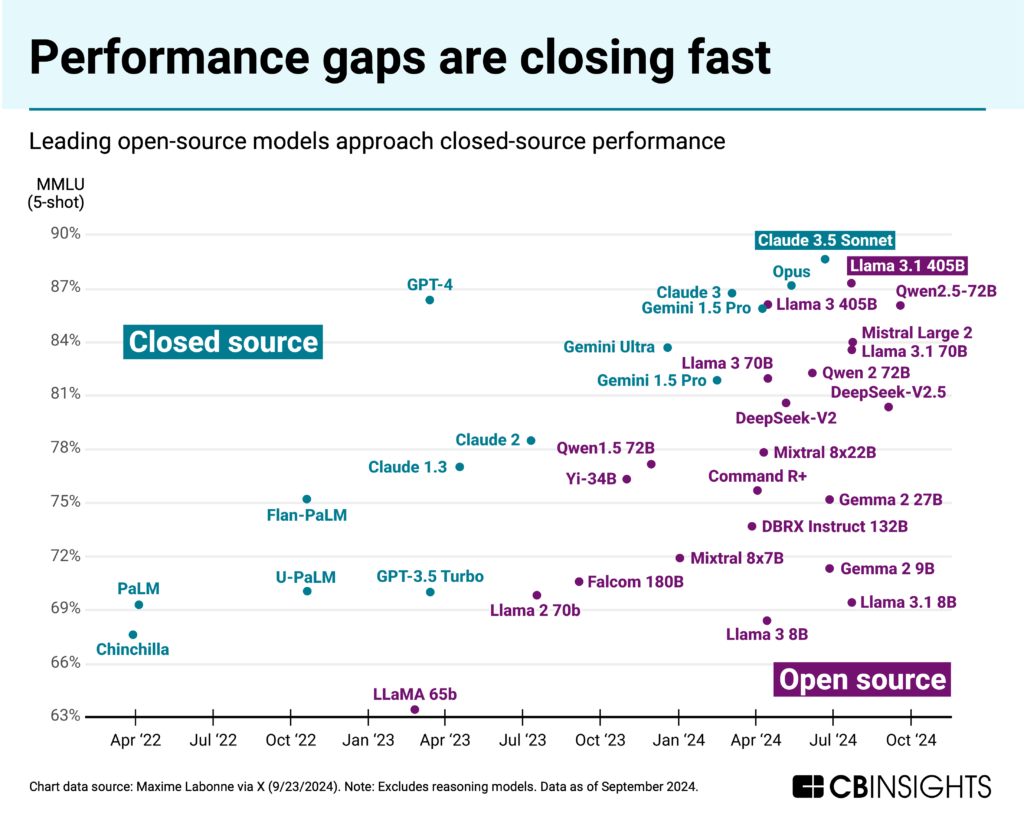

With the vast and evolving array of models available, financial institutions face an important decision: choosing between open-source and closed-source options.

The authors outline the benefits and challenges of using open-source models versus closed-source ones. (Along that line, a graphic from CB Insights shows how general open-source models are closing the performance gap.) Plus they include a number of examples and considerations.

{kind=link}

In case you’re wondering whether the Holy Grail has been found:

Stock movement prediction remains challenging for both FinLLMs and general purpose LLMs, with no model achieving consistently high accuracy.

GP stakes

Blue Owl published a paper, “The Anatomy of a GP Stakes Fund,” which breaks down the components of return from a GP stake, the elements of a transaction, the contributors to an entry valuation, and the calculation of “GP alpha.” It also compares GP stakes investments to secondaries purchased from limited partners.

One topic given a high profile could be described as “searching for a bucket.” Apparently Blue Owl thinks trying to figure out which asset category to put GP stakes in is something that is impeding adoption.

Of note on the sentiment front, the subtitle for the paper is “An Investment for All Seasons.”

Litigation finance

Asset managers have gotten increasingly interested in financing litigation, which makes “The Alchemist’s Inversion” by Samir Parikh an important read for asset owners. He calls the private equity firms and multistrategy hedge funds that are active as “opaque capital,” changing the dynamics of litigation finance. As for the title of the paper:

The Alchemist’s Inversion describes a litigation financier’s use of unethical and potentially illegal tactics to create, enhance, and marshal apparently low-value claims with the hope of turning them into gold.

By examining the move by these investors into mass tort, Parikh gives asset owners a look at the mechanics of litigation finance — and raises a potential question of whether or not they want to play the emerging game. In that sense it fits with the theme of an earlier Investment Ecosystem posting, “Does it Matter (How the Money is Made)?”

The market data industry

The Terminalist is an excellent newsletter about the market data industry. Its first three postings:

1 ~ What makes Bloomberg so successful. Its “Seven Powers” and the innovations that put it ahead of every one else in the business.

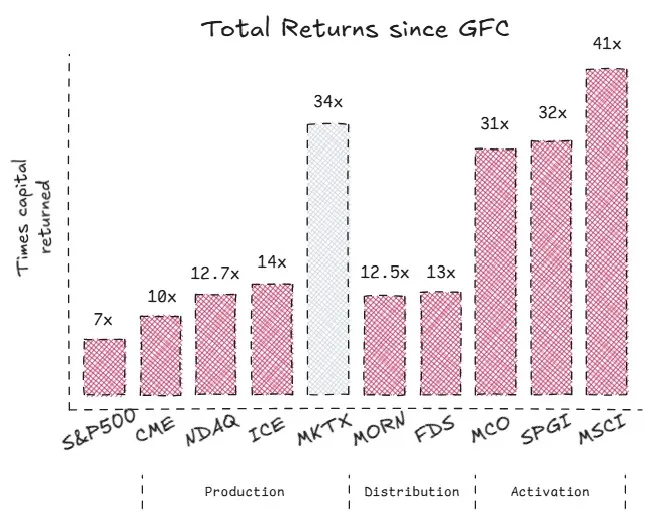

2 ~ How data travels across the ecosystem and the three acts of market data — production, distribution, and activation — with detailed looks at “pure-play champions” for each (CME, FactSet, and MSCI, respectively).

As financial data journeys from creation to consumption, it flows through a value chain that forms the nervous system of modern markets, transmitting millions of signals through a complex yet structured system.

3 ~ More detail on each of those functions and companies, as well as a look at their extraordinary returns since the financial crisis, shown below. (Left to right: the S&P 500; CME; Nasdaq; Intercontinental Exchange; MarketAxess; Morningstar; FactSet; Moody’s; S&P; MSCI.)

By the way, the author estimates Mike Bloomberg’s return since he started his firm (a different inception date than shown in the chart) to be 10,000 times his investment in 1981.

Safety in numbers

Charles Skorina, who is in the business of executive search for investment professionals, thinks that “Safety-in-numbers seems to be the new endowment-model-norm.” That is, everyone is using the same playbook (and it’s not working as well as it used to), including in the selection of talent:

Let’s be honest here. If the David Swenson of 1985 had applied for the CIO position at Yale today he would not have made it past the first round of interviews. A young untested Wall Street banker working on some exotic swap thing? Not a chance.

Rebalancing redux

The last Fortnightly included a reading from Vanguard on threshold-based rebalancing. Subsequently, Campbell Harvey, et al. released a paper, “The Unintended Consequences of Rebalancing,” which garnered a lot of attention in the financial press.

The authors find that “the predictability of these [calendar-based and threshold-based] trades enables certain market participants to profit by front-running the orders of large institutional funds.”

Other reads

“Slowly Melting Ice Cubes,” Phil Bak, BakStack.

Melting ice cubes are the anti-moat. And legacy asset managers are slowly melting ice cubes. Here is why, and here is what they should do about it.

“For junior allocators looking to be more involved in portfolio construction,” Dave Morehead, LinkedIn. Thoughtful suggestions from Baylor University’s chief investment officer.

“It’s time to rethink due diligence,” Jay Scanlan, et al., Accenture.

This report explores exactly that: how, using technology, firms can expand due diligence beyond risk assessment to make it a springboard for creating value.

“There are several kinds of trend,” Grant McCracken, Tailwind Radar. The cultural anthropologist offers a categorization of trends that can be adopted to the analysis of industries and the investment ecosystem itself.

“Increasing Your Hit Rate with LPs,” John-Austin Saviano, High Country Advisors.

Understanding who you are selling to, what they want, and how they will view your offering can help focus your efforts. Marrying that initial understanding with substantial preparation will increase your likelihood of success and the overall speed of your fundraise.

“AI and the Mag 7,” Daniel Rasmussen, Verdad.

Now that they are mega-cap behemoths run by mega-billionaires trying to outspend each other, maybe the Mag 7 will be outmaneuvered by their true heirs, another group of as-yet-unknown young innovators who are toiling away all over the world in garages.

“Founder Ownership Report,” Peter Walker and Kevin Dowd, Carta. How the typical composition of founding startup teams is changing and how equity is split.

“Private Equity Firms Are Finding New Ways to Curb Creditor Power,” Giulia Morpurgo, et al., Bloomberg.

The fight over such provisions marks the latest salvo in a power struggle between buyout firms and debt investors.

“Imbalance Sheet: Supply, Demand, and S&P 500 Financing,” D. E. Shaw. On “an unusual, and unusually persistent, anomaly.”

“RIAs fear broaching ESG topics with clients amid blowback, but ‘do-the-right-thing’ investments are still big business, Cerulli shows,” Brooke Southall. RIABiz.

RIAs and investors are walking on eggshells around each other when it comes to discussing ESG investing amid political and financial scrutiny.

To say the least

“People have complicated utility functions.” — Cass Sunstein.

Flashback: Valuing revenues

We are within a few weeks of the 25th anniversary of the peak of the internet bubble. Here’s the chart of Sun Microsystems for the ten years surrounding that time:

After the fall, Sun’s CEO, Scott McNealy, uttered these famous words:

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

Fast forward to now. Palantir is trading at 70 times projected revenues.

Postings

Search the archives for lots of great evergreen content. The very first posting, in October 2021, was “A Case Study in Three Dimensions of Asset Manager Practice,” regarding ARK Investments:

These considerations — the role of experience, the structure of research activities, and the balance between firmly-held beliefs and the openness to other voices — are by no means limited to ARK; they should be of concern for every asset manager (and, therefore, for those who allocate capital to them).

The firm’s flagship strategy started its steep descent three weeks later.

Thank you for reading. Many happy total returns.

Published: February 17, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.