The most recent Investment Ecosystem essay is “Analyzing the Due Diligence Process to Produce Better Outcomes.” It covers a novel piece of academic research about venture capital due diligence, as well as some questions about general diligence practice that are prompted by it.

Also new are five short postings on LinkedIn about core concepts for evaluating investment organizations. They concern categorization, performance expectations, differentiation, edge, and circle of competence. There are six more to come.

Reminder: If you don’t receive email versions of postings like this one, you can subscribe here. Now, on to the readings.

The pedestal of popularity

The latest piece from Howard Marks of Oaktree is titled “On Bubble Watch,” published a quarter century to the day since “the first memo that brought a response from readers,” bubble.com.

He offers a good overview of bubbles and their characteristics: newness, “no price too high,” but also no history on which to rely. Some of his points:

There’s usually a grain of truth that underlies every mania and bubble. It just gets taken too far.

When something is on the pedestal of popularity, the risk of a decline is high.

In bubbles, investors treat the leading companies — and pay for their stocks — as though the firms are sure to remain leaders for decades.

Elsewhere, in response to “a raging bitoin bubble,” Owen Lamont of Acadian offers “seven phrases of timeless relevance” with historical perspectives and references.

Another juggernaut on the bubble watch list is AI. Doug O’Laughlin, who writes Fabricated Knowledge, explores the nature of capital cycles and the implications for AI. Right now “it’s time for capital to chase the land grab blindly.”

Analyst angst

Bloomberg published an article on “How Analyst Job Cuts on Wall Street Are Reshaping Equity Research.” To wit:

Regulations on how banks charge for research, a shrinking market for publicly listed companies, and the popularity of index-tracking funds have conspired to squeeze equity research in ways few could have imagined even a decade ago. Leaps in artificial intelligence only threaten to accelerate that trend, with firms like JPMorgan already experimenting with AI-powered analyst chatbots, sowing deeper doubts about the value of fundamental analysis and whether investors will keep paying for it.

The article delves into the implications of the changes for analysts and for market behavior. A column by Matt Levine elaborates.

Also of note: “The Lamentation of David Einhorn,” by Robin Wigglesworth for the Financial Times, on the ripple effects of the massive flows to passive investing and other strategies that have changed the game “for people who are trying to buy undervalued things.”

Blowing in the political winds

This chart comes from a Wall Street Journal article by Sarah Nassauer. It shows the abrupt rise of DEI as a topic during corporate conference calls and presentations starting in mid-2020 — and the marked decline from the peak.

The shape of the histogram is indicative of a broader pattern in corporate behavior. Many companies are fleeing memberships in the net-zero initiatives that they previously embraced and ridding themselves of or deemphasizing broader ESG efforts. Some leaders who were publicly critical of the January 6 attack on the Capital and other actions during the first Trump term are now providing funding for his second inauguration and changing (or hiding) corporate policies to curry favor.

Those aren’t universal trends, of course. For example, the WSJ article cited above covers Costco’s reaction to a shareholder proposal regarding its diversity stance.

You might think that the reversals in response to changing political winds are terrible or you might herald them as refreshing returns to sensibility — or you might see the ebb and flow of such things as a vivid demonstration of craven decision making and wonder what that indicates about the firms and their leaders.

New sources

The last twenty years have seen an explosion of investment writing online, and there are always new sources popping up to try out. Three recent debuts that may be of interest to you:

Jeffrey Ptak is the Chief Ratings Officer for Morningstar Research Services. He writes about interesting ideas in the fund world at Basis Pointing.

An investment funds lawyer publishes Cash and Carried, which offers straightforward explanations of the nuts and bolts of investment products and the entities that produce and invest in them.

It is hard to keep abreast of the flood of academic writing about investments. One way to do so is by reading Alpha in Academia.

Public funds

A team of researchers from Marquette University has published a paper, “Does the Board Engagement of Public Pension Plans Matter?” in the Journal of Financial Research. (Christopher Merker, one of the authors, offers background on the project with links to additional material.) Their approach:

We collect data [from publicly available meeting minutes] that reflects board engagement levels, including meeting frequency, the extent of investment discussions, attendance rates, and member turnover, among other factors. From this novel database we create an index which captures the extent of board engagement.

The bottom line: funds with higher index scores have better performance.

Given the size of unfunded liabilities at many public plans and the myriad ways political considerations can enter into decision making, it’s not surprising that market crises bring increased attention. What may be surprising is that “on average, about 8 percent of state pension plans are under SEC investigation each year.” Kangkang Zhang analyzed the effects of those investigations.

Also see: “Pension funds dabble in crypto after massive bitcoin rally.”

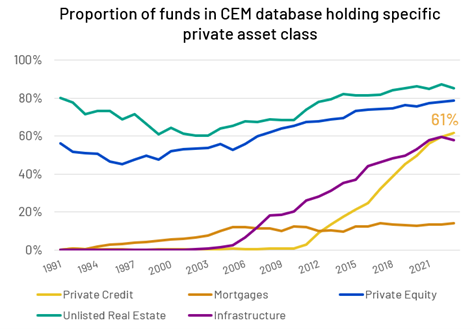

Changing menu

CEM Benchmarking analyzes the holdings, costs, and performance of large pension and sovereign wealth funds around the world. A posting from it about private credit includes this chart, showing the rapid adoption of that asset class as an asset allocation “bucket” over the last fifteen years.

Other reads

“The Who and How of Hedge Fund Risk Shifting,” Spencer Andrews and Salil Gadgil, Office of Financial Research.

Our findings illustrate that compensation considerations distort managers’ portfolio allocation decisions.

“Beyond the Blame Game: Why the Proxy System Needs to Change,” Matthew Leatherman and Olivier Lebleu, FCLTGlobal. A call for reform, including sections on “costs to be minimized” and “value to be maximized.”

“The ‘Positives’ Section of a Due Diligence Report,” Anthony Hagan, Freedomization.

There are ways to portray conviction without putting out foolproof “best-thing-since-sliced-bread” vibes. There is an art to highlighting positive attributes in an objectively convincing manner without sounding like you work for the fund (or deal) you are putting forth.

“This is What a Good Investment Meeting Should Look Like,” Jeffrey Bronchick, Cove Street Capital. Unfortunately, many potential clients who want to sit in on an investment meeting of an asset manager are looking for theater when they should be looking for the messiness that is inherent in good teamwork and decision making.

“The Accuracy and Importance of Growth Guidance,” Naoki Ito, Verdad.

Our favorite motto is that investing is not a game of analysis; it’s a game of meta-analysis. Stock prices already reflect growth projections. In our opinion, what drives returns is the deviation between projected growth and realized growth.

“What You Don’t Know Could Sting Your Portfolio,” Jason Zweig, Wall Street Journal. When custodian firms demand more revenue from investment advisors, clients can end up paying the price.

“The problem with marketing puffery,” Seth Godin, Seth’s Blog.

If you need to out-hype your competition, it’s a race to the bottom. Someone is always more willing to hype than you are.

Step right up

“The large print giveth and the small print taketh away.” — Tom Waits.

Flashback: The pits

They say a picture is worth a thousand words. Two pictures can tell a story.

To illustrate a LinkedIn posting arguing that “an AI Tsunami is coming this year in marketing,” Nick Candler posted this diptych:

It is a reminder of how profoundly the structures on which an ecosystem is built can change over time. The trading pits and stock exchanges were the beating heart of the financial system. No more.

It is a reminder of how profoundly the structures on which an ecosystem is built can change over time. The trading pits and stock exchanges were the beating heart of the financial system. No more.

To be in the room when there was market-moving news was to see and hear the world of money move.

Postings

All of the postings (now over two hundred) are available in the archives.

For example, this is from a piece from three years ago, “Capital Market Assumptions as Explored Beliefs”:

Whether home-grown or off-the-shelf or something in between, the CMAs are an expression of beliefs. As such, in draft form they should serve as a vehicle for a discussion of those beliefs, the proposed choices, and the implications of them — well before the CMAs are adopted and implemented.

Thank you for reading. Many happy total returns.

Published: January 20, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.