The next essay to be published will be “Does it Matter (How the Money is Made)?” It will delve into questions about whether and how asset owners should consider the business models and practices behind the returns that they receive — or just focus on maximizing those returns.

Until then, here’s a fresh crop of interesting reads.

Hedge funds

Multi-manager, multi-strategy hedge funds — commonly known as pod shops — have been all the rage. A report from Acadian poses a question: “The Systematic Multi-Strategy Hedge Fund: A Better Alternative?”

The report lays out the advantages of pod shops, including avoiding the hassles of selecting, sizing, and evaluating a roster of hedge funds on your own; better capital and operating efficiencies; fee netting; improved diversification; and advantages in risk management. The big negatives are the difficulty of getting access; “opacity and information asymmetry;” and cost pressures as the talent war continues to escalate. (Pass-through fees “have become the norm,” often leading to the bulk of returns flowing not to the asset owner but to the manager of the hedge fund and those expensive pods).

Not surprisingly, since it is a systematic asset manager, Acadian goes on to stress the benefits of a multi-strategy approach offered in a systematic fashion. The firm argues that such a strategy leads to reduced cost pressures; a better alignment between the manager and investors; increased transparency; and improved risk management and liquidity.

Elsewhere:

In a new posting, Rupak Ghose draws an analogy to an earlier time:

The implosion of Man Group is ancient history now but there are timeless lessons. Highly leveraged funds. Investors looking for uncorrelated returns. Products that are dependent on the low correlation between the components. The continuous search for new capacity.

Francois Lhabitant released a paper, “Ten Common Mistakes Investors Make When Allocating to Hedge Funds (or how to make sure your hedge fund portfolio will disappoint).” Among those mistakes:

~ Using hedge fund indices to guide strategic decisions.

~ Choosing high Sharpe ratio funds and expecting a high Sharpe ratio combination.

~ Overdiversifying.

~ Applying pie-chart thinking to complex allocation problems.

Private credit

Barely on the radar of most investors a decade ago, private credit has become a juggernaut. Some readings:

~ “The next era of private credit.” McKinsey outlines how this still-young area is evolving across a range of different strategies and partnerships.

~ “Private Credit’s Shifting Identity.” Steven Kelly’s Without Warning cautions, “It has slowly begun undermining most of its original value propositions.”

~ “The Rise of PIK: A Double-Edged Sword for Private Credit.” On the CAIA blog, Vincent Weber comments on “the increasing use of Payment-in-Kind (PIK) financing” in private credit.

~ “Private debt misconceptions.” Stepstone defends the asset class against five misconceptions about it.

Being long-term

FCLTGlobal released lists of questions about what it means to be “long-term.” These “gold standards” touch on governance, incentives, engagement and dialogue, and metrics, with separate questions for asset owners, asset managers, and companies. While the lists are shorter than you might expect, the questions in each can serve as a good starting point for discussions about what it means to be truly long-term and whether actions match up with intent in that regard.

Skill and returns

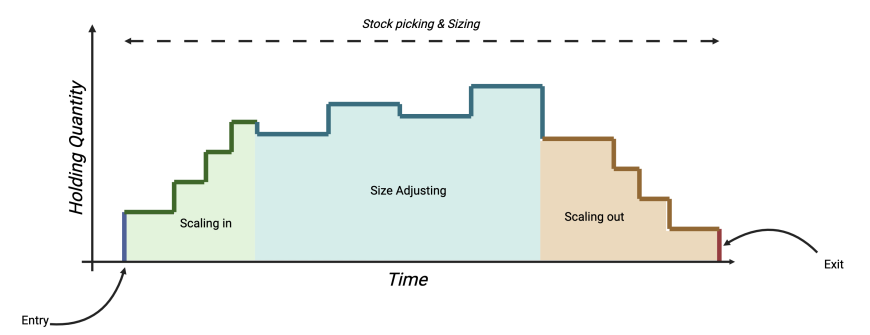

The last edition of the Fortnightly featured a paper about excess return profiles of active equity managers that used monthly data across a broad spectrum of managers. It echoed work done by Essentia Analytics, which is hired by asset managers to analyze portfolio decision making using real-time data. (An accumulation of Essentia white papers on portfolio manager decision patterns can be found here.)

Three members of the Essentia team just released a new study, “Actions Speak Louder Than (Past) Performance: The Relationship Between Professional Investors’ Decision-Making Skill and Portfolio Returns.” According to it, professional investors face a “combination of a complex ecosystem, limited cognitive resources, and time constraints,” causing them to lose advantages that they have over others and “often displaying the same overconfidence and errors as non-experts.” The authors introduce a measure they call the Behavioral Alpha Score, which they link to subsequent portfolio performance.

The image above was chosen from the paper because it clearly shows specific decisions to add, subtract, or hold shares of a position over time. This often gets lost in evaluations based upon the weight of a security within a portfolio, which is affected by other factors in addition to those specific decisions. Incorporating a graph like this with one depicting the portfolio weight paints a much clearer picture of decision making.

Making a pitch

When you want to get your ideas across, what’s the best way to do it? Where would you want to be on a spectrum from “like everyone else” to “totally unique”? Most investment communication can be found in a “like everyone else” pile.

The bottom line of some research regarding pitches to angel investors is that they work best when “the narrative is familiar but not too familiar.” So a good formula might be stated as “familiarity plus differentiation” — following convention to a certain point in order to orient the audience but moving them beyond that in order to show them that you are not just like everyone else.

(FYI, the Investment Ecosystem provides evaluation and training for organizations and professionals in regards to effective communication — among coworkers and to clients and prospects.)

Other reads

“The Operator’s Dictionary,” Permanent Equity. A wonderful “guide to terms, ideas, and phrases — annotated with notes, nuance, and nit-picking,” for operating businesses and organizations of all kinds.

“Prisoner’s Dilemma and Private Equity Pacing,” Christopher Schelling, LinkedIn.

Collectively, the individually rational response to committing greater and greater amounts of capital may have resulted in the industry as a whole becoming substantially overcapitalized.

“Todd Combs Retrospective?” Old Rope. With ongoing interest in what a post-Buffett Berkshire will look like, this piece considers one of the key players, including “questionable decisions” by him at GEICO, as well as other potential issues.

“The Noise Factory,” Joe Wiggins, Behavioural Investment.

For any issue or event, we should ask two questions: Does it matter? Is it knowable?

“Just do it! Brand Name Lessons from Nike’s Troubles!” Aswath Damodaran, Musings on Markets. On valuing brands, using Nike as an example, where the “new CEO has his work cut out for him!”

“Factor Premiums: An Eternal Feature of Financial Markets,” Guido Baltussen and Bart van Vliet, Enterprising Investor.

Factor premiums are an eternal feature in financial markets. They are not artifacts of researchers’ efforts or specific economic conditions but have existed since the inception of financial markets, persisting for more than 150 years.

“Culture Club: CalPERS puts people first in talent reboot under new CIO,” Sarah Rundell, Top1000Funds. Early changes by new CIO Stephen Gilmore.

“Broad Strategic Allocation,” AQR.

In our experience, the most insightful SAA analyses are those with thoughtfully constructed constraints or anchors that define a reasonable territory within which the investor is able to address their specific portfolio problem.

“Are Institutional Investors Meeting Their Goals? Spotlight on Earnings Objectives,” Richard Ennis, Enterprising Investor. A look at how asset owners have done relative to their stated goals since the financial crisis.

“GP Fundraising Trends in 2024 — Does Performance Attract Capital?” David Dawkins, Preqin.

Consistent performance, rather than eye-catching outperformance, has been the foundation of fundraising success for a number of the biggest and most notable funds.

“Visual Matters: Visual Deception in Financial Markets,” Jiali Gao, SSRN. Does the auto-scaling of charts on investment terminals mislead investors “in interpreting trading information and assessing risks”?

Achievement reveals

“Some people grow and some people swell.” — John Weinberg, senior partner at Goldman Sachs from 1976 to 1990, quoted in Robert Rubin’s book, The Yellow Pad.

Flashback: Adam Smith, behavioral economist

“Adam Smith, Behavioral Economist” was published in the Journal of Economic Perspectives in 2005. A question mark was added to the end of that title for a short Harvard Business School interview with Nava Ashraf, one of the authors. Of Smith’s The Theory of Moral Sentiments, she said that:

The field of behavioral economics, which economists usually think of as a “new” field, was in fact rigorously studying the very factors that Smith, arguably the “father” of modern-day economics, had always thought were critical in human behavior and interaction.

The struggle between “passions” and “the impartial spectator” that Smith referenced is ongoing — and now much discussed, albeit using different words — centuries after Smith wrote about it.

Postings

Check out the categories of postings in the archives that are of particular interest to you.

A very early piece, “Mass Customization and Tactical Asset Allocation,” reviews a paper about “the dance between theory and practice, as well as the push and pull in the industry between customization and industrialization.” Among the observations about the paper:

Another point of interest comes from a sentence which was quoted earlier: “Creating a viable industrial TAA process is thus part of the asset manager’s fiduciary duty towards all its clients.” In a business of scale, the need for “industrial” activities is very real, but there are trade-offs. Some might argue that industrialization is largely for the benefit of providers rather than clients (resulting in improved margins and allowing for even more scale).

And, while firms need to do what they say they do — and to act in their clients’ best interests — having an “industrial TAA process” is not a necessary element of fiduciary duty.

Thanks for reading. Many happy total returns.

Published: October 14, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.