Jason Zweig’s book, The Devil’s Financial Dictionary, is the subject of the latest Investment Ecosystem posting. (Subscribe here to see all of the content as it is released.) It is an unusual and fun look at the lexicon of the investment business:

Zweig provides a mix of history, etymology, and satire that takes the book well beyond the typical dictionary. Skepticism about the language and practices of the investment world is essential for lay investors and professionals alike — and the recurring abuses and calamities of the investment industry come in for deserved cynicism.

On to the readings.

Social investing (A)

In a recent paper, J. Anthony Cookson, et al. provide a review of research into the interplay of social media and investing, “distinguishing between research using social media as a lens to shed light on more general financial behavior and research exploring the effects of social media on financial markets.” The quantity of papers cited is impressive, showing that the topics have received a lot of academic attention, and a number of important areas of study are covered.

To pick one, how does the “abundant but noisy” content that flows from “non-experts” affect the network structure of information and the behavior of investors (and investments)?

Rather than traditional media editors determining which stories are featured, thus receiving the most attention, social media attention is driven by popularity, often mediated via algorithms. In turn, this enhances the scope for information cascades and for coordinated sentiment to influence markets.

Social media amplifies human predispositions while introducing new effects:

Is investors’ propensity to place themselves into a financial echo chamber a natural tendency that would exist to the same extent irrespective of social media interactions, or do features of these platforms exacerbate echo chamber behaviors? In reality, social media both shapes us and reflects fundamental aspects of ourselves.

Social investing (B)

Another kind of social investing is the subject of research by Hoa Briscoe-Tran. et al. They examine the “S” in ESG, challenging “the common ESG investing approach of amalgamating factors without considering their distinct, potentially contradictory, risk and return implications.”

The study focuses on the MSCI ESG ratings, in which the social category has “two primary components: the human capital score and the product safety score.” However:

The expected impact of a firm’s social ratings on its future stock returns varies depending on whether the ratings pertain to human capital or product safety.

The two scores have opposite effects:

This divergence questions the practice of combining varied ESG factors into a single score, which can mask the distinct risk and return implications of each component. Our findings underscore the complexity and diversity within ESG factors, particularly the social dimension, advising investors and practitioners to consider ESG criteria’s individual aspects in investment decisions.

Active, passive, and magnificent

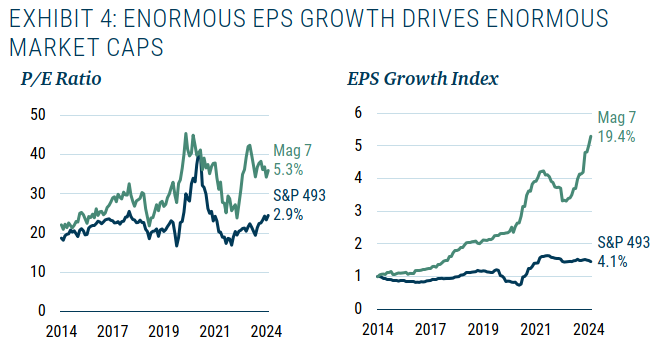

The latest quarterly letter from Ben Inker and John Pease of GMO includes the above exhibit, showing on the left that the annual growth of the multiple on the Magnificent Seven has outpaced the rest of the market, but that the real story is on the right:

The primary driver of the enormous market caps of the Magnificent Seven (Spectacular Six? Fabulous Five?) is — drum roll — the enormity of their EPS growth.

But those stalwarts aren’t the main course in the piece, which is titled “FAQ: Passive Investing.” Regarding the headline topic, the authors summarized the difficulty of divining the impact of the increase in passive investing:

The problem has instead come from the dilemma of wanting to say fairly definitive things about the impact of passive investing on the stock market when it is exceedingly difficult to make conclusive statements about the effect of a single market change in an environment in which many other things have also changed over the same basic time scale.

Among the topics discussed are the differences in scale economics for active and passive funds; how the effects from the growth in passive depend on which investors are making the switch to it; and the different incentives for plan sponsors managing defined contribution plans versus defined benefit ones. Of note, although markets have changed a lot in the last few years, most multi-asset portfolios look a lot like they did before:

This suggests that the elasticity (read: price sensitivity) of multi-asset investors isn’t particularly high. Some of this is due to tight benchmark constraints, some of it is just inertia.

The bottom line:

The reality, then, is not so much that the rise of passive investing ruins markets, but only that it changes them. It changes how much short-term investors should care about flows. It potentially changes how much long-term investors should bank on mean reversion. It changes how all investors should think about correlations, seeing as both passive flows and passive allocations might mechanically introduce (or reinforce) sources of asset co-movement.

Morningstar conference

A pair of columns in the latest Mutual Fund Observer include perspectives on the Morningstar Investment Conference. The first item in David Snowball’s ten takeaways notes that “it’s not a conference for investors anymore”:

It might simply be a healthy evolution that financial planners are spending less time on things that are hard and iffy (selecting up-and-coming managers) and more time learning about “winning the next generation of high-net-worth investors.”

He also mentioned that Morningstar waived the admission fee for advisors who would attend three sponsored sessions — and gave a description of the exhibitor hall that made it sound moribund. (Many conference organizers are wondering how to reinvigorate their previous models in a post-pandemic world.)

Charles Boccadoro provided an in-depth review, including lists of hot and not-so-hot topics. Among other things, he said a panel “expressed an almost nostalgic desire for more in-depth articles with less click-bait titles, but also the recognition that this desire is at odds with today’s media business model.” That is telling, since many of Morningstar’s own web offerings are fronted with click-bait titles in a way that they didn’t used to be.

Commercial real estate

Since 2005, Tadas Viskanta has been the go-to source for the daily curation of investment reads. One recent set of links included three articles on commercial real estate that provided a good summary of the state of the market and the actions of the big investors most exposed to it:

“Fearing Losses, Banks Are Quietly Dumping Real Estate Loans” (New York Times).

“Real Estate Bets Gone Wrong Roil $1.24 Trillion Canadian Funds” (Bloomberg).

“Property group boss likens UK office values to ‘melting ice cubes’ ” (Financial Times).

Generating commentary

Perhaps the only thing worse than having to read portfolio attribution summaries period after period is having to write them. Don’t fret, a machine will take care of it for you. For example, clicking “generate commentary” in this FactSet application will spit out the copy. But is it as good at painting things in a favorable light?

Other reads

“The Last 72 Hours of Archegos,” Ava Benny-Morrison and Sridhar Natarajan, Bloomberg.

Weeks of testimony have exposed cringeworthy misjudgments and costly blunders in various camps throughout the crisis — hardly Wall Street’s preferred image of calculated risk-taking. Bankers, for example, painfully acknowledged how they relied on sometimes-vague or evasive trust-me’s from Archegos while doling out billions in firepower for Hwang’s bets. That confidence melted into confusion . . .

“Hedge Funds: A Poor Choice for Most Long-Term Investors?” Richard Ennis, Enterprising Investor. On balance, they are “alpha-negative and beta-light” and investors mute the performance of the best ones by over-diversifying.

“Optimization and Evolutionary Dead Ends,” Christopher Schelling, LinkedIn.

An optimization is quite literally best fit to one environment — that’s what it means. But when environmental conditions are not as expected, optimization is what creates fragility.

“Balancing Innovation & Control,” Capco. An accumulation of articles regarding governance issues, primarily in the areas of technology and sustainability.

“Elephants in the Investment Committee Boardroom,” True North Institute. Among ten top-of-mind issues for asset owners:

1) The long-term prospects for private equity

2) Artificial Intelligence: investment opportunities and the impact on our investment process

3) Illiquidity management: managing PE capital call cash requirements as distributions dry up

4) Alpha from public equities: active vs passive debate

5) Rethink our ESG Policy (making it more practical)

“Broyhill Book Club 2024,” Broyhill Asset Management. This year’s compilation, with links to previous editions.

“BlackRock throws support behind effort to move pensions beyond ESG,” Lee Harris and Brooke Masters, Financial Times. Regarding the Alliance for Prosperity and a Secure Retirement; Tim Hill, a retired Phoenix firefighter who is president of the alliance is quoted as saying:

We are not pro-ESG. We are not anti-ESG. What we are is ‘pro’ letting investment professionals, who have a fiduciary duty to their beneficiaries, do the work that they’re supposed to do. We are ‘anti’ politicians, from either the right or left, interfering with that fiduciary duty so they can carry out a political, social agenda.

What room are you in?

“If you’re the smartest person in the room, then you’re in the wrong room.” — Richard Feynman.

Flashback: Ray DeVoe

In the days when research reports were found on paper rather than pixels, you could walk into a portfolio manager’s or analyst’s office and see whose work was getting their attention (although most noticeable were the large stacks of unread research piled around).

You might very well see “The DeVoe Report” from the firm of Legg Mason Wood Walker. Ray DeVoe was an old-school analyst who was unafraid to point out the follies of the business. His 2014 Bloomberg obituary cited two phrases for which he became famous (each of which is referenced in Zweig’s The Devil’s Financial Dictionary). He originated the term “dead cat bounce,” and Warren Buffett among countless others has quoted his maxim, “More money has been lost reaching for yield than at the point of a gun.”

Postings

Check out the archives to find earlier editions of the Fortnightly and original essays that target the important problems faced by investment organizations and professionals.

For example, in 2023, proposed rules for investment advisors from the SEC prompted a posting, “The Outsourcing Debate: Principles and Rules”:

While the proposed SEC rule is getting the attention, the general questions behind it are what’s most important. How good are advisory firms at assessing the trade-offs — for their clients, not themselves — of the range of outsourced services that they are employing? How well can they judge the quality of those providers? Does their own circle of competence qualify them to evaluate that of others?

Organizations should want to get better at all of this, whether the rule forces them to do so or not.

Thank you for reading. Many happy total returns.

Published: July 8, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.