The next essay on the Investment Ecosystem is tentatively titled “The Active Management Reinvention Project.” (Sign up to receive all postings via email as they are published.)

On to the latest crop of readings.

Selection algos

A pair of briefs from Addepar written by Dane Rook and Dan Golosovker address the manager selection process. The first, “What’s Your Algo for Manager Selection . . . and How Good Is It?” says:

An investor’s processes for manager selection can materially impact their portfolio-level returns. However, many investors struggle to think analytically about their selection processes and do not know objectively how good those processes are or how to improve them.

The briefs specifically address the evaluation of managers in private markets, but the ideas apply equally to public mandates. The “false temptation of past performance” is the big problem; the authors instead want to identify the “deeper drivers of performance that can function as high-confidence signals of future results.” But most selection processes fail the tests of a good algorithm; furthermore:

Many investors’ selection algos aren’t codified anywhere, which not only limits their consistency, accuracy and efficiency, but also reduces their amenability to “debugging.”

In practice, investors have “an unfortunate satisficing tendency”:

They often focus their deep diligence on what information is offered to them by prospective managers, rather than demanding the information that matters most.

The theoretical characteristics and steps to be taken are fleshed out — and augmented by the second brief, “The ‘Algorithmic’ Mindset for Selecting Best-Fit Manager in Private Markets.” A footnote speaks to the title:

We emphasize “best-fit” managers, because the managers that deliver the best returns might not be the managers who are the most appropriate [for the] investor: there is also a need to factor in alignment, contribution to portfolio-level diversification and risk management, and various other relevant properties.

(The critical “deep diligence” phase referenced by the authors is at the heart of the Advanced Due Diligence and Manager Selection course. Also of note: Many of the shortcomings mentioned in terms of the imprecision of selection algorithms also apply to the investment processes of fundamentally-driven asset managers.)

Better deals

Emily Holdman of Permanent Equity, a firm that manages multi-decade private equity funds, wrote a report called “Better Deals.” In a series of short and interesting chapters, it examines the dynamics of negotiation and the behavioral tendencies that come into play — and serves as a cultural yardstick for a broader range of investment management deal making.

The final section is “Ask All the Questions: Overcommunicate and Don’t Assume Anything.” It includes:

People sometimes limit their inquiries to avoid appearing ignorant or difficult. This is exactly the kind of self-sabotage that leads to poor outcomes.

Questions are a cornerstone of real relationships (along with listening). Interest in the other party is healthy, not intrusive. Dialogue develops mutual understanding. Which can lead to trust. Which, ultimately, results in better deals.

In parts of the ecosystem without a multi-decade time horizon, the pace is more frenetic and (it seems) the actions more cutthroat, but the advice still applies.

A shared interest

In “A Shared Interest: Do Bonds Strengthen Equity Monitoring?” Todd Gormley and Manish Jha investigate how corporate bond holdings at asset managers affect their monitoring and voting of their equity positions. From the paper:

Investors influence governance through a combination of voice (managerial engagement and voting) and exit (selling one’s position). Lacking the ability to participate in shareholder votes, bond investors are typically not thought to play an important governance role, and commonly used measures of institutional investors’ incentive to be engaged stewards focus solely on their equity positions. However, bond investors have many reasons to be concerned about firms’ governance structures, which can influence bond values (via increased firm value), credit ratings, and the likelihood of repayment.

The authors “find evidence that institutions’ bond holdings predict their stewardship activities,” highlighting “how the determinants of institutional investor attention are more complicated than typically assumed.”

(Because firms differ structurally and culturally, the amount of information sharing across asset classes varies quite a bit from manager to manager. It would be fascinating to see how those firm-specific factors are reflected in their unique voting patterns.)

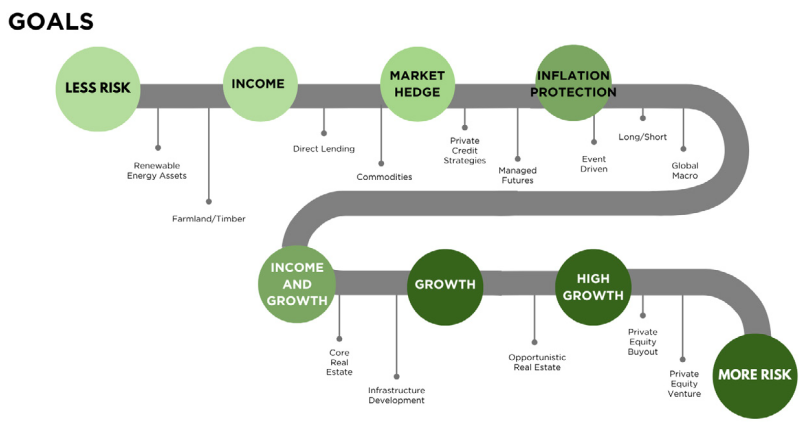

Private markets

This image comes from “Crossing the Threshold: Mapping a Journey Towards Alternative Investments in Wealth Management,” a report from CAIA Association. The stylized view could be improved with the addition of key categories of public assets, especially since the report says that one way to change perceptions about private market vehicles “is to position private markets exposure alongside public markets exposures”:

By removing the imaginary line between private and public markets, investors begin to conceptualize their allocation to “alternatives” instead as exposures that are an important part of the overall [portfolio] construction.

The challenge for an association of analysts whose credential has “alternative” in its name is to avoid the excesses of the “alts for the masses” push of product providers and to faithfully execute the fiduciary responsibilities that are the foundation of wealth management — at a time when the opportunity set is different than the one that created the historical record. It’s a tough balance between the two forces, as is evident in the text.

Another credentialing body, CFA Institute, has published “Private Markets: Governance Issues Rise to the Fore.” The report includes information from a survey of CFA Institute members, recommendations for investors and policymakers, and a section on “the end of the era of cheap money” and its implications for governance. Of particular interest is the sixth chapter, a primer on governance issues in private markets which serves as a good introduction for investment advisors and asset owners alike.

With an asterisk

There have been several articles of late about private equity managers buying positions on the secondary market (at a discount) and immediately marking them up to their last official valuation. For one, an Institutional Investor piece by Michelle Celarier examined this “sleight of hand,” legal as it is.

As mentioned there, secondaries have been a hot spot in a sluggish private equity landscape, with those markups aiding performance. Buying such exposures on the cheap can be a value-adding strategy, but the instant gains may mislead investors, who are prone to imagining repeatability and chasing returns. The numbers should be thought to come with an asterisk until those revaluations are sized and gauged as to the likelihood that they will last.

Other reads

“Six Words for a Capital Raise: ‘Slow is Smooth. Smooth is Fast.’ ” John-Austin Saviano, High Country Advisors.

Whatever the reason, an overeagerness to tell your story risks it being told badly, wasting priceless introductions, and the process becoming an awful slog. Create a generic deck, run unstructured meetings, and give meandering answers and you’ll find yourself pushing on a string.

“Market efficiency and value added by listed and unlisted U.S. institutional investor real estate portfolios,” Alexander Beath and Maaike van Bragt, CEM Benchmarking. A 24-year study, including the “proportions of investors outperforming by year and the implied probability that investors have skill in alpha generation.”

“How Do Public Pension Plan Returns Compare to Simple Index Investing?” Center for Retirement Research.

Over the full period [2000-2023], plan returns are virtually identical to the simple index strategy, but plans have done much worse since the Global Financial Crisis.

“A tl;dr for annual reports: same is good, change is bad,” Bryce Elder, Financial Times. Two studies of the language of corporate filings.

“Betting with a Weak Hand,” Joe Wiggins, Behavioural Investment. On poker and investing:

We are not sure what a strong hand is.

We will misjudge when we have a strong hand.

We will play too many hands.

“Janus Henderson’s Ali Dibadj: ‘You’ve just got to roll with the punches’,” Brooke Masters, Financial Times. The challenges of managing a large asset manager that resulted from the merger of disparate firms.

“Seven Questions About Proxy Advisors,” David Larcker and Brian Tayan, Stanford Business.

The proxy advisory industry is marked by considerable controversy regarding its purpose, influence, value, and objectivity.

“Nvidia to get 20% weighting and billions in investor demand, while Apple demoted in major tech fund,” Jesse Pound, CNBC. The unexpected effects of an “index” rule.

“Dilemma on Wall Street: Short-Term Gain or Climate Benefit?” Lydia DePillis, New York Times. (Note: This topic will be the subject of an upcoming Investment Ecosystem essay.)

Portfolio managers have conflicting incentives as the economic and financial risks from climate change become more apparent but remain imprecise.

“The Cultures that Actually Win,” Gapingvoid. Charlie Munger and Amish barn raising; “trust is everything.”

The key question

“Why are we doing it this way?” — William Donaldson, a founder of DLJ; his NYT obituary said he thought it was “a question that can be asked about everything.”

Flashback: The Five Percent Club

A 2023 article in the StarTribune answered the headline question: “Minnesota was once a leader in corporate philanthropy. Is that still true?” The backstory:

Nearly five decades ago, the Five Percent Club put the state on the map nationally as a leader in philanthropy. Target and 22 other Minnesota companies vowed to give away 5% of their pre-tax earnings to charity — the first group of its kind in the nation.

Actually, it wasn’t called Target at the time; the discounter was part of Dayton Hudson then, and the pledge was at the parent level. The Club got its name because the firms “gave 5% of their earnings before taxes back to the community.” Today, the members of the broader Keystone Program give at least 2%, with half reaching the 5% level.

The “shareholder value” movement kicked in around the time of the formation of the Five Percent Club — and the debate between the two ways of thinking continues today.

Postings

The archives include all of the previous editions of the Fortnightly. For example, “Becoming a Learning Organization” taps observations from the CIA (like the one below) and applies them to investment organizations:

Institutional learning from those directly involved in events can provide context for situations of the future. As time passes, people move on, memories fade, and important lessons are lost — or misremembered. After-action reports of significant events can illuminate investment dilemmas of the future and, perhaps more importantly — if objectivity versus blame drives the culture and interviews are conducted with that intent — the social and psychological factors that affected those involved.

Thank you for reading. Many happy total returns.

Published: June 24, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.