No matter your particular taste in music, you are likely to have an interest in the most recent posting on the site, “The Music of Investment Genres and Processes.” The analogies offered will help you think about industry practices (and communicate with others about them).

If you find these Fortnightly editions and the other essays helpful, please recommend The Investment Ecosystem to your co-workers and friends. If you’re new and want to subscribe (for free!), you may do so here.

The robots are coming here

Nathan Dong begins his paper, “Can AI Replace Stock Analysts? Evidence from Deep Learning Financial Statements,” with a screenshot of a headline from the New York Times Magazine, “The Robots are Coming for Wall Street.” (That article was published more than eight years ago.)

Using deep-learning techniques (and an inexpensive setup), Dong’s approach “outperforms human analysts in 12-month-ahead target price forecasts by a large margin.” The abstract concludes:

Overall, the results of this research support the notion that AI has the potential to replace human analysts in certain aspects of predicting financial performance.

Figuring out what the machines can do better than the humans is a point of focus these days. Target prices are low-hanging fruit. Dong suggests that the lagging forecasting performance of analysts “reflects the degree of optimism bias or the need to curry favor with companies’ management.” Another potential factor is unveiled via the research methodology: adding interest rate information was helpful in improving the performance of the AI model, but most sell-side analysts don’t pay much attention to it. Plus, target prices are promotional devices for selling ideas — and analysts can sometimes get into leapfrogging games to have their targets stand out from others. Using information available to all, the machine outperforms by removing longstanding behavioral distortions that are an accepted part of assigning target prices.

Another paper, “Financial Statement Analysis with Large Language Models,” by Alex Kim, et al., includes this conclusion:

Even without any narrative or industry-specific information, the LLM outperforms financial analysts in its ability to predict earnings changes. The LLM exhibits a relative advantage over human analysts in situations when the analysts tend to struggle.

Much more to come.

Embrace the mania?

A report by Que Nguyen of Research Affiliates counsels readers to “Learn from Last Tech Bubble to Embrace GenAI Mania.” It provides some history of the dot-com period, performance comparisons of a few notable companies of that era, and favorable words for the economic progress that comes from manias “despite the misallocation of much capital.” As far as investing lessons:

Those who invested in profitable, well-capitalized tech companies in 1996 fared well over the long term. Those who piled into speculative companies at the height of the mania while eschewing “old economy” stocks often experienced significant losses.

For the current case:

If investors believe that GenAI will be as impactful as the internet, they will need to participate by getting invested, and the best approach will be to stay diversified and be prepared to hold through ups and downs.

John Rekenthaler of Morningstar also compared today’s environment with the dot-com era, coming to a different conclusion, that “with internet stocks, most of the industry’s future leaders arrived not with the first wave of technology, but the second.”

In “The Alpha Cycle,” Joe Wiggins opens with a cautious reminder:

{kind=link}

Industries in which capital has become abundant and optimism unbridled often end up disappointing investors.

And, in the process, the “intoxicating mix of unusually strong performance and seemingly irrefutable narratives draws increasingly large flows” to the asset managers who most embrace the mania, setting up a classic error in manager selection:

Selecting active fund managers who have enjoyed prodigious tailwinds comes with twin challenges. First, we are likely to grossly overstate the presence of skill (we cannot help but conflate performance with skill). Second, even if they do possess an edge, it is unlikely to matter because the odds of investing successfully in an area that already has stretched valuations and delivered exceptional performance are poor.

Real estate questions

Two property funds — Blackstone Real Estate Income Trust (BREIT) and Starwood Real Estate Investment Trust (SREIT) — continue to raise eyebrows among market watchers, while their sponsors try to convince investors that the bottom is nigh. Cash flows fell below dividends in 2023 and each fund has had redemption requests exceed stated caps at times. The monthly limit for withdrawals for SREIT was just slashed, with this explanation:

[As] a fiduciary to our stockholders, we cannot recommend being an aggressive seller of real estate assets today given what we believe to be a near-bottom market with limited transaction volumes, and our belief that the real estate markets will improve.

Two articles focus on the uncertainties around BREIT, which is significantly larger than SREIT. The New York Times gives a short synopsis of the issues, while a subheading on a much longer piece from Business Insider wonders whether BREIT is a house of cards.

The essential question is shrouded in fog, since no one knows what the properties in the portfolios are worth. That means that there are potential issues regarding the fairness of prices for incoming and outgoing investors (and for the fees based on net asset value). With the increased popularity of semi-liquid alternative investments, these concerns are bound to be an area of attention for quite some time.

Endowment performance

True North Institute published the first report in a promised “performance ranking series,” this one focused on large U.S. university endowments. The four conclusions:

Outperformance or alpha is becoming more difficult to generate for even the most capable of institutional investors.

Total portfolio absolute returns are primarily driven by the overall risk budget of the portfolio including large allocations to illiquid asset classes — primarily comprising private equity.

It is not clear that the large endowments are outperforming the average private equity and venture capital investor. High allocations to private equity do not necessarily translate into high overall portfolio alpha.

We do not assume that private equity and venture capital will deliver the same level or consistency of returns in the future. Endowments with more diversified sources of illiquidity premium may outperform in the future.

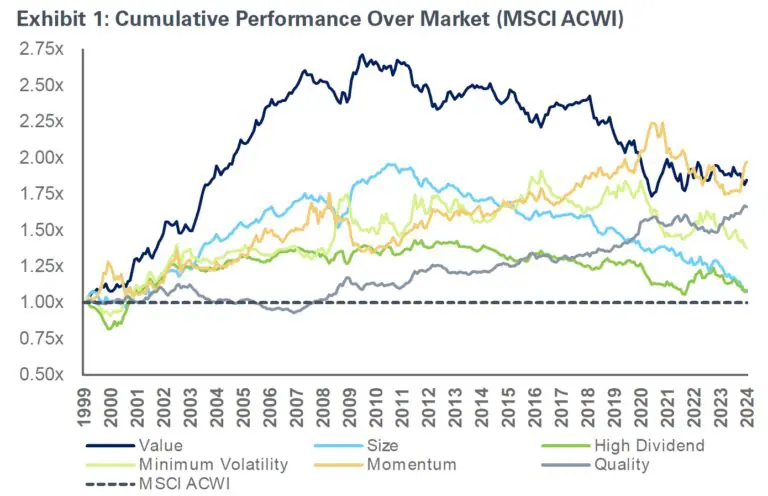

Faltering factors  This image is from “A Guide to Factor Investing,” by Alex Goroshko of NEPC. It aptly demonstrates the quandary of the day: The two factors, size and value, that were thought to be the most reliable (and which became the backbone of many investment strategies) peaked in performance around the time when factor investing dramatically increased in popularity.

This image is from “A Guide to Factor Investing,” by Alex Goroshko of NEPC. It aptly demonstrates the quandary of the day: The two factors, size and value, that were thought to be the most reliable (and which became the backbone of many investment strategies) peaked in performance around the time when factor investing dramatically increased in popularity.

Other reads

“Banks in Disguise,” Marc Rubinstein, Net Interest.

Unzip companies across a range of industries . . . and you will find financial companies lurking inside.

“Portfolio Construction & the Lower Middle Market,” Tim Hanson, Permanent Equity. How to think about building a portfolio of private companies for multi-decade performance.

“Behind the J-Curve,” Juliet Clemens, PitchBook.

In due time we shall see whether recent vintages can make remarkable recoveries to get ahead of the curve rather than remaining behind it.

“In the Thick of It: How Performance Teams Are Driving Value Across the Organization,” FactSet. There have been significant changes in this area over the last few years, including much more remote/hybrid work, expanded responsibilities, greater integration with other teams, and an increased need for new skills.

“Multi-strategy hedge fund primer: deep dive into diversification,” Aurum.

Multi-strategy hedge funds are not a homogeneous group and they can vary enormously; adopting different business models, areas of focus, risk parameters, levels of concentration, liquidity requirements and fees.

“The Economics of Private Equity,” Alexander Ljungqvist, CFA Institute Research Foundation. This literature review summarizes major research findings regarding private equity and includes a helpful bibliography that includes conclusions from a wide variety of analyses.

“An Open Letter to Vanguard CEO, Salim Ramji,” Dave Nadig, Echo Beach.

Vanguard is entirely opaque. Your ads all promise me that there’s value in being an owner. So show me!

“Hedge funds hit by lack of private equity exits,” Harriet Agnew, Financial Times. The denominator effect and assets tied up in PE affect the allocation to other strategies in the “alternatives” category.

“For the Analyst: Peer Benchmarking Methods to Improve Earnings Forecasts,” Ahmet Kurt, et al., Enterprising Investor.

Finding suitable peers for financial analysis is a vexing task that requires careful consideration of firms’ underlying economics, accounting choices, and financial statement presentation. But without comparable financial statement information, peer benchmarking may yield less meaningful and even misleading insights that negatively impact earnings forecasts.

“Initial Observations Regarding Advisers Act Marketing Rule Compliance,” SEC. Early indications of shortcomings in implementation of the new rule, including, “Advertisements stating that the advisers were ‘free of all conflicts,’ when actual conflicts existed.”

Find a partner

“Nothing clears up a case so much as stating it to another person.” — Sherlock Holmes (from Silver Blaze by Arthur Conan Doyle).

Flashback: Early warning

A year and a few days before 9/11, Inferential Focus sent its clients a briefing, “Bombs and Networks: New Terrorist Organizational Tools and Western Intelligence.” It warned of an increased level of terrorist activity and the development of new organizational structures made possible by improved networking capabilities.

While citing other groups, the focus was on the Arab Afghans, led by Osama bin Laden, which we would soon enough learn to call Al-Qaeda. The briefing ended:

Thus, the issue becomes: Who is evolving faster — networked terrorist organizations and their communications systems or Western intelligence services? Bombs and networks are forcing bigger and faster changes in intelligence realities.

The references to Hamas in the piece are a reminder that nearly a quarter century later intelligence services have trouble understanding the potential threats emanating from those networks.

Investment risk management — which doesn’t involve matters of life and death — likewise often suffers from a lack of attention to changes in the established order of things.

Postings

The archives are full of essays that might interest you. For example, here’s a bit of “The Red, Amber, and Green of Performance Tests, a posting from 2022:

Explicit and implicit performance rules are often applied without consideration as to whether they add value or not — since they just seem right — even though they are often counterproductive. Therefore, it makes sense to identify and assess them, and to design organizations to minimize the bad decisions that can result. This is especially difficult given the chains of agents that reinforce the tendencies.

For example, an institutional asset owner may have to deal with layers of tests applied by consultants, in-house due diligence analysts, the CIO, and the investment committee. Someone at an advisory firm may use an outside research firm for ideas, need to hew to the buy list of a centralized due diligence function, make a presentation to their investment committee — and then have to sell the idea to clients. At each stage, performance exerts a gravitational pull on those involved.

Thank you for reading. Many happy total returns.

Today is the sixteenth anniversary of the debut of “the research puzzle” blog, which laid the foundation for this site. A special thanks to those who have been reading across the years.

Published: May 27, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.