Welcome to the latest edition of the Fortnightly, connecting you with interesting developments throughout the investment world.

The most recent Investment Ecosystem essay is “Thoughts about Asset Manager Pedigree,” which explores that fuzzy but frequently cited characteristic. Next up, a look at a famous asset management firm that provides profound lessons about narratives and due diligence. (Sign up to receive that and other new postings.)

On to the readings.

Active management blues

The last few weeks have been overloaded with articles about the troubles facing traditional active managers. “Index Funds Have Officially Won,” according to a John Rekenthaler column which marked the milestone of passive investment in U.S. equity funds and ETFs eclipsing active in total assets. And outflows from notable active managers dominate the headlines (examples: T. Rowe Price; Abrdn and Baillie Gifford; equity hedge funds).

Their frustration is showing. GMO believes “Your active managers are more competent than they look,” citing the narrowness of market leadership (see the next section below in that regard), but admits it has seen “an avalanche of questions coming in from institutions as to whether it is time to abandon active management, at least in U.S. large caps.”

David Einhorn says the markets are “fundamentally broken” as a result of the growth in passive:

Passive investors have no opinion about value. They’re gonna assume everybody else has done the work.

So far, firms are retreating to old talking points about the benefits of active management, in the face of evidence that shows it’s mostly a losing proposition, while asset owners and investment advisors are abandoning public market active strategies. While other market environments may be more favorable for active, a radical rethinking is in order, something that is hard to do given the long and profitable history of the established order.

The chosen ones

In a posting on “how big tech rescued the market,” Aswath Damodaran referenced the evolving names (FANG, FANGAM, Mag Seven, and other iterations) of leading stocks and the feeling that “the market would be lost without them”:

There is clearly hindsight bias in play here, since bringing in the best performing stocks of a period into a group can always create groups that have supernormal historical returns.

Today, there is one stock above all the rest, the leading beneficiary of the rush to AI: Nvidia. Phil Bak wrote about “La Vida Nvidia” at a time when “narratives are running the show”:

Now, for both companies and investors, the stock price itself is the product. It’s a big game of Number Go Up.

Don’t look now, but Bryce Elder of FT Alphaville highlighted concerns about Nvidia. The subheading of the story — “Sanctions risks, self-funded demand, customers becoming competitors . . . . Just don’t tell the shareholders” — hints at the fact that the caution comes from a credit analyst. It is a bit of an echo from the dot-com era, when one high-profile equity analyst had to defend her Amazon number-go-up actions against warnings about the company from a credit analyst at her own firm. Amazon ultimately became one of the biggest winners of all time, but it got crushed in the short term.

Endowment returns

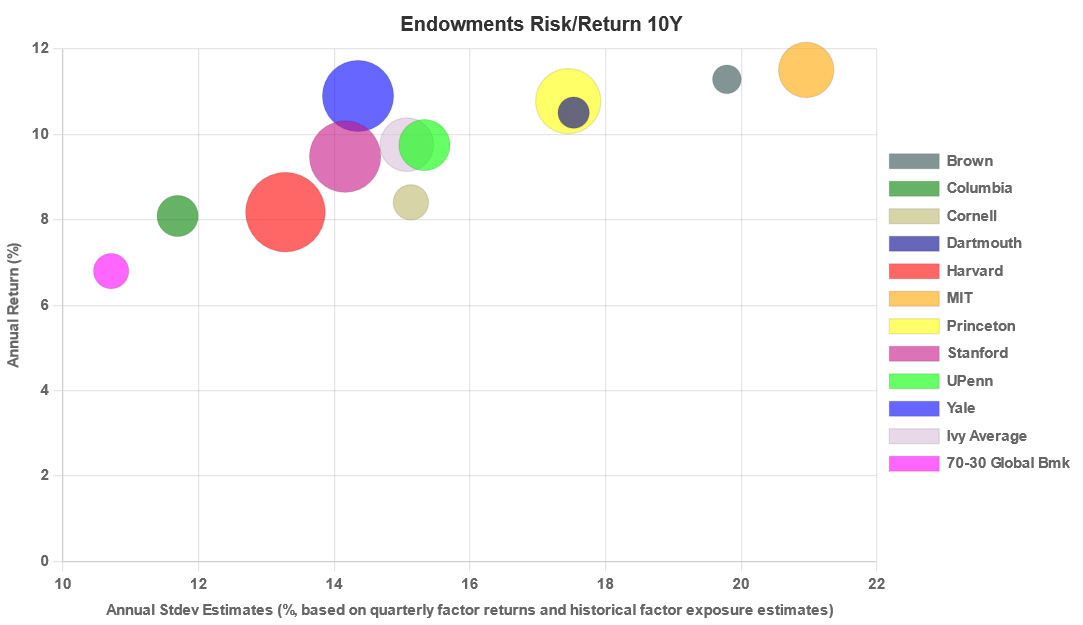

Markov Processes published a posting called “FY2023 Ivy Report Card: Volatility Laundering and the Hangover from Private Markets Investing,” which summarized the endowment returns for fiscal year 2023 for the Ivies plus MIT and Stanford. It is important to understand that the analysis is based upon the firm’s approach, which it says “largely overcome(s) the lack of transparency shading large opaque portfolios” that report aggregate performance once a year. Such style-based return analysis is imprecise but can be instructive.

The report delves into the volatility side of the equation as well, resulting in the chart shown above, which plots the annual returns for the last ten years versus the imputed standard deviations for each portfolio.

Two main conclusions:

Longer-term drivers of performance = more risk. Over 10-yrs, Ivy and elite endowments show a very clear relationship between returns and risk-taking; simply put, these endowments appear to be levered versions of a global 70/30 portfolio.

Laundered risk is still risk: Despite the masking or laundering of volatility related to investing in private markets assets, which Ivy endowment CIOs state as a benefit of the Yale model, elite endowments are significantly riskier than a balanced portfolio invested in 70% stocks.

As noted in the second item, even CIOs of major endowments make questionable statements about the volatility of private assets; see the comments from Harvard and Brown.

Also of interest is the quote from Yale’s CIO that “the Investments Office today finds itself in a market crowded with institutional investors, many of them employing similar investment strategies.” That plus an economic regime has him looking for ways to “adapt” what has come to be called “The Yale Model.”

Credit threads

Two pieces put the history of credit research and investment in context. A posting, “The Definitive History of Private Credit” by Van Spina of Wall Street Fintech, starts with Michael Milken (“Nearly all major players in today’s private credit landscape track their roots directly or indirectly to Drexel Burnham Lambert.”) and proceeds through the changes in regulation and the bank consolidations that led to today’s “golden age” of private credit. In the latest issue of Financial History, Alfred Mazzorana sheds more light on the developments of the 1970s that led to “The Birth of the Fixed Income Analyst.”

“Once a Trader, Always a Trader: The Role of Traders in Fund Management,” a paper from Gjergji Cici, et. al, concludes that corporate bond portfolio managers with backgrounds as traders (rather than as analysts) “exploit short-term trading opportunities at lower transaction costs . . ., reduce credit risk during periods of market stress and take more maturity risk during periods of large interest rate fluctuations, while holding portfolios with greater convexity.” (This brings up an interesting general question: What kinds of backgrounds are “best” for different investment positions?)

CIO job descriptions

What is the main job of a chief investment officer? Other than for small entities, shouldn’t it be to build and sustain an organization that makes good investment decisions?

It is surprising how often that core responsibility is not addressed directly in CIO position or search descriptions, whether from asset owners, asset managers, advisory firms, etc. (One example of late, CalSTRS.) Ultimately, it’s what matters.

Other reads

“Are We Baking Portfolios with Bad Ingredients?” Preston McSwain, via CAIA Association. A straightforward look at the shortcomings of reporting and analysis that hamper the asset allocation process.

“What do MAG7 earnings and a Snickers bar have in common?” Stephen Clapham, Behind the Balance Sheet.

The rationale doesn’t matter — this is accounting shrinkflation. A bit like how you pay the same price but get a smaller Snickers bar these days, this time you pay up for a larger, but lower quality, eps number.

“The Hare and the Tortoise: Assessing Passive’s Potential in Bonds,” Tim Edwards, et. al, S&P Dow Jones Indices.

Many of the arguments mocking indexing in fixed income have been either importantly qualified or outright refuted by empirical evidence.

“Discussion of Treasury Futures Positions Across Different Investor Types,” Treasury Borrowing Advisory Committee. A good example of investor segmentation, how different kinds of investors use one important vehicle (and the implications of their actions).

“Increasing Returns,” Michael Mauboussin and Dan Callahan, Morgan Stanley.

In practice, it is difficult to discern whether lower costs per unit are the result of technological improvement, economies of scale, or learning by doing.

“AI Risks and Compliance Strategies,” Ken Joseph, et. al, Kroll. The need for “policies, procedures, testing, training and recordkeeping” regarding AI implementation.

“Overcoming experimenter bias in scientific research and finance,” David Bailey, Mathematical Investor.

What is clear is that researchers from all fields of research need to take experimenter bias and the larger realm of systematic errors more seriously.

“Is Your Equity Hedge Fund Portfolio Resilient Enough for Uncertain Times?” Michele Aghassi, et. al, AQR.

The average hedge fund is unlikely to provide meaningful diversification during periods of macro uncertainty, which are also typically difficult for traditional assets.

“What is Alternative Data, and Why Does it Matter?” Byrne Hobart, Capital Gains. The goal: “Getting at the true unit economics of the business, and getting inside the head of people making strategic decisions.”

Conviction

“So much of what people call ‘conviction’ is actually a willful disregard of facts that might change their mind.” — Morgan Housel.

Flashback: Independent research

In late 2003, Thomson Financial published what it termed the “first and only directory of independent investment research.” Coming on the heels of the Global Research Analyst Settlement, it heralded a new era of research on Wall Street. (For more about the independent research part of the settlement, see this series from The Research Puzzle.)

The hefty blue book included firms, analysts, and companies covered by those deemed to be “independent,” which ranged from single person operations to long-standing, larger organizations. The credit rating agencies were in there too; the subprime debacle a few years later would cause their independence to be questioned.

Many of the firms are long gone and the book was truly the “first and only” such guide. It marked a time when it was thought that the old sell-side research model might be changing for good. That didn’t happen.

Postings

Explore the archives to find nuggets like “Ascendance of the Pod Masters” from March 2023.

Thanks for reading. Many happy total returns.

Published: February 19, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.