Since the last Fortnightly, two postings were published on the site that leveraged the work of Richard Ennis. The first looked at the evolution of the institutional investment consulting industry, as featured in his book. The second explored his writings over the last few years, which have challenged the conventional wisdom regarding governance and investment policy by asset owners.

In addition, a Linkedin article summarized the Investment Ecosystem series on the social and cultural underpinnings of investment organizations and roles that was published earlier this year.

Two notes: Make sure to subscribe for email updates so you don’t miss any of the postings — and the next Fortnightly will be delayed by a day (the normal schedule would have had it coming out on Christmas).

On to the readings.

Diamonds in the rough

We’re still a couple months away from spring training, but Bob Seawright got a jump on it with his latest piece, “Revenge of the Nerds.” It traces the emergence of analytics as a driving force in baseball, starting with Bill James and Sabermetrics and its impact (decades later) in the professional game, recounted in the book and movie Moneyball. The whole story serves as an analogy to developments in the investing world (and there are some direct references to it).

At the core of the Moneyball mentality is the desire to identify actual value that is greater than the perceived value in the marketplace. (The same goes in reverse; you don’t want to pay more than you should based upon the evidence, even though that often happens in the heat of the moment. In related news, after Seawright’s posting, Shohei Ohtani agreed to a contract roughly twice as large as any other in baseball history. How do you judge what a generational talent is worth?)

After writing about how edges get worn away over time, Seawright closes with this:

Ongoing and consistent outperformance, in baseball, the markets, and in life, is staggeringly difficult. Prepare and respond accordingly. We get better and keep getting better at things by being responsive, observant, and applying what we’ve learned. Over and over again.

Fumble-itis

Another sports-related article with an investing angle comes from the Daily Coach, this time regarding (American) football. A famous hedge fund manager, David Tepper, bought the Carolina Panthers in 2018 and has made quite a mess of it. The article says that Tepper “demonstrates a lack of understanding of the requirements needed to build a championship organization.”

Later, the author writes, “The ‘lone star’ model of hiring in the NFL has proven to be a failure.” If you read the story and think about the organizational weaknesses common in the investment industry, the connections come easily.

Vanguard

Some investment firms are closely identified with one style or ethos, even after they have grown into other categories and beliefs. Vanguard certainly fits the bill; the thoughts that come to mind are Bogle, indexing, and a focus on keeping costs low.

Last week, the firm announced it was selling its OCIO operation to Mercer. Mercer’s press release referenced “Vanguard’s differentiated investment philosophy;” it will be interesting to see how the contrasting belief systems at the two organizations are reconciled in the coming years and what that means for current clients, who thought they were getting one thing and may end up with another.

Also of interest: John Rekenthaler on Vanguard pitching margin loans.

Heads I win . . .

As discussed in the last Fortnightly, natural language processing and artificial intelligence have taken the parsing of language (and, in response, the crafting of language) to a whole new level.

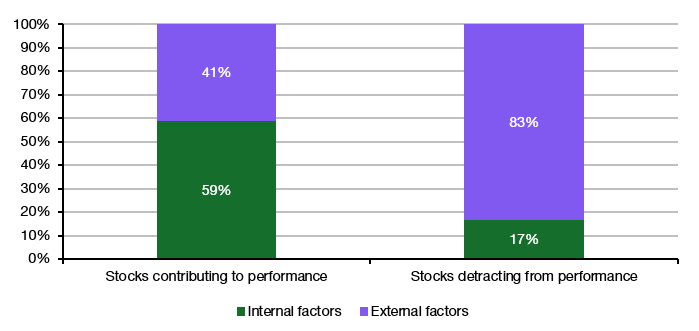

Joachim Klement featured the chart above in a posting about Meng Wang’s research paper, “Heads I Win, Tails It’s Chance: Mutual Fund Performance Self-attribution.”

Perceptive due diligence analysts try to assess how objective portfolio managers are about assessing credit and blame. Now there are tools that can help in that task. Will the dialogue change as a result?

Goodbyes

The legendary Charlie Munger passed away a few weeks short of his hundredth birthday, prompting a number of great tributes, including his obituary in the New York Times and articles in the Wall Street Journal from Jason Zweig and Gregory Zuckerman.

Josh Brown’s Reformed Broker blog was interesting, unique, and fun, a mainstay of the financial blogosphere that propelled him to great success. He’s not going away, but the site and persona are. Here’s his farewell.

Somerset Capital Management announced it was closing after the majority of its assets were pulled by St. James’s Place. The story illustrates how large subadvisory mandates can change the fortunes of an asset management firm, in good ways and bad.

We’re getting to the end of the year, so there are more than enough 2024 outlook pieces to read — and retrospectives on 2023, including a fun one of those from Nick Mazing that looks at the trends in conference-call words, among them “double-click.” (Do it, don’t say it.)

Other reads

“Why Do Investors Play Low Probability Games?” Joe Wiggins, Behavioural Investment. This is a perceptive list of reasons in answer to the question.

“Tangible change at Fordham endowment in manager re-vamp,” Sarah Rundell, Top1000Funds.

We have more managers than we need and instead of adding value they are detracting, costing us money, and in some cases, providing only benchmark performance.

“Big Ideas in Tech 2024,” Andressen Horowitz. A variety of possibilities in different categories summarized in short paragraphs.

“How on Earth do you Allocate Effectively when the US Market has Grown so Large?” Brandes Center. Challenges for US and foreign investors (and for readers trying to figure out Exhibit 9).

“Surveying the Medley of Sub Lines in Private Funds,” Patrick Warren, MSCI.

Given the wide range of GP behavior, it is critical for limited partners (LPs) to maintain visibility into sub-line usage when forecasting cash flows.

“The next stage of ESG evolution in the pension landscape,” Create Research. This survey provides a good picture of the changing ESG landscape; one theme is “from virtue signaling to value signaling.”

“‘A perfect storm’: How and why top gatekeepers are adding private assets,” Tania Mitra, Citywire Pro Buyer.

“There’s immense pressure from the asset management industry for advisors to move into alternatives but there’s also an absurd amount of client demand and wealth advisors believe in it,” said Kenny Pitman, director of alternative investments at Mercer. “So it’s coming from all angles [and] it seems like a little bit of a perfect storm.”

“Bitcoin Valuation: Four Methods,” Rob Price, Enterprising Investor. Which, if any, of these approaches are useful in trying to put a value on the cryptocurrency?

“SEC, FASB Take Closer Look at Companies’ Statement of Cash Flows,” Mark Maurer, Wall Street Journal.

The SEC has observed that some companies “don’t dedicate the same level of rigor and attention” to the cash-flow statement compared with other statements.

“Artificial Intelligence,” Capco. The firm’s Journal of Financial Transformation provides a number of articles, grouped within technological, operational, and organizational categories.

“How (and Why) to Ask ‘Craft Questions’,” Rob Walker, The Art of Noticing. Important points for those conducting due diligence interviews.

“The Quality of New Entrants,” Chris Satterthwaite, Verdad.

We believe discerning among small-cap stocks on the basis of both valuation and quality remains paramount to avoid the large number of unattractive, low-quality constituents that have entered the universe in recent years.

“Investment banks and the scourge of pre-Christmas job cuts,” Sarah Butcher, EFinancialCareers. ‘Tis the season.

“500 Questions to Ask Your Parents,” Umbrex. It’s never too late until it’s too late.

Never stop

“I think a life properly lived is just learn, learn, learn all the time.” — Charlie Munger (from a collection of his quotes on Farnam Street).

Flashback: Memos from Ace

Bear Stearns is best known today as one of the first casualties of the financial crisis. The demise came fifteen years after Alan “Ace” Greenberg ended his time as managing partner and CEO. He became known for the memos he would send to his staff, some of which were assembled into a book, Memos from the Chairman, which was released in 1996.

In the forward, Warren Buffett wrote, “Ace Greenberg does almost everything better than I do — bridge, magic tricks, dog training, arbitrage — all the important things in life.” Through Greenberg’s memos, including frequent references to the fictional Haimchinkel Malintz Anaynikal, you see his “wit and wisdom;” the ups and downs of markets and Bear’s fortunes within them; and the culture he fostered, including doing the little things right.

The most famous of the memos was about the need to save paper clips. You can read more about them in a Washington Post article that happened to be published the day before the 1987 stock market crash.

Postings

Explore the archives and/or use search function found on every page of the site to locate postings of interest to you. Most apply across the board in the industry despite the fact that they are divvied up into categories. One example is “Addressing the Culture Gap.” It starts:

An enduring question: To what degree do ideas, theories, and principles regarding organizations apply to investment organizations?

Thanks for reading. Many happy total returns.

Published: December 11, 2023

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.