As a reminder, all of the content on The Investment Ecosystem is now free. Dig in.

The most recent posting, “Cooking Up the Ingredients of an Investment Recipe,” reviewed a five-part description of investment strategy that offers a self-examination process for asset managers — and a way for allocators to classify and evaluate them. Next up is “The Double-Edged Sword of Manager Selection.” Subscribe to get it in your inbox.

Now, on to the readings.

The fund

Few books about investment organizations have gotten the attention given to The Fund, Rob Copeland’s look at Ray Dalio and Bridgewater Associates. It has been excerpted in a number of publications, with different eye-opening stories in each one (including the New York Times, New York, Insider, Vanity Fair, and Semafor). There have also been many reviews and related articles, such as Robin Wigglesworth’s piece in the Financial Times.

Bridgewater’s response is in full swing — here is an Institutional Investor story — but no doubt the real action is at the firm itself and especially in meetings with its clients. Dalio has carefully cultivated an image over time of a unique and special culture at the firm — in fact, the most unusual culture of any firm of size in the investment business.

By all accounts, the book is not much about investments, but about organizational culture, leadership, and the stories that animate the business and the flow of money within it. It will affect the perception of the industry — or perhaps reinforce it, as it did for Mark Gimein in the New York Times Book Review:

Most of “The Fund” doesn’t feel like a book about finance. Instead, it is about how a man of surpassing mediocrity used money to control and humiliate, and how much people abased themselves for it. Which, come to think of it, makes it one of the better books ever written about Wall Street.

It also raise questions for the institutional investors who have built the mountain of assets at Bridgewater. How will they find what they believe to be the truth and what will they do in response?

The trial

It didn’t take long for the jury to come to a verdict in the trial of Sam Bankman-Fried, adding a coda to yet another boom-to-bust chapter in market history.

Of particular note was the commentary from a partner at Sequoia (which had provided funding to FTX and which published a glowing profile of Bankman-Fried two months before everything fell apart). Alfred Lin tweeted:

Immediately after FTX collapsed, we extensively reviewed our due diligence process and evaluated our 18-month working relationship with SBF. We concluded that we had been deliberately misled and lied to.

He was “fried” in response. For example, from Jamie Powell:

“due diligence”, my brother in christ it had no board of directors, no cfo, no head of risk and was incorporated in antigua and barbuda. 2 mins of googling would have got you there.

Chris Addy of Castle Hall Diligence arrived at a couple of big-picture conclusions from the whole affair: that crypto “is not yet ready for institutional investment” and that “FTX raises profound questions around the venture capital investment model.”

(Learning how to crack the narrative of asset managers is at the heart of the Academy due diligence course. The first step is wanting to do it.)

ODD and IDD

The Standards Board for Alternative Investments and CAIA Association have released a great report, “Striking the Right Balance: Navigating Operational and Investment Due Diligence in Institutional Investments.” In a brief six pages, it covers the emergence of ODD in the wake of the financial crisis, as well as the challenges that developed during the “Goldilocks era” that followed.

Among the topics are FOMO-driven compromises to standards and the reliance on others for due diligence (or on the marketing spiels of managers). Importantly, the resourcing and power imbalances between IDD and ODD — and the competition between them — take center stage, thus the theme of “striking the right balance,” in governance, process, resourcing, etc.

Total shareholder return

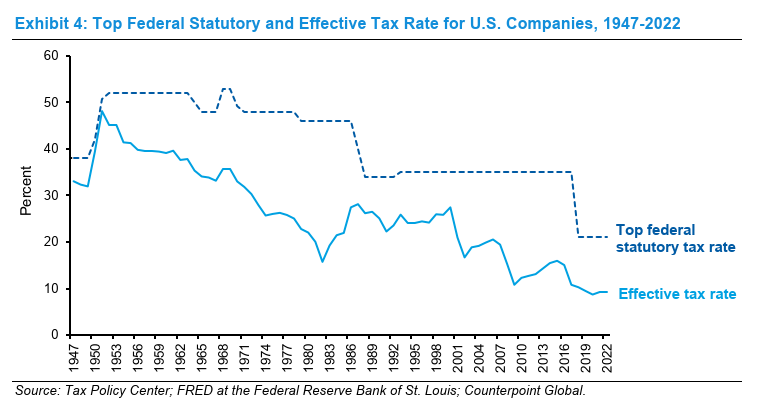

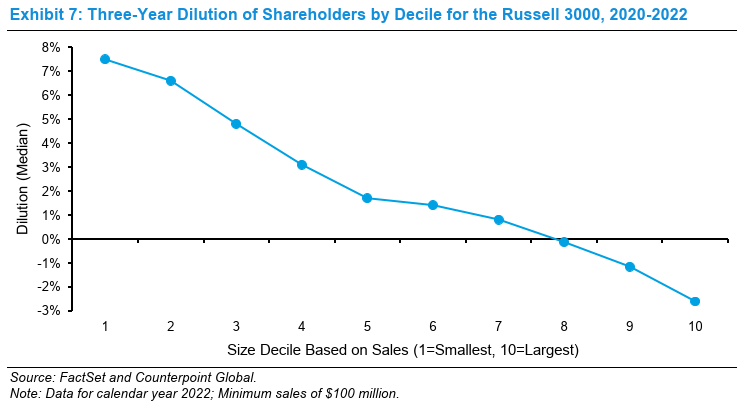

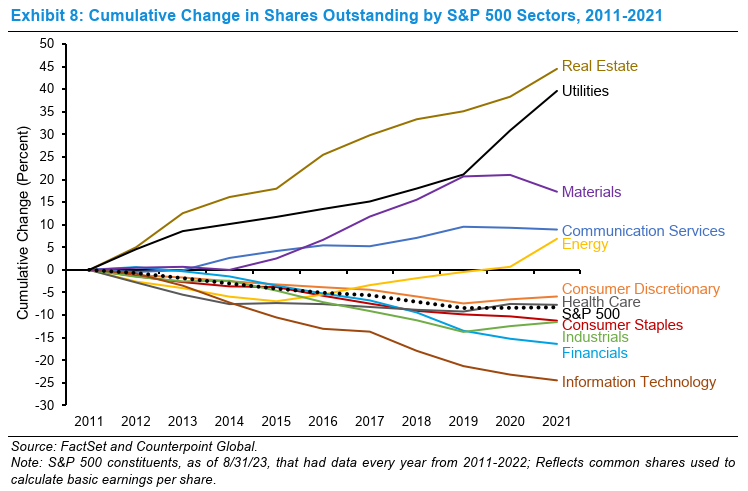

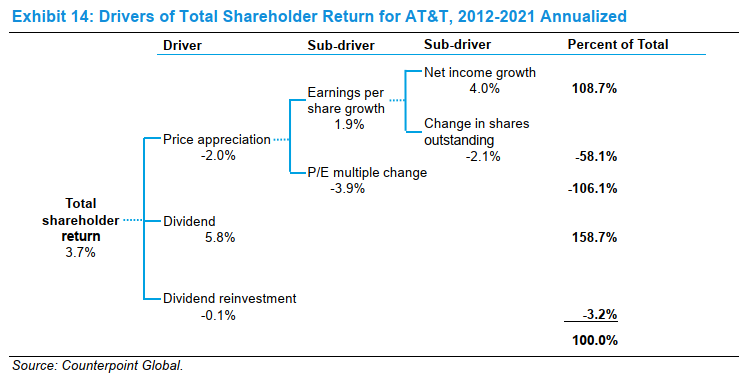

The latest research from Michael Mauboussin and Dan Callaghan is “Total Shareholder Return: Linking the Drivers of Total Returns to Fundamentals.” As is usual for them, it contains a number of good exhibits, among them ones that show corporate tax rates across the decades (down, down, down); dilution by sales deciles (monotonic); changes in shares outstanding by sector (big differences); and the instructive drivers of total return for AT&T. Also, there’s a checklist for assessing prospective returns.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Personalized investment

Broadridge released a report, “U.S. advisor-sold asset management: This time it’s personal,” full of data supporting its assertion:

Most asset managers are still approaching a 21st-century clientele with 20th-century business models. Today’s U.S. investors demand an increasingly personalized approach to investing, reshaping product and distribution strategies across the industry.

The five themes emphasized are additional portfolio objectives of clients, a focus on holistic outcomes, evolution away from the “tax inefficiencies and non-customizable pooled format” of mutual funds, shifting capital markets, and increasing industry concentration. There are a number of “action items” with details on what “successful managers” will do in the coming years to navigate the large advisor-sold market for investment products and services.

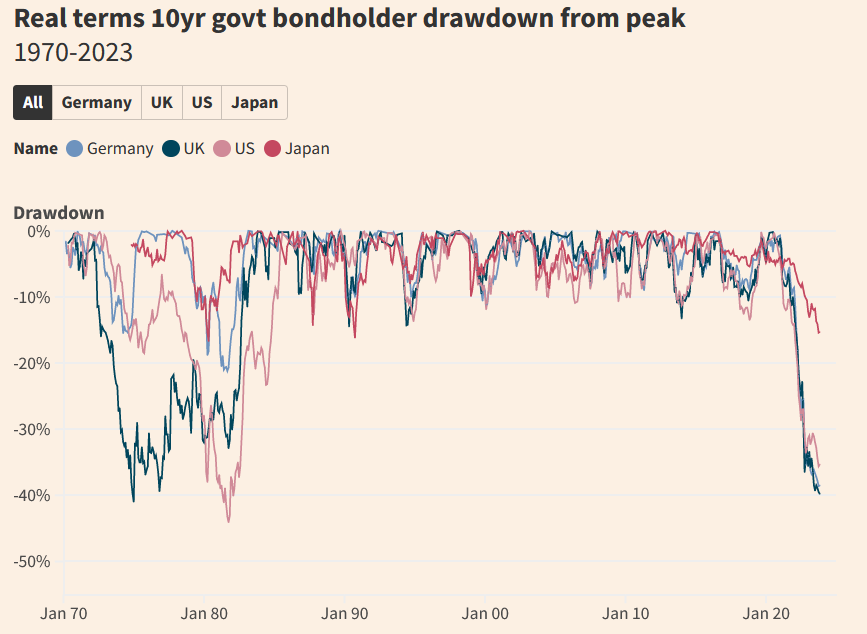

Drawdowns

Toby Nangle started an article in the Financial Times with this:

All the worst things about the 1970s seem to be coming back. Inflation. Strikes. Really silly flared trousers. And of course double-digit bond portfolio drawdowns.

The charts provided show that the global bond bear market of late stands out “for its magnitude and pace.” But, as the chart above illustrates, the drawdown from a half century ago lasted a good long time, prompting the description back then of bonds as “certificates of confiscation.” Nangle’s concluding comparison of the two periods:

So while this bear market has been a shocker, we reckon we’ll need to check back in 2034 to see whether it beats the 1970s for sheer doggedness.

Other reads

“Should CalPERS Fire Everyone And Just Buy Some ETFs?” Meb Faber. “All the time and money spent . . . Is it just CalPERS, or is it the industry?”

“How the Fearless Fund Lawsuit Is Provoking Outrage, New DEI Strategies — and Renewed Commitment,” Michelle Celarier, Institutional Investor.

With the stakes so high, the Fearless Fund case is forcing venture capitalists and allocators alike to rethink or reshape their efforts at increasing diversity, including among the companies they invest in, the managers they hire, and their own organizations.

“Big hedge funds pay ‘silly’ money, says founder of Europe’s largest manager,” Kaye Wiggins and Harriet Agnew, Financial Times. Paul Marshall bemoans a “kind of battery-hen farming merry-go-round,” which is “not the right way to build great businesses or even to build a great industry for our clients.” (Plus, “surfing the guarantee.”)

“The Transformation of Labor Markets,” PGIM.

For investors, the forces reshaping global labor markets will impact wages, productivity, unemployment, economic growth, inflation and fiscal deficits — creating a new roster of winning and losing industries and countries.

“Money Managers With $100 Trillion Confront End of the Bull Market,” Silla Brush and Loukia Gyftopoulou, Bloomberg. Big active managers “have been bleeding cash” (client assets, that is).

“Thinking Broadly: Improving Active Performance Via Systematic Extensions,” Acadian.

Systematic extension strategies . . . have been underutilized for years (Figure 1) due to hazy perceptions of their underperformance around the Global Financial Crisis (GFC) and a blurry leeriness of risks associated with shorting.

“Sandy Gottesman: A Whale of a Value Investor and Philanthropist,” James Russell Kelly, article in Financial History (within the “publications panel at the bottom of the page). On “The Buffett Group” and how it evolved, and the career of the founder of First Manhattan.

“11 Signs to Avoid Management Meltdowns,” Todd Wenning, Flyover Stocks. Indicators of ethical collapse and factors that impede “management’s ability to make rational, ethical, and thoughtful decisions.”

“Blacklisted ‘woke’ firms like BlackRock and State Street still have a lock on AUM in oil states . . .,” Oisin Breen, RIABiz.

Perhaps not surprisingly, pension fund managers are leading the backlash against the backlash.

“Large Language Models Understand and Can be Enhanced by Emotional Stimuli,” Cheng Li, et. al, arXiv. Can an “EmotionPrompt” improve the relative performance of LLMs?

Mutual fund performance, Jeffrey Ptak, @syouth1. A series of revealing charts, with this conclusion:

In summary, with only a third of active U.S. stock funds beating their index before fees over the average 10-year period and with the average fund outperforming by just 0.26% p.a. (excluding dead funds), one thing seems pretty clear: Active U.S. stock funds charge too much.

Change

“In times of change, learners inherit the earth, while the learned find themselves beautifully equipped to deal with a world that no longer exists.” — Eric Hoffer.

Flashback: The Tao Jones

In 1983, Bennett Goodspeed of Inferential Focus wrote The Tao Jones Averages: A Guide to Whole-Brained Investing. A 2010 review of it from the original “research puzzle” blog includes this:

While it’s tempting to view the book as gauzy Eastern philosophy with no practical application, its central message is that a good investment process is one of balance, and that the lopsided approach practiced by most organizations and individuals is doomed to fail.

In sync with the Eric Hoffer quote above, the last two pages of the book include a section called “The Warmth of the Herd,” which begins this way:

Wall Street has a bias in favor of logical, left-brained thinking. Consequently, the right-brained sensing needed to decipher changing conditions tends to be ignored or overridden by reason. As a result, the collective wisdom is often surprised.

Postings

Check out the archives (the paywall is no more) and search some of the categories. You’ll find evergreen postings of interest. Here’s one from January 2022: “The Goal of Explanatory Depth.”

Thanks for reading. Many happy total returns.

Published: November 13, 2023

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.