Among the latest “clippings” in our visually-oriented Substack potpourri are items on the bond breakout, changing leverage in direct lending, looking for crowding in quant-land, the pig in the python at interval funds, and more. See it here.

On to the readings.

Who owns what

One important part of ecosystem thinking in the investment world is understanding which types of investors own what and how that affects pricing, especially when circumstances change. A recent edition of the weekly credit update from JunkBondInvestor, “Who Buys It Next?” lays it out particularly well:

There are two questions every credit investor should ask before making a new investment: who owns this paper and who would buy it if they needed to sell?

The answer often matters more than leverage, price, or all-in yield, and almost nobody focuses on it.

Credit markets have always worked this way. Different cohorts hold paper under different rules. Different rules mean different prices when paper has to move between them. The handoff between buyer bases has always been where price discovery happens on stressed names.

It goes on to detail how the dynamics have changed in the last few years. In some respects, it is as it always has been — “Each step is a handoff. Each handoff has a price.” — but, as structural change has occurred, “the handoffs are harder now.”

For those not well versed in the credit markets, some of the details cited might make little sense, but don’t skip this important piece:

~ With the emergence of private credit as an emphasis for many asset owners, the nature of credit exposures across the landscape and the interplay among the different types of credit have become an important backdrop to selection practices and the ongoing valuation (and risk management) of positions.

~ Fixed income exposures are expected to hum along in the background while equity investments garner attention and excitement, but most financial crises are rooted in bad credit, usually with structural shifts and “innovations” happening in advance.

~ To quote the posting, “Almost nobody focuses on it;” that’s true in other markets as well. People do pay attention to who owns what, but in a limited way, via 13Fs and other public reports. That reveals much but not all of what the highest profile investors have done, but it’s still an incomplete picture, devoid of the kind of understanding demonstrated in this JunkBondInvestor piece.

(For example, consider the kinds of handoffs now happening in software stocks as highlighted in the Sparkline report featured below.)

Keeping the faith

In his article “Trading in the end times: keeping faith in financial markets,” Crawford Spence writes that “how asset managers themselves think and explain their own position in financial markets is rarely explored.” He then proceeds with such exploration:

Notwithstanding variation in styles and strategies . . . we can think of active fund management as a religious group in the sense that it has a unified system of beliefs and practices and constitutes a single moral community centred around the sacred objective of generating “alpha” (above market returns).

The reactions of active advocates in response to the increasing dominance of “profane, passive investing” is the subject of Spence’s paper (the topic was also covered in a 2023 Investment Ecosystem posting, “Cognitive Dissonance and Stasis in Active Management”).

Spence sees four “faith-based survival strategies” in play by those involved in active management: theological innovation, ministry outreach, praying for the end times, and finding new converts.

It has been interesting to watch the evolution of the reaction to passive over the decades, from the early days (“passive investing is un-American”) to current concerns about less market efficiency because passive has gained the upper hand. While Spence’s work is based upon a relatively small number of practitioners in one part of the world, it faithfully represents the “cracks in the underlying belief system of [at least some] active managers” — and the changing views and coping strategies in response to them.

See, for example, these comments from two fund managers:

I think fees will definitely continue to come down. Fees have come down a long way but we are probably still being over remunerated for what we do.

I do not mind the active management industry shrinking in Australia because the average fund largely underperforms the index and charges a fee for the pleasure of it.

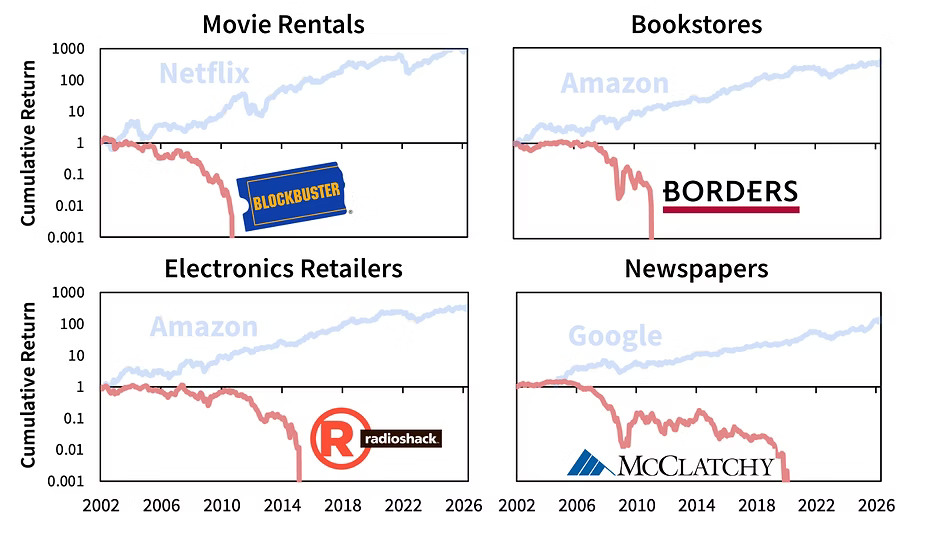

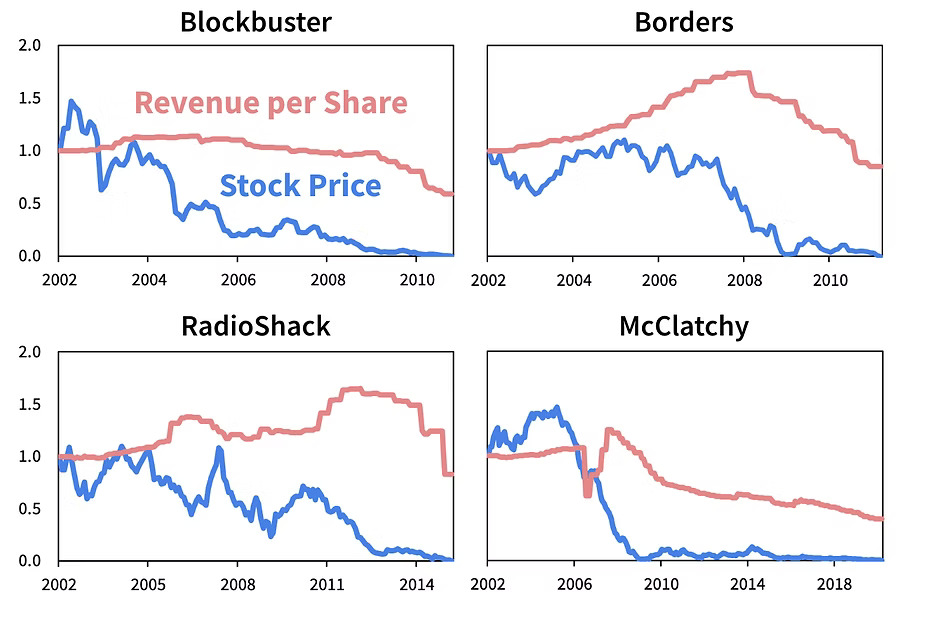

The fear of AI disruption has caused downdrafts in many software stocks as well as those in some other industries. That’s the subject of “AI Disruption: Moats and Value Traps,” the latest report from Kai Wu of Sparkline Capital.

Some of the classic disruptions appear in the graphic above. A second image shows that in these cases company revenues held up well for quite a while, with dire consequences:

Falling prices relative to lagged fundamentals created the illusion of cheapness — luring value investors onto sinking ships.

With that as a backdrop, Wu considers the conditions that might favor companies in the face of the latest disruptive threat, including examining traditional value versus intrinsic value (the subject of previous Sparkline reports). He then focuses on software:

For investors, the sweet spot consists of software companies [that are] AI early adopters with strong complementary moats. These firms not only enjoy naturally defensible businesses but are also actively positioning for the age of AI.

What’s coming? A time of fat tails in software returns:

For investors able to separate AI survivors from value traps, whether using intangible value or another framework, we believe software stocks represent an unusually attractive stockpicking opportunity today.

The shelf life of prudence

The abstract for “The Shelf Life of Prudence: Trust Law, Reauthorization, and the Temporal Limits of Fiduciary Judgment,” by Ian Edwards begins:

This Article examines how the common law of trusts evaluates fiduciary prudence over time, and how that standard diverges from prevailing practice in defined-benefit pension plan governance. Trust law treats prudence as a continuing obligation requiring fiduciaries to exercise judgment under “circumstances then prevailing.” Yet institutional practice often treats prior approvals and professional techniques as sufficient by default, allowing authorization to persist without renewed fiduciary evaluation.

The practices go beyond those of defined-benefit plans to other situations where fiduciary responsibility exists. Yet how often does this idea come up at all? Governance has an inertia to it that doesn’t pause for basic assumptions to be rethought:

Modern fiduciary practice operates within a dense architecture of policies, benchmarks, delegation frameworks, and professional conventions that present themselves as compliance.

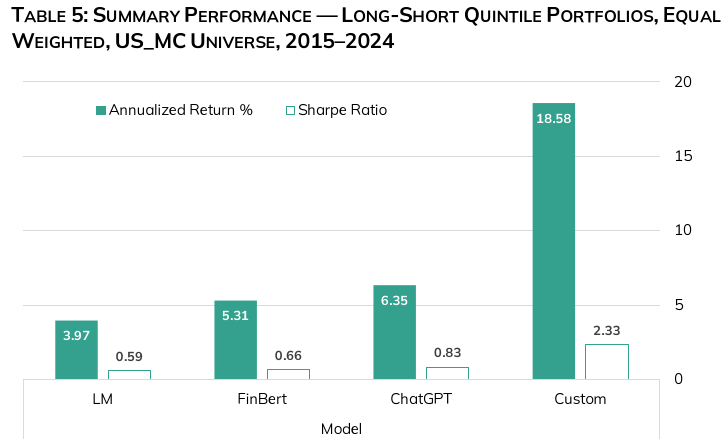

AI and investing In “Quants Learn to Read (Finally),” Harindra de Silva of AJO Vista documents “the evolution of textual analysis in quantitative finance.” While the capabilities of today’s AI applications have led to great leaps in the ability to process and interpret words, it remains the case that off-the-shelf products fall short when interpreting investment information. (The chart above provides one study that shows that.)

In “Quants Learn to Read (Finally),” Harindra de Silva of AJO Vista documents “the evolution of textual analysis in quantitative finance.” While the capabilities of today’s AI applications have led to great leaps in the ability to process and interpret words, it remains the case that off-the-shelf products fall short when interpreting investment information. (The chart above provides one study that shows that.)

The bottom line:

Technological advantages in finance often belong to those who painstakingly tailor their algorithms and models to the unique structural, semantic, and logical realities of the capital markets. Custom training is a key mechanism by which an edge can be created and sustained.

Private equity

GMO published a two-part quarterly letter about private equity. In Part 1, Ben Inker and John Pease present a theme:

With private equity portfolios looking ever more concentrated on a small set of risks, investors in these portfolios look more vulnerable to certain types of economic shocks than they ever have.

More specifically:

Not only have small caps seldom been a lower-quality group of businesses than they are today, but the buyout space is lower-quality still.

They offer commentary on software in particular and end with a section on “hedging the downside,” which leads to a strategy managed by GMO (a common asset manager ploy, although it may be spot on; do your own work).

Part 2 is by Inker, a “letter to the investment committee on private equity.” While he writes, “I’m not trying to make the case that institutions should abandon private equity,” it is full of ideas that are contrary to the ways in which such investments are approached by most governing boards now. A few quotes:

While we all know “past performance is not indicative of future results,” it is extremely hard to overstate how central past performance is to investors’ decision-making when choosing private asset managers. You are buying into a blind pool, and almost the only thing you know is what the manager did in the past.

The bar to invest in a private equity manager should be high — arguably even higher than it is for active public asset managers, since you’ll be stuck paying PE managers high fees for a long time, even if you lose conviction in the interim.

Private equity programs are not meant to run on autopilot; there are critical questions to answer and, for many institutions, disappointing results to grapple with.

Other reads

“Is Nvidia Too Big to Fail?” Robin Wigglesworth, FT Alphaville.

This all means that fate of the equity market is unusually tied to the fate of not just one technology, but just one company, to a degree possibly unprecedented in modern history?

“Recombination,” Michael Aronstein, The Alternatives Universe. Get ready for a downshift in the five-year numbers at leading asset owners.

“The Three Seeds,” Rohit Yadav, All Things VC.

Multi-stage funds didn’t push into Seed by writing more $3M checks. They pushed in by writing $25M+ checks and labeling them Seed.

“Cocaine on the Tables,” TSCS. The impact of mechanical bids on market performance.

“Bayes and Base Rates 2.0: How History Can Guide Our Assessment of the Future, Michael Mauboussin and Dan Callahan, Morgan Stanley Investment Management.

Base rates are dynamic distributions. That means they change as the world changes. There is nothing in past results that says OpenAI’s projected rates of growth are unachievable. Still, there is value in knowing that this would be a novel accomplishment were it to occur.

“Litigation Finance: An Industry at a Crossroads,” Joshua Myers, Enterprising Investor. Implications for the parties involved from shifts in the structure of litigation finance.

“The Trouble with AI Investment Writing,” Joe Wiggins, Behavioural Investment.

If investment writing is just the result of a few prompts, it lacks any original thought and fails to represent the author’s voice. Rather it is simply the output of a predictive system that has no stake in what it generates.

“Greedy Portfolio Construction: A Practical Alternative to Full-Universe Optimization,” Andreas Steiner, SSRN. Parsimonious approaches to common portfolio objectives (with a different, useful approach to providing references at the end of the paper).

“Compliant on Paper, but Exposed in Practice,” Greg Davies, Oxford Risk.

There are two sides to any set of laws: the words that comprise them (the letter), and the intentions behind them (the spirit). Typical suitability processes focus on the wrong one.

First things first

“Judge a man by his questions rather than by his answers.” — Voltaire.

Flashback: Idea velocity

“Dasan” was an anonymous investment/trading blogger who was popular among hedge fund readers (and wannabe hedge-funders). According to ChatGPT, his “SAC-related posts were especially widely shared because they offered a rare semi-insider perspective on Steve Cohen-era culture, pressure intensity, and portfolio management dynamics.”

One viral posting was about “idea velocity.” The timing of it, in 2013, meant it started like this:

SAC, the infamous hedge fund led by mercurial, secretive, super art collector Stevie Cohen is legendary. They have recently been accused of insider trading and it sure looks like they are guilty.

The piece calls idea velocity “the underpinning of everything in The Game.” In today’s era, dominated by pod shops, that’s still the case.

A devilish lexicon

A 2024 posting provided a review of Jason Zweig’s 2015 book, The Devil’s Financial Dictionary:

Zweig provides a mix of history, etymology, and satire that takes the book well beyond the typical dictionary. Skepticism about the language and practices of the investment world is essential for lay investors and professionals alike — and the recurring abuses and calamities of the investment industry come in for deserved cynicism.

One example relevant to our times (and some impending IPOs):

NEW ERA, n. A period of collective investing insanity during which, according to its proponents, stocks should be valued by new rules — such as “this company is growing so fast that its value is infinite.”

Thanks for reading. Many happy total returns.

Published: May 25, 2026

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.