As we approach the start of a new year, thank you for your support of these writings and your thoughtful comments.

If you missed it, the first edition of the new “clippings” offshoot of the Investment Ecosystem came out last week. Each posting will feature images and snippets of text, all of which you can view in less than a minute; links are included if you want to get more detail.

It can be found on the Substack platform; you can subscribe here to receive each posting by email.

Spray and pray

Two decades after its founding, Tiger Global became known for its unusual approach to venture capital investing:

The New York-based hedge fund and venture firm had earned a global reputation for its fast-paced, “spray-and-pray” style of investing, writing giant checks far and wide in hopes that a small number of them would yield outstanding returns. Tiger rarely took board seats, assumed a hands-off approach to oversight, and while it invested in companies at all stages of their life cycle, it became known for driving up company valuations in late-stage deals.

That quote comes from “Big bets and broken unicorns: Tiger Global’s rise and reckoning,” an article by Issie Lapowsky for Rest of World, which tracks the firm’s impact on companies in India that hoped for and angled for the easy money and then got it. (Things didn’t work out as planned.)

It’s an interesting story about how waves of capital can distort things. In the aftermath:

The founders of these now-infamous companies have rightly borne the brunt of scrutiny for the scandals and failures that followed. Yet questions remain: How much of the blame should lie with Tiger and other hyperaggressive investors for fueling the global unicorn bubble, and the slaughter that followed?

And, as another bubble swells in the artificial intelligence era, has anyone learned their lesson?

An equilibrium of disequilibrium

A captivating posting by The Terminalist tackles the history of information markets. An important starting point:

There must always be enough information asymmetry — enough gap between what prices reveal and what informed traders know — to compensate those traders for their costly research. Markets . . . exist in a perpetual state of almost-efficient, never quite arriving.

An equilibrium of disequilibrium.

The author walks through six key changes in information markets (starting in 1531!), with the pattern repeating over and over:

Chaos to order. Disorder to structure. Fragmentation to unification. Each channelled new technology to reduce information entropy. The playbook never changed.

Which brings us to the present day. Who will create the “high-quality evaluation infrastructure” to corral large language models and other capabilities in a way that becomes the new standard? The bottom line is a lucrative bottom line:

Financial markets have a perpetual need to reduce information asymmetry. And those that build the infrastructure to minimise it across market participants capture enduring value.

Two sides of capitalism

Appearing within a couple of days of each other:

“Why Sears’s Last Great Hope Was a Promise That Never Materialized,” Lauren Coleman-Lochner, New York Times. The story of Sears, Kmart, and Seritage Growth Properties, featuring two decades of conflicts of interest and extraction capitalism.

“The Boss Who Gave His Employees a $240 Million Gift,” Gregory Zuckerman, Wall Street Journal. “When Graham Walker sold his family’s Louisiana company, he made sure his 540 employees got a cut.”

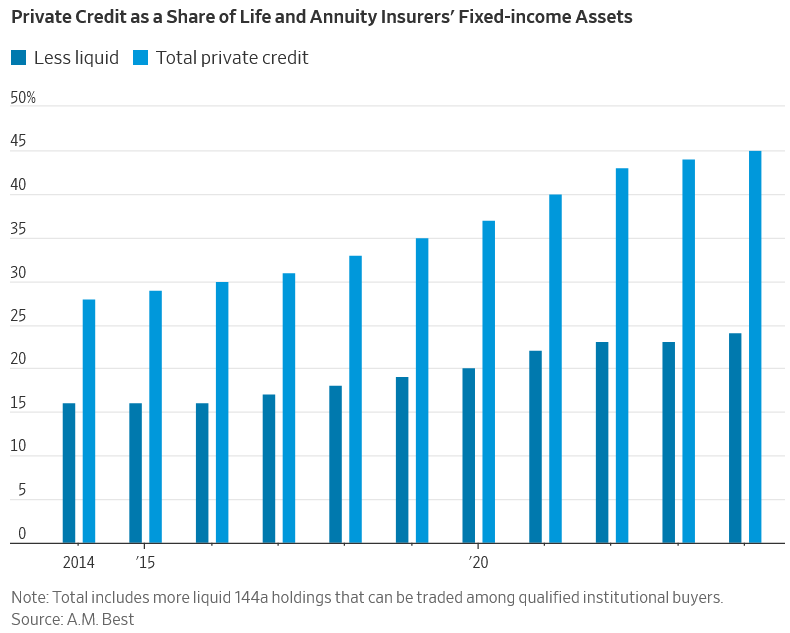

Insurance assets

This chart is from a Wall Street Journal article by Heather Gillers, “Warren Buffett and Private Equity Both Love Insurance. The Similarities End There.” It shows the increased use of private credit in insurance portfolios.

While private-asset managers appear to be using insurance companies to follow “in Buffett’s footsteps,” the author lays out “the radically different philosophies of a 95-year-old legend and the new crop of float-hungry investor-insurers.”

Ajit Jain, the head of Berkshire Hathaway’s insurance operations, was quoted as saying that a more difficult economic environment may expose the riskiness of the life insurance portfolios that are in vogue right now, the adoption of which “could end in tears.”

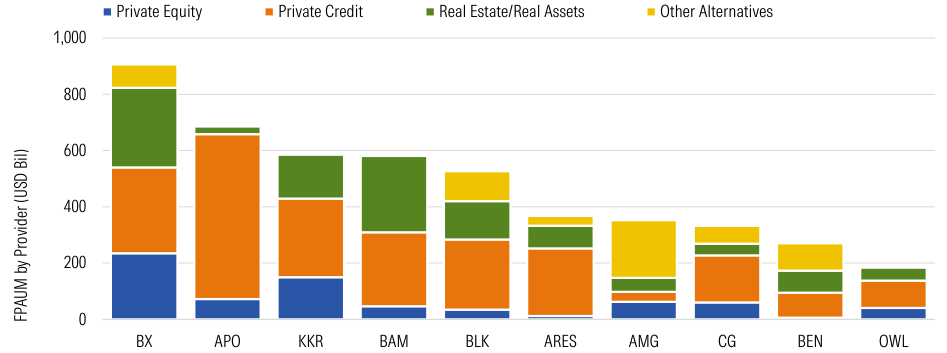

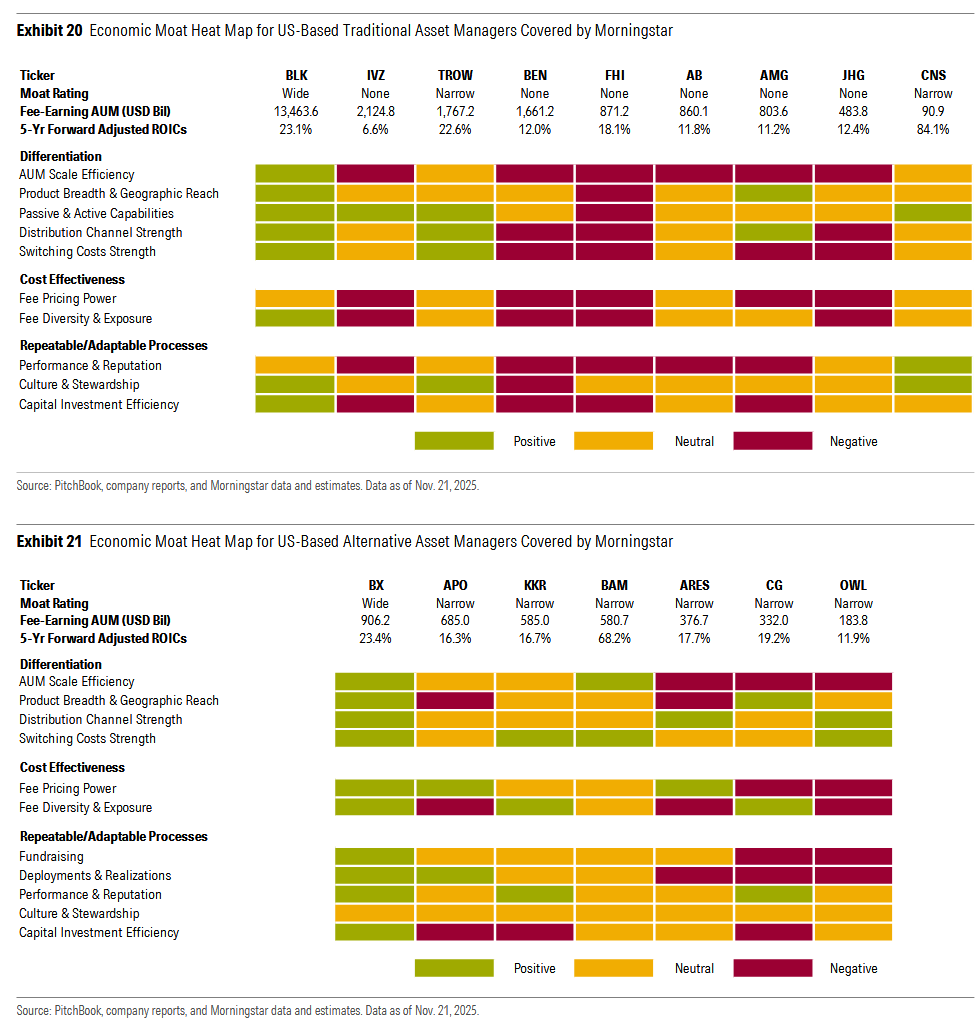

Alternative asset managers

Also regarding alternative asset managers, a Morningstar report by Greggory Warren provides a trove of exhibits about the publicly traded firms that he follows. For example, the image above shows the assets under management in the main alt categories for those firms.

As one subheading states, “Alternative Managers Operate in a Completely Different Ecosystem than Traditional Managers,” something reflected in the detailed moat ratings that are provided.

{kind=link}

Mission investing

Meketa provided a short summary of its Mission-Driven Investing Day Roundtable, which featured representatives of two leading asset owners:

The roundtable highlighted two different but deeply complementary paths for aligning capital with climate resilience, community strength, and long-term value creation. CalSTRS advances mission through a fiduciary lens by embedding sustainability across a global portfolio. MacArthur does so by deploying catalytic, risk-tolerant capital where it is most needed. Both models expand what is possible when mission becomes a strategic driver of investment decisions.

While the discourse about climate change and other issues seems to have gone underground, “Clients, beneficiaries, and communities increasingly expect capital to do more than deliver risk-adjusted returns.”

Book club

This time of year brings forth all kinds of “best of” lists, including those about books of the year. The author of the Substack newsletter Mr Market Miscalculates took an uncommon approach to reading in 2025:

I dedicated the entire year to “old, undiscovered gems”: the oldest was published in 1972 while the most recent is from 2017 but still covers the events of the October 1987 crash.

The document linked here is more than a list of books — it’s a wonderful set of short descriptions of notable events, ideas, and strategies that have shaped the investment world.

Other reads

“The Broken Yardstick: Why Your ‘Historic’ P/E Chart is Lying to You,” Fundamentally Sound.

Comparing the S&P500 PE ratio of today to that of the past is apples-to-oranges comparison. This common comparison assumes that the “E” (Earnings) in the 1990s and early 2000s measures the same thing as the “E” in 2025. It doesn’t.

“Marc Rubinstein on the Hidden Fault Lines in Modern Finance,” Michelle Celarier, Institutional Investor. Shadow banking, insurance portfolios, multimanager hedge funds, and similarities in today’s environment to the conditions that preceded the Panic of 1907.

“Mistrust and/or Distrust Between LPs and GPs,” Anthony Hagan, Freedomization.

A plethora of LPs, during initial GP engagement, define their method of due diligence as organic and people-centric, with a high emphasis on the motivations, integrity, and pragmatism of team members, but then launch into a very mechanical and mundane process of demanding large batches of ordinary information and asking pre-scripted, prosaic questions.

“2025 Buy-Side Quant Job Advice,” Giuseppe Paleologo, At night we walk in circles and are consumed by fire. An excellent overview, also of general interest to job seekers in other areas.

“Value Creation and Firm Life Cycle,” Tatjana Puhan. et al., SSRN.

Taken together, our results suggest a simple, implementable principle for long term public investors: tilt equity portfolios toward financially unconstrained mid-life firms and manage risk at the life cycle tails.

“How CalPERS aims to add 50-60 bps using TPA,” Amanda White, top1000funds. A look at the internal expectations for what will surely be one of the most scrutinized applications of the total portfolio approach.

“The Impact of U.S. Stock Buybacks: Theory vs Practice,” Victor Haghani and James White, Elm Wealth.

In sum, buybacks are not a neutral corporate finance choice but a force shaping market dynamics, investor welfare, and fiscal policy. Their rise since the 1990s may be one of the most under-appreciated drivers of U.S. equity market performance and warrants greater attention from academics, investors, and policymakers.

“Between Headlines and Numbers: Tracking What We Can’t Yet See in AI Buildouts,” Olga Usvyatsky, Deep Quarry. Digging into the accounting disclosures surrounding AI financing, equipment, and data centers.

“Peer Momentum,” Lionel Smoler-Schatz, Verdad.

Within biotech, we find that peer momentum adds predictive power beyond stock-level momentum, strengthening forecasts and improving signal robustness in a domain where traditional financial metrics are often uninformative.

Prescient

“The new writing will be about technology, the global economy, the electronic ebb and flow of wealth.” — Jay McInerney in Bright Lights, Big City (1984).

Flashback: Philip Fisher

In 1987, Forbes published two pieces about the investor Philip Fisher, a short appreciation from Warren Buffett followed by an interview with Fisher.

The interview delves into Fisher’s approach: a small number of stocks, many of which were held for a considerable length of time. He said, “I hate the buzzword ‘technology’,” but liked companies that “can expand their markets by taking advantage of the discoveries of natural science.” The general formula for his winners:

They are all low-cost producers; they are all either world leaders in their fields or can fully measure up to another of my yardsticks, the Japanese competition. They all now have promising new products, and they all have managements of above-average capabilities by a wide margin.

Also, he preferred it if clients argued against a new idea — if they were enthusiastic, “that’s usually a warning sign that it’s too late to buy.”

The interview begins with Fisher’s concern about the “huge overextension of credit in all directions.” The interviewer asked, “When will the crash come?” Fisher:

I haven’t the faintest idea whether we are in 1927 or 1929. Some awfully bright, able, sound people were scared as hell in 1927. But the thing rolled on for two more years, and that may happen here. I don’t know.

The date the issue was published? October 19. (Which happened to be the largest one-day market drop in history, by a sizable margin.)

The music of investment

A 2024 posting beings with a simple question, “Is your investment process jazz or classical?” It also deals with changes in process, the people involved, and investment categories:

Standards and practices and dividing lines don’t stand still. Appreciating what they are today — and understanding their power as social norms — is essential. But so is remembering that they aren’t eternal.

(All of the previous postings are available in the archives.)

Thanks for reading. Many happy total returns.

Published: December 29, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.