The latest Investment Ecosystem posting asked a simple question: “How Do We Know?”

It delved into “mapping the landscape of our understanding,” an essential aspect of due diligence:

Not nearly enough time is spent detailing what we don’t know.

What we think we know gets most of the attention and drives the narratives that lead to decision making.

The overlooked question is: “How do we know (what we think we know)?”

On to the readings for this issue, starting with an examination of the overall theme.

A complex adaptive system

It should be no surprise that a report titled “Reframing Financial Markets as Complex Systems” would be featured here, since that idea formed the foundation of this site.

The CFA Institute Research & Policy Center issued the report, which was authored by Genevieve Hayman and Raymond Pang. They argued that traditional financial models don’t adequately account for the way things really work:

Market-level phenomena (e.g., volatility, crashes, contagion, innovation) result from myriad interactions among heterogeneous agents (e.g., investors, firms, governments, regulators), often yielding unexpected (i.e., heavy-tailed) or nonlinear outcomes.

The heterogeneous adaptive agents don’t stand still:

Market participants differ in their goals and strategies, but they are mutually interdependent and adapt to each other’s behavior and environmental conditions. Investors, fund managers, and regulators react to each other’s activities, often in feedback loops.

Those reactions travel along interconnected networks that have changed dramatically over time. The complex systems that result “may exhibit resilience (the capacity to absorb shocks and reorganize), but they can also harbor hidden fragility.”

As you read this issue, think about how each of the topics reflects changes in the ecosystem. Identifying changes and the unappreciated x-order effects of them should be a core part of an investment process.

Cockroaches

Oh, boy. A month ago Jamie Dimon mentioned the possibility of cockroaches in the credit markets on an earnings call and now that’s all anyone talks about (including us).

Howard Marks used the meme (mixing it with the “canary in the coal mine” idiom) in a memo on the state of credit. While noting that issues are cropping up, he didn’t think they were systemic but a normal part of the credit cycle:

This isn’t part of the plumbing of the financial system but rather a regularly recurring behavioral phenomenon. So, it isn’t ‘‘systemic,’’ but it is “systematic.”

He revealed that his firm, Oaktree, had a small position in First Brands (one of the cockroaches), did some research, and “reached the correct conclusion” (although he wasn’t specific about what that meant). He wrote that during the firm’s long history they’ve “experienced plenty of defaults and even a few frauds,” which he says comes with the territory of “knowingly bearing credit risk for profit.”

Stephen Nesbitt of Cliffwater struck an emphatic chord in a short piece, “No Cockroaches in Private Debt.” As with Marks and other purveyors of product, he has a vested interest in whether that turns out to be true. (As you can judge from a posting, “The Interval Fund That Ate the Market,” from Covenant Lite.)

Nesbitt argues that credit problems will show up in the broadly-syndicated loan market, not in private credit. One reason: because those loans “are less likely to be private equity sponsored, making their debt more susceptible to weak management and fraud.”

But private debt is by no means immune from those kinds of problems. The recent case of Renovo Home Partners has drawn a lot of attention, since its (private equity sponsored) debt went from being marked at par to zero on BlackRock’s books when the firm went under. (Oaktree also owned the debt.) With more firms owned by private equity showing signs of distress, you can expect there to be other surprises, although maybe the holders will get better about marking them down in a timely fashion.

Concerns are spreading about the quality of ratings in private credit, the degree of concentration of that kind of debt (especially at insurance companies), and even the increased prevalence of private credit in the enormous and speculative AI buildout going on. Here’s Paul Kedrosky’s take on “The Great Credit Convergence”:

The line between public and private credit is functionally gone: there is a single continuum of liquidity and opacity.

That efficiency hides danger: spread compression, shared exposures, correlated marks.

Private credit is now infrastructure finance for AI (and defense and energy).

The only real lending difference now: who sees the marks — and when.

Across the credit spectrum we have seen a loosening of standards and an explosion in new debt structures. Given the dramatic changes since the financial crisis, it only makes sense to worry about the cockroaches that are showing up now.

If they continue to multiply we’ll know what terminology to use, thanks to Leyla Kunimoto of Accredited Investor Insights: “A group of cockroaches is called an intrusion.”

ESG, we hardly knew ye

In 2021, we published “The ESG Juggernaut and Points of Pushback,” which began with a sole sentence: “ESG is dominating the investment business.”

It used a paper titled “Seven Myths of ESG” to frame issues for both proponents and opponents of the many concepts embedded in the acronym to consider, in conclusion asking:

Does your organization have clarity about where it stands on these cornerstone issues? Do your actions reflect those choices? Do your clients and/or stakeholders understand your beliefs and why you hold them?

After the ensuing political scrum it’s time to pick up the pieces. Where to start?

“ESG Ratings Are Trash” (a paper by Brian Bolton) and “A Lawsuit Waiting to Happen” (a report by Bryce Tingle for the Fraser Institute) are focused on ESG ratings as they came to be, a disparate set of underlying ideas that was mashed together into a catch-all category by the workings of the investment industry in a dash for cash.

We are now back to the hard and necessary work of analyzing and identifying specific long-term risks to companies. Many of the concepts embedded in ESG are essential considerations in determining whether and how value will be created or destroyed. But they don’t fit together into a nice, neat package for marketing.

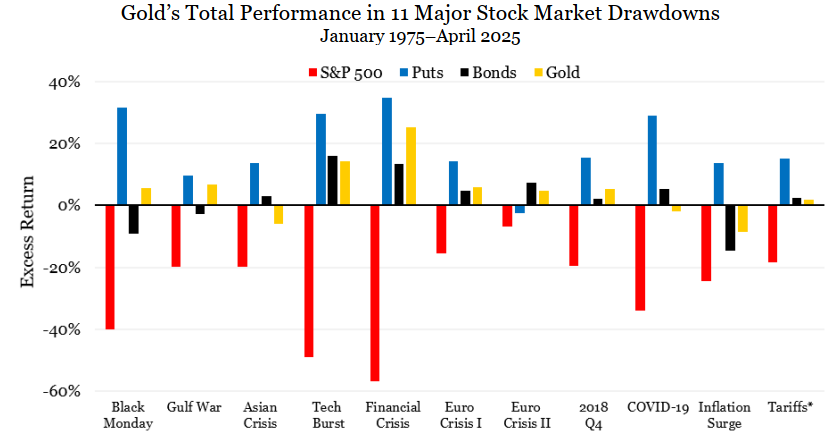

Gold

Investor interest and flows follow price, so gold has gotten a lot more attention lately than it usually does. This chart comes from “Understanding Gold,” a paper from Claude Erb and Campbell Harvey. They find that “when gold hits all-time highs, the subsequent multi-year returns are low or negative,” but a large number of exhibits paints a nuanced picture of gold, and the authors offer one intriguing possibility: that Basel III could allow commercial banks to hold gold for regulatory purposes, which would change the dynamics of the metal.

Other evaluations of interest come from D. E. Shaw and Man.

13Fs

Once upon a time 13Fs provided a fairly complete snapshot of what the big money (in equities) was doing, by showing what positions were on the books as of a half-quarter before, with which you could compare to the previous quarter and see what had changed. A Bloomberg article notes the general problems with that approach (the delay involved and the exposures not captured), but a posting from Inside the Mind of Mojo (“The ABCs of 12D Chess For 13Fs”) digs much deeper into how misleading the data can be:

This is the real anatomy of sophisticated capital deployment by modern hedge funds, and it’s the reason that treating 13F filings like stock-picking scorecards misses the entire game. These documents are quarterly freeze-frames of multidimensional systems in constant motion — static images of pawns being deployed in a sophisticated game of 12D chess.

Most press reports — and some investment strategies based upon 13F information — assume that the world operates the way it has before. That’s true in some cases, but not at the margins of alpha discovery, where change occurs.

Lone wolf

Recent issues of the Fortnightly have had sections about sell-side analysts. Here’s another:

The lone analyst with a sell rating on Fiserv Inc. ahead of the company’s crushing stock selloff says the writing was on the wall for months.

The headline on the Bloomberg story in which that appears referenced the “26-year-old analyst who beat Wall Street.” Dominic Ball, an analyst at Rothschild & Co Redburn, explained his stance:

There was a big dichotomy between what was happening on the ground, when we speak to merchants and retailers, versus what the investor base thought was happening.

The chart above comes from a Spencer Jakab column in the Wall Street Journal which asks, “Are Stock Analysts Useless?” His answer is no (but that their recommendations often are).

Factors and causality

A new brief, “Causality and Factor Investing: A Primer,” by Marcos López de Prado and Vincent Zoonekynd was published by the CFA Institute Research Foundation. Its theme is that the “econometric canon applied in factor investing studies — linear regression, two-pass estimation, p-values, and correlation-based statistics — rarely discusses causality,” leading to “real-world consequences.”

The “factor zoo” has turned into the “factor mirage,” a problem for the creators and consumers of the slew of products created over the last couple of decades.

In addition to a short examination of the thesis (which will be expanded upon by the authors in a coming work), a list of questions is included in the brief that can be used to craft “a due diligence questionnaire, investment memo, or strategy approval process.”

Other reads

“Alpha ex-Ante,” Lewis Enterprises.

The dividing line between debt and equity has melted into a gradient of structured promises. Credit investors now participate in upside through covenant engineering; equity investors protect their downside through liquidation stacks and preferred waterfalls.

“Somewhere Down There,” Jeffrey Ptak, Basis Pointing. Opening the nesting dolls of a fund to inspect the structure and fees.

“Winners and Losers in a World Without Quarterly Reporting,” Clare Flynn Levy, Essentia Analytics.

Whether in markets or in individual portfolios, the rhythm of information release shapes how decisions are made, how risk is managed, and how attention is allocated.

“A Company Sold Investors $1 Billion in Art. Did it Paint Too Rosy a Picture?” Zachary Small, New York Times. How one alternative asset class is being marketed to the masses.

“From Sharpe to Pedersen: Why Active Management Isn’t Zero-Sum After All,” Diego Costa, Enterprising Investor.

There must, therefore, be a middle ground: a market that is just inefficient enough to reward those who uncover information, but efficient enough to keep profits from lasting too long.

“The Gravity of Habit: How Assumptions Drive the Re-up Cycle,” Anthony Hagan, Freedomization. Thoughts on the “psychological game of Twister that GPs and LPs play” and how it is changing in a time of “hand-to-hand combat for every available commitment dollar.”

“‘Total Portfolio Approach’ Is Shaking Up How Trillions Get Managed,” Justina Lee and Lu Wang, Bloomberg.

To its proponents, TPA is a better fit than the old static model — known as Strategic Asset Allocation — for an unpredictable world in which inflation spikes or geopolitical shocks can easily upend market assumptions.

“Why poker is used to train traders,” Kris Abdelmessih, Moontower. A posting based upon a video by Jerrod Ankenman of Susquehanna.

“The Add-On Illusion: Why Traditional Attribution Analysis Misses the Mark,” George Pushner and P.J. Viscio, Kroll.

Created value attribution is certainly complicated by add-on acquisitions, but a careful and methodical breakdown of the value impacts of each add-on can identify true organic value creation and is a critical component of the measurement of Alpha.

Open doors

“When one door closes, another opens; but we often look so long and so regretfully upon the closed door that we do not see the one which has opened for us.” — Alexander Graham Bell.

Talent

A 2022 Investment Ecosystem posting used a book by Tyler Cowen and Daniel Gross as a jumping off point for examining issues of talent in investment organizations. One pitfall is that “you may end up experiencing the ‘winner’s curse’ of finding out you paid too much in your rush to capture that talent”:

That is especially true when notions of intelligence are intertwined with observations of an investment track record (which is an inherently noisy measure of quality). Intelligence is context dependent and so is performance. If you hire someone into a new organizational environment, they may struggle to understand how to succeed within it. Or they may encounter a much different market regime to navigate than they had before and find it difficult to adapt. Faced with tougher circumstances, their results may suffer, and perceptions of their intelligence may decline along with them.

Thanks for reading. Many happy total returns.

Published: November 17, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.