It’s an old story. A hot area of the market starts to show some cracks and a few notable players make the news because of outsized losses in failed investments.

Some hits in the credit markets have generated lots of headlines recently, which makes it a perfect time to ponder the quality of due diligence practices. That’s the topic of an upcoming essay from The Investment Ecosystem. To receive it in your inbox, subscribe here.

On to the readings.

Continuation funds

As markets evolve, assessments of a class of investment strategies or structures can change. For example:

The trajectory of continuation funds is a story of their remarkable turnaround, from a reputation associated with “zombie funds” to a repository of trophy assets.

That’s from a CFA Institute report by Stephen Deane and Ken Robinson on continuation funds, which acquire one or more assets from another fund managed by the same general partner. “The Rise of Private Equity Continuation Funds,” an excellent law review article by Kobi Kastiel and Yaron Nili, addresses many of the same issues, “exploring the cautionary tale [the funds] present to the conventional deference of law and economic theory to private contracting among sophisticated parties.” Among those issues:

~ There are all sorts of conflicts of interests. A general partner is purporting to act as a fiduciary for both sides of a transaction (including for new investors in the continuation fund that weren’t in the legacy fund). Those investors who move on to the continuation fund and those who cash out have different interests. Which group comes out ahead in the transaction?

~ Something on the order of ninety percent of investors don’t roll over their stakes. For many it feels like a forced choice, given the short amount of time to make a decision in most cases, the lack of information made available to them, and the inexperience of investing in individual companies versus hiring managers.

~ Limited partnership agreements “do not protect [limited partners’] interests regarding continuation fund transactions” (Kastiel/Nili) and the members of limited partner advisory committees aren’t responsible for representing the interests of all of the limited partners.

~ Law firms and financial advisors involved have their own interests in helping continuation funds be formed and in maintaining good relationships with general partners.

~ Limited partners are reluctant to litigate regarding questionable general partner tactics because they think it will impede their ability to gain access to other funds in the marketplace.

~ While advocates promote the funds as a “win-win-win” for all involved, in the end it’s the general partner that “almost always wins” (Kastiel/Nili).

These two sources provide a rich assessment of the practical realities and power dynamics in this area that should be of use to asset owners considering their options.

Given the rapid adoption of continuation funds, the historical record on them is sparce. Two recent papers provide some early evidence as to the composition and performance of them:

“From Exit to Extension: The Rise of Continuation Vehicles in Private Equity,” Leon Luepertz, et al.

“Continuation Funds: Performance and determinants 2018-2023 vintages,” Oliver Gottschalg.

Differentiation

One concept we use in evaluating investment organizations is a simple ledger with “same as” on one side and “different than” on the other. True differences are relatively rare, be they in investment process, operations, or any other facet of organizational design or activity, since most organizations within a particular realm look alike in big ways and small.

That’s true with portfolio structure too, which makes a new paper from Rocco Ciciretti, et al., “Portfolio Overlap and Mutual Fund Performance,” of particular interest. The authors “find evidence of a negative relation between portfolio overlap and the fund’s future extra performance where only low-overlap funds, i.e. those that differentiate more their holdings from those of other funds, achieve positive risk-adjusted returns.”

Building those kinds of portfolios is behaviorally difficult, especially during periods of weak relative performance, when pressure from internal and external sources magnifies a portfolio manager’s concerns about career risk. Building a culture that mitigates those tendencies and encourages differentiation should be a leadership priority.

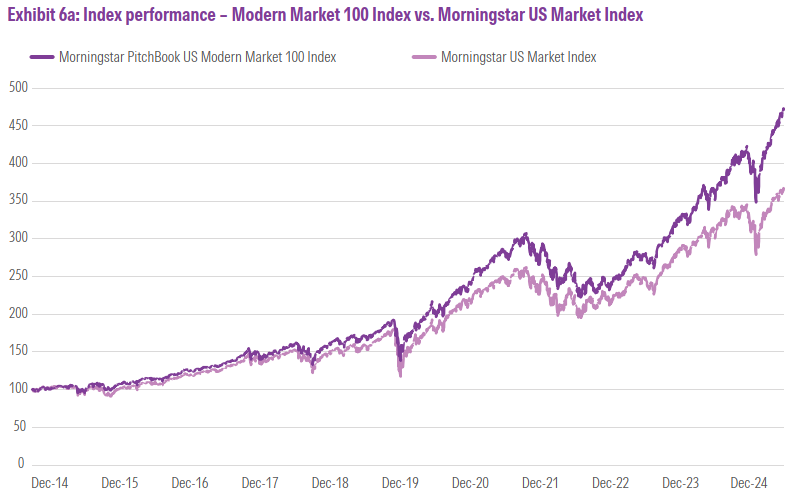

The modern market

Morningstar released a report, “When Public Meets Private: Rethinking the Modern Market,” in which it highlights the performance of the Morningstar PitchBook US Modern Market 100 Index, which “has outperformed its public market equivalent over all trailing time periods with lower volatility.”

The index is comprised of the ninety largest public companies and the ten largest private firms. Well, sort of. Venture-backed private firms; large, successful private companies aren’t spicy enough.

Using Morningstar’s sector classification, the combination yields a technology weighting that is close to fifty percent (about fifteen points higher than the firm’s public index). The report concludes:

This is only the beginning. We are committed to developing a next generation of companion indexes designed to equip investors with more accurate tools, deeper insights, and better ways to navigate an evolving market landscape. Together, these innovations will help move the science — and art — of investing forward, enhancing transparency, access, and opportunity for the entire market ecosystem.

Let’s see: technology, convergence, and indexing as innovation. It checks all of today’s boxes. But in a few years will it still be at the center of trends or the vestige of a particular era?

Seating charts

One of the virtues of onsite due diligence is to see how offices are organized and, if possible, to observe where people sit at meetings. Cultural dynamics are reflected in how people are arranged, something that Matt Levine has covered well in sections of his columns titled “Everything is seating charts.”

If you think that masters of the universe don’t care about such mundane things, take a look at a recent New York Times article by Ken Belson. In the print edition, its headline was “Inside the N.F.L.’s Most Powerful Huddle” (the quarterly meetings of the league’s owners). But the online title better captures the scene: “Inside the World’s Most Powerful High School Cafeteria.” To wit:

The seating chart in effect serves as a proxy for their status and their beefs.

Read it and know that such concerns motivate behavior even in organizations that seem above it all.

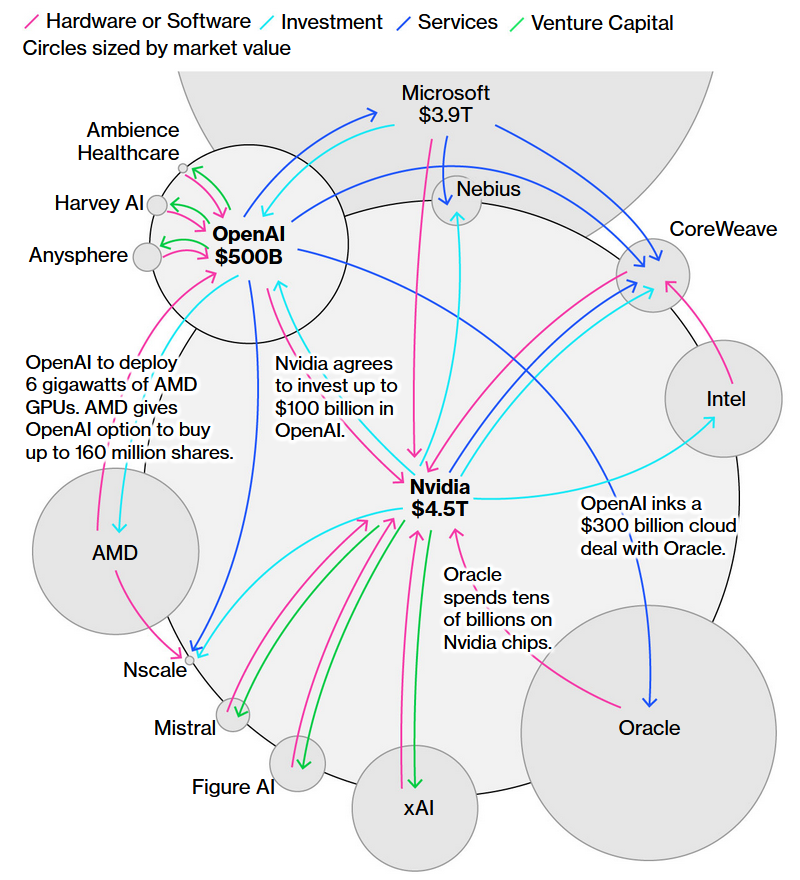

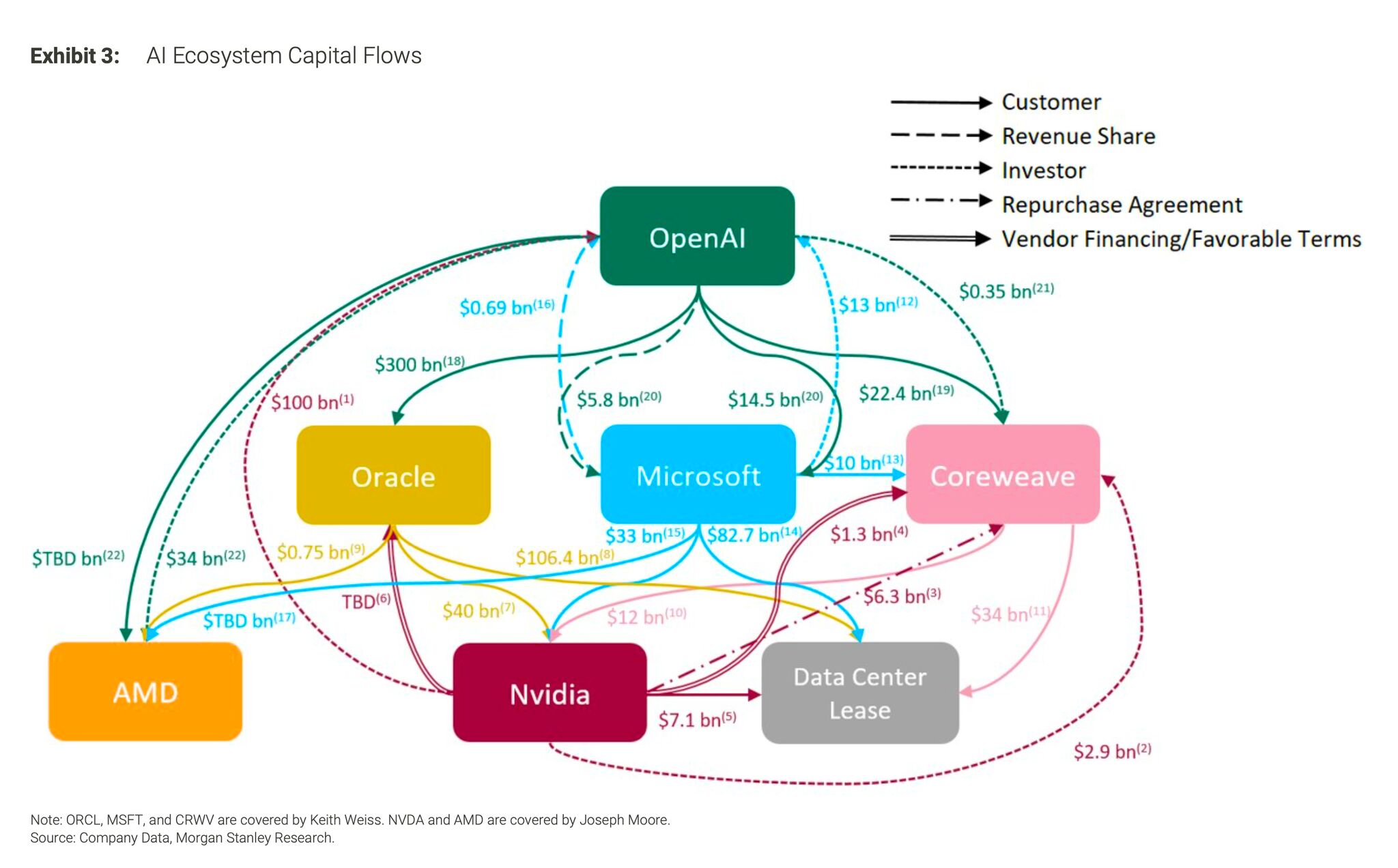

A complex web

There have been a number of attempts to map the increasingly recursive investments of key companies in AI. For example, from a Bloomberg story, which called the relationships a “complex web”:

This one comes from Morgan Stanley:

This one comes from Morgan Stanley:

Each published within the last couple of weeks, the images are already out of date, as new announcements seem to come nearly every day. What’s the endgame?

Other reads

“Investing as Myth-Making,” Alexander Campbell, Campbell Ramble. Stories are what drive the markets — and a simple structure (compelling narrative, inconvenient reality, genuine complexity, and predictable endgame) is used to summarize a bunch of the popular narratives of the day.

“Exploring Capital Efficiency,” AQR.

The most diversifying investments are the most likely victims of this “line-item thinking” because their performance tends to stand out in the broader portfolio.

“Unlocking Domestic Investment Opportunities: Aligning Public Goals with Pension Fund Realities,” International Centre for Pension Management. Regarding “the investable window” — how things need to come together for infrastructure investments to be successful for governments and investors.

“Where Factors Speak Loudest,” Lionel Smoler Schatz, Verdad.

We believe size matters — not as a standalone source of return, but as a modulator of other factors. In our research, we have found factor premia are strongest in microcaps and fade gradually as market cap increases. Small size amplifies factors, while large caps dilute them.

“The diversification illusion: how indexing turned the S&P 500 into a single risk bet,” Philip Hackleman and Álvaro Freile, Citywire Americas. On the effect of indexing “in changing correlations between independent stocks.”

“6 Ways Longevity Is Transforming Investment Careers,” Tiffany Tivasuradej and Sarah Maynard, Enterprising Investor.

The investment industry’s greatest asset has always been its people. As populations age and careers extend, that asset is changing in ways firms can’t ignore.

“The Mysterious Billionaire Boss at Jane Street Smashing Trading Records,” Sridhar Natarajan, et al., Bloomberg. A fascinating story of a very un-Wall-Street-type co-founder of the highly successful firm.

“Changing Times,” Charles Skorina.

If most investment managers think alike, what’s to keep AI and algorithms from taking their jobs?

“Alternative Investment Due Diligence For RIAs: A Framework For Compliantly Evaluating Private Funds,” Ben Henry-Moreland, Nerds Eye View.

In short, different investments require different levels of due diligence. While some are relatively transparent about their structure, risks, and costs, others require a much deeper dive for an advisor to meet the “reasonable basis” standard.

“This is a warning,” David Villalon, LinkedIn. Copilot in Excel and “the risk of embedding non-deterministic AI into critical business functions.”

Keep them simple

“The simplest questions are the hardest to answer.” — Northrop Frye.

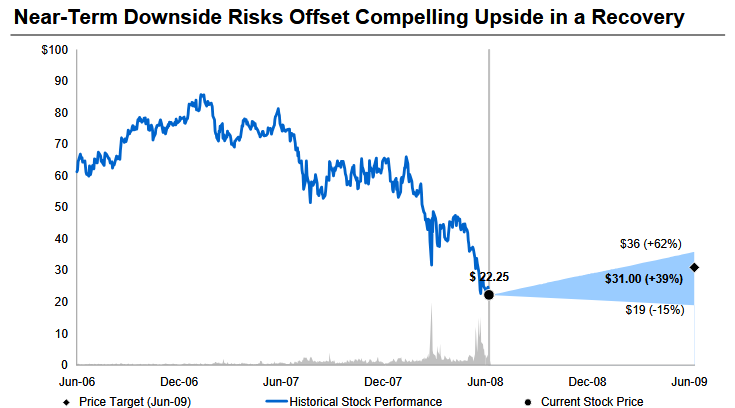

Flashback: Lehman Brothers

It’s only been three months since Lehman appeared in a Fortnightly flashback, that time featuring a 2007 slide deck describing the firm’s internal risk management.

We revisit the topic because Bryce Elder of FT Alphaville dropped a posting that included a trove of links to sell-side reports from around the time that Lehman went bust. Short summary: no one had a clue what was happening. Given that the lessons of the past aren’t always passed on, the reports should serve as a module in investment training programs.

The chart above comes from a Morgan Stanley piece. Such a “cone of possibilities” that shows the bull, bear, and base cases of an analyst is much preferable to a single target price under normal conditions, but it too fails in an all-bets-are-off situation. The stock was a zero in less than three months.

A view from the inside

An essay on this site a year ago reviewed Private Equity, a memoir that oddly enough wasn’t about private equity per se, but the the culture inside one of the most highly recognizable investment firms of the day.

At its core, it is about the cultural divide that exists at most firms:

Those supporting the investment team were seemingly a world apart from it, and relatively small in number. As such, they were surrounded by the trappings of wealth and status but not really a part of it.

Those insiders know things about the organization that even the most astute outside observers and due diligence analysts don’t. As a result, the book is revealing.

Thanks for reading. Many happy total returns.

Published: October 20, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.