Programming note: The Fortnightly will not be published on October 6, returning two weeks later.

In case you missed it, the most recent Investment Ecosystem essay is “The Tyranny of the Playbook,” which examines “the missing art in the management of investment organizations.”

Humans and machines

Tesla represents one of the oddest market stories of the past several decades. An amazing success in many respects, it is also known for some shady practices and frequent promotional claims regarding new features that turn out to be vaporware. And for a very high multiple on its stock.

Those investors who love it really love it, and the same could be said for sell-side analysts. A Financial Times article by Bryce Elder recounted the breathless and persistent advocacy of Tesla by Adam Jonas and his autos team at Morgan Stanley in 62 reports so far during 2025. (A total of 32 reports were written about all of the other seventeen stocks that the team covers.)

A sell-side analyst has a hard job. It’s a challenge to avoid being buffeted by market moves — last week, an analyst upgraded Tesla at $416 after downgrading it at $308 in June — and there are pressures and potential conflicts from all sides (companies, clients, and your firm). Add to that the risk of falling in love with a stock or a CEO and you have a behavioral minefield.

So when will those rational machines take over?

Two other Financial Times articles address aspects of that question. Alan Livsey looks at a Bernstein Société Générale test which showed that AI did pretty well with some basic tasks, but:

After this, everything went a bit sour. Making pretty pictures and assessing the tone of earnings calls only make up a small portion of an analyst’s job.

In a similar vein, Robert Buckland thinks the junior analysts doing those basic tasks are most at risk now, with the people at the top not being disrupted any time soon. In more than three decades on the sell-side, even as supporting technology advanced, Buckland saw very little change in the structure of how the work was done. Now it’s coming and organizations (including slow-to-change sell-side ones) will be transformed.

So the questions are how fast and in what ways that will happen. (Reach out if you want to have a discussion about what it might mean for your organization.)

Greatest hits

Focus Consulting Group marked its 25th anniversary with a compendium of ideas across the years written by its founder Jim Ware. The firm has produced an impressive pile of books, papers, and videos over that time, all focused on the continuous improvement of investment organizations. Its work on culture is particularly notable, including examining the various tribes within an organization, the importance of leadership behavior, the pernicious effects of blame, and the damage that can be wrought by a “Red X.” All (and much more) covered in this summary.

Wounded lions

A Bloomberg article by Nishant Kumar carried the title “Hedge Fund Traders on a Bad Streak Are the Hottest Recruits Around.” You might not believe it, but:

Rather than being damaged goods, veteran portfolio managers making heavy losses are now some of the hottest recruits around.

Fallen stars are being viewed as battle-tested hunters temporarily off their game. That moment of weakness is when they’re most poachable, driven and available at a discount, people with knowledge of the matter say. Instead of the slog of recouping a pile of losses at their previous employer, traders can wipe the slate clean and start making money for themselves again.

While the trend is “infuriating some important investors and hedge fund bosses,” a hedge fund recruiter provides the pitch:

Even a wounded lion is still a lion. And the lion isn’t mortally wounded. He will heal. And when he’s fully back, that lion is worth a lot more money.

A fascinating read.

Focus versus diversification

There is an ongoing debate about concentration versus diversification in investment portfolios (see recent items from Owen Lamont of Acadian and Brian Chingono of Verdad arguing against concentration). This image does not address that, but rather the discount given to companies with diversified operations versus focused ones.

The analysis comes from BCG. It concludes:

On average, companies that streamlined their scope, concentrated capital and talent, and followed through with disciplined transformation outperformed peers in both relative [total shareholder return] and valuation metrics.

As you might suspect, and as is shown in the chart, the attractiveness of focus versus diversification varies in response to the economic environment. BCG makes a long-term call on what works:

Although diversified models can offer advantages in moments of systemic crisis, the long-term premium increasingly favors focus. In today’s market, where strategic clarity is scarce and investor scrutiny is high, focus is a path to market outperformance.

Reinventing cap-weighting

Research Affiliates, which is known for its pioneering work on “fundamental indexing,” has introduced another new variety of index, one “designed to fix a costly but little-known ‘bug’ in cap-weighted indexing.”

As with previous RA offerings, the index selects holdings based upon fundamentals but in the new incarnation weights them according to their market values. The firm says that results in “better macroeconomic representation and better performance,” specifically by avoiding the “performance drag of procyclical rebalancing” of the leading cap-weighted indexes.

Another permutation. As with all things like this, how well will the forward look match the backward one?

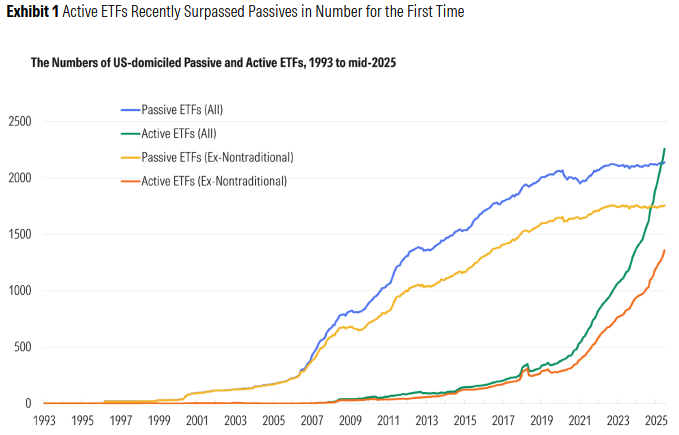

Active ETFs

While the massive size of passive ETFs means that they dominate active ETFs in terms of market value, the number of active ETFs is rising dramatically, as illustrated in the chart.

It comes from Morningstar’s “Guide to Active ETF Due Diligence.” The report covers strategies that are well-suited to active structures (and those that aren’t); the relationship of ETFs that are linked to or derived from traditional fund structures; the importance of bid-ask spreads to the total cost of ownership; transparent versus non-transparent vehicles; differences in tax efficiency; and more.

Other reads

“Familiar Signal, New Context: The Evolution of Earnings Call Sentiment Analysis from Lexicons to LLMs,” Mengmeng Ao, et al., S&P Global. On the effects of moving from rules-based natural language processing to LLM-based sentiment models.

“AI Will Not Make You Rich,” Jerry Neumann, Colossus.

There is nothing better than the beginning of a new wave, when the opportunities to envision, invent, and build world-changing companies leads to money, fame, and glory. But there is nothing more dangerous for investors and entrepreneurs than wishful thinking.

“Wish I Was Making This Up,” Jeffrey Ptak, Basis Pointing. Talk about a bad combination: A fund paying out high distributions (including a return of capital) and investors chasing performance results in a bizarre bottom line for them.

“Songs my portfolio manager taught me (part 6),” Dan Davies, Back of Mind.

When this sort of order went round, usually after complaints from the sales desk of not having enough research to sell, everyone did the only thing they could do; they took all the existing crap they had, and lied about their level of conviction.

“Fun with Numbers, feat. The American Investment Council,” Tim McGlinn, TheAltView. Sloppy (misleading?) advocacy by an industry group made up of major players.

“How do you get management to talk about things they don’t want to talk about?” Ian Cassel, MicroCapClub.

They only invest in businesses where there is enough transparency to allow them to see the business separate from whatever management is telling them.

“Best Practices for ERISA Plan Sponsors and Fiduciaries in a Changing World,” Stephen Rosenberg, Wagner Law Group. Six recommendations for “A Cheat Sheet for Deciding Whether to Add Private Equity or Other Alternative Investments to Plans.”

“Hedge Funds Have a Reputation for Ruthlessness. Dmitry Balyasny Took a Different Approach.” Michelle Celarier, Institutional Investor.

“Dmitry leads first and foremost through positive reinforcement, which means that the firm’s culture is really characterized by encouragement and support, not fear,” says chief risk officer and partner Alex Lurye.

Cause and effect

“The answers you get depend upon the questions you ask.” — Thomas Kuhn.

Flashback: Showing again

Robert Redford’s death last week brought forth an outpouring of memories of his acting and his work as a director and promoter of independent films. It also caused fans to watch his movies, including All the President’s Men.

Redford became interested in the story of Watergate well before it garnered much attention — and bought the rights to Woodward and Bernstein’s book even before it came out, then starred in the film version of it.

It is particularly timely to revisit it today. Then, there were many examples of Nixon administration officials criticizing and pressuring the Washington Post about its reporting, waging a public campaign against it while covering up and lying about the facts of the matter.

Now we are seeing unprecedented attacks on the press by the current administration, including several multibillion-dollar lawsuits by Trump against media companies, direct pressure on firms to axe content/people, regulatory actions being subject to toeing the administration’s line, and threats to suspend broadcast licenses for exercising free speech rights.

More than a half century later, the words of Ben Bradlee at the end of the film are once again relevant:

Nothing’s riding on this except the First Amendment of the Constitution, freedom of the press, and maybe the future of the country.

Process improvement

Among the pieces in the archives is “Creating and Sustaining Process Improvement,” a posting from 2022. It examines improvement loops and the differing effects of “working harder” and “working smarter.”

Thanks for reading. Many happy total returns.

Published: September 22, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.