A late August buffet of tasty reads for you before market activity starts to pick up again.

As a reminder, the mission of the Investment Ecosystem is to help investment professionals and organizations working on continuous improvement. To that end, if you ever want to weigh in on how we are doing — regarding our publications and courses, or Tom Brakke’s presentations and consulting work — you may do so anonymously here.

The hunt is on

In a Bloomberg story, “Private Equity Keeps Inventing New Ways to Give Cash to Investors,” Andrea Auerbach, global head of private investments at Cambridge Associates, was quoted as saying:

All sides of the industry are looking for liquidity in different ways. The hunt is on.

The dearth of distributions from private vehicles has changed the game. The illiquidity premium is starting to look like a penalty.

Preqin put summaries of three different vehicles — continuation funds, evergreens, and secondaries — into one short report, “Unlocking Liquidity in Private Markets 2025.” Each is related to the current theme, although they don’t really fit together — or deal much with the problem except on the margins and over time.

Jason Zweig of the Wall Street Journal aims a laser pointer at the core issue in his column, “The Ivy League Keeps Failing This Basic Investing Test.” Those endowments pressed the edge of the envelope on private funds and, as happened to them during the financial crisis, outside events unveiled the inherent risk in their strategy. While not (yet) facing their own threats from the Trump administration, other asset owners who gorged on privates in imitation should see the trade-offs differently now.

To look at liquidity and private equity in a different way, Richard Ennis and Daniel Rasmussen analyzed the “public-market pricing of private equity interests on the London Stock Exchange.” While the number of vehicles included in the review is admittedly small, collectively they hold over a thousand buyout funds. The authors conclude that private equity is more volatile, more correlated, and has a much higher beta than public equity — and that discounts to net asset value are below and much more variable than those indicated by reported secondary transactions.

The drinking game

Long-time CNBC correspondent Bob Pisani started a Substack newsletter. His first dispatch was about dealing with difficult people (he used a different word). The most recent posting is “Drinking on Wall Street: A Primer.”

Pisani paints the drinking scene in some detail. What’s most interesting is his place within that culture, how and why he did some of his work over cocktails and what parts of the market story come out in that setting versus others.

Also of interest was his view of “the dirty truth about Wall Street commentary: most of it is crap”:

80% of it was garbage, and I am not exaggerating. Most analysts and strategists exhibit very little original thinking and are exceptionally poor writers.

Journalists and investors both need to get at the story (and be able to tell it well). We have much to learn from each other.

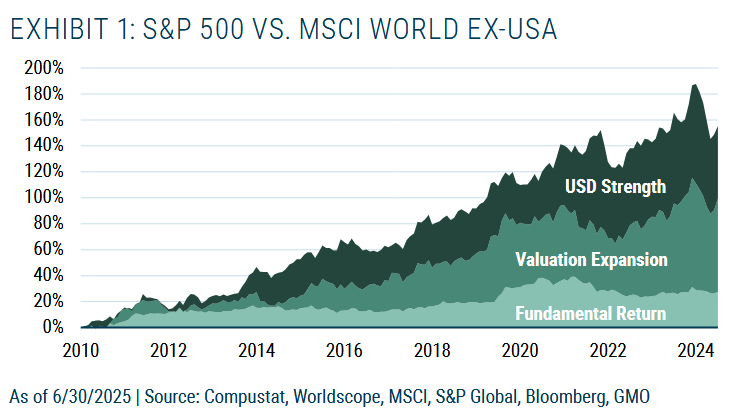

Unexceptionalism

The latest letter from Ben Inker and John Pease of GMO is “American Unexceptionalism,” a play on the pervasive phrase that doesn’t include the “Un-.” The new description stems from the relatively small portion of differential return of the S&P attributable to fundamentals:

The magnificence of the success of the very largest companies in the U.S. stock market has led to an assumption that U.S. companies on average have done well, when in fact they have not.

The chart is also included as an example of another kind of unexceptionalism: the use of stacked-area charts when a regular line chart would provide more information. The same information done in that fashion would allow for accurate and easy observation of the ebb and flow of the three individual parts, something that is not possible when values are stacked together. (This example is a convenient one, but stacked-area charts are a widespread industry scourge.)

Hedge funds

On the same day last week, Bloomberg published two articles on hedge funds. One: “Frustrated Hedge Fund Investors Push Back on Sky-High Fees.” The other: “Investors Pile Back Into Hedge Funds With Decade-High Inflows.”

The first article is really about the passthrough fees of multistrategy funds — and a few asset owners balking (or talking about balking) at the high levels of fees that the funds are levying against gross returns. But the story itself doesn’t really live up to the headline. There may be an inclination by some to push back on fees, but there’s no real sense that it’s happening much at all. And, for those firms that have had “unusually high returns,” the asset owners are not as concerned (although in that case they’d sure like to have a cash hurdle in place).

According to the other article, no matter those qualms, “appetite for the largest multistrategy firms . . . has remained consistently high.” Allocators are pushing hedge funds these days — despite the owner-unfriendly terms that have remained in place for decades — and multistrats, the latest and boldest manifestation of those terms, are the luxury goods that people want to say they own.

Buffer funds

AQR has extended its previous work on buffer funds, with a short summary on its website and an extended article published in the Journal of Portfolio Management. As before, the verdict is that the popular funds underdeliver on their promised goals. For starters, those payoff diagrams that are part of the pitch don’t represent reality very well. In fact,

Buffer funds are less a breakthrough and more a familiar repackaging: the promise of comfort, cloaked in complexity, at the cost of risk-adjusted returns.

In that they uphold “the broader lineage of structured products,” with the analysis adding to “a growing body of evidence that much of the innovation in this space is superficial, engineered more for sales than for substance.”

Individual investor power

Marc Schmitt sees a pattern in recent years that has “reshaped the trajectory of financial innovation itself.” A couple of quotes from his paper:

The technology-enabled rise of individual investors has democratized financial markets, challenging the long-standing dominance of Wall Street professionals.

Existing models often assume rational agents operating within information-efficient environments, overlooking the behavioral patterns and technological affordances of the modern individual investors.

There is no doubt that market power has shifted somewhat — just ask those pros who were on the short side of the big meme stocks — but to what degree?

Along similar lines, Byrne Hobart wrote a posting on The Diff about “Corporate Populism,” in which he sees new kinds of corporate activity designed to appeal to retail investors. Investor relations of a different sort.

Other reads

“The Calculus of Value,” Howard Marks, Oaktree. A great exposition of price and value, with some comments on the current market state.

“Private Credit Hyperscalers Risk Eroding Investor Returns,” Jeffrey Diehl, et. al, Adams Street.

Rapid asset scaling increases pressure on investment teams to deploy capital, which can compromise underwriting standards and credit selection. This can lead to sub-par returns, an underappreciated risk for institutional investors, the traditional source of capital for private credit managers.

“Being an angel investor is tougher than it looks,” Craig Coben, Financial Times. Years of investment experience in one area don’t necessarily prepare you for another.

“It’s So Simple,” Jeffrey Ptak, Basis Pointing.

Talk about a good sort. It’s an almost perfect stairstep from the cheapest funds to the priciest and it didn’t matter how long the period was.

“Cash Holdings,” Michael Mauboussin and Dan Callahan, Morgan Stanley Investment Management. How should we think about cash on corporate balance sheets?

“Seemingly Straightforward Positive GP Characteristics That Are Tricky For LPs To Evaluate,” Anthony Hagan, Freedomization.

The tone of a GP’s or placement agent’s fundraising frustration visibly and audibly changes when these individuals believe their product truly embodies or delivers what LPs have historically sought, yet it still fails to gain the expected traction.

“Are Busy Analysts Detrimental? Evidence from Stock Price Crash Risk,” Lucas Schwarz and Flávia Dalmácio, SSRN. What workload produces the best results? (A universal and important question; see also this posting.)

“The Spectrum of Infrastructure Assets,” Meketa. A summation of the range of offerings.

Talking your book

“I have never been more right.” — Neil Woodford, to his fund company board, two months before the fund was suspended due to an illiquidity crisis (source).

Flashback: Leverage

Leverage builds in every cycle before some of it is cleared out (in whatever manner). You could date our current market cycle to the end of the financial crisis — quite a long time — or the pandemic-induced selloff. In either case, we’ve seen leverage increase of late in a variety of ways.

That makes it a good time to link to a D. E. Shaw piece from 2010, “Lessons from the Woodshop: Common Sense in Managing and Measuring Leverage.” The woodshop reference is an analogy to woodworking:

Leverage and power tools share three fundamental properties: they can be extremely helpful, they can allow for far greater precision, and they can be really dangerous, even in the hands of experts.

The conclusion:

Quantity should not be the sole consideration in evaluating leverage. Equally important are the quality and riskiness of both the portfolio and the leverage supplied.

Wined and dined

The only posting in a short-lived category on this site, “Lutèce, Antoine’s, Arnaud’s — and Denny’s” recounts being wined and dined by companies and brokers forty years ago. Some things have changed, but this hasn’t:

Wherever you are in the ecosystem, there are people whose job it is to curry favor with you.

Thanks for reading. Many happy total returns.

Published: August 25, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.